Lucid Motors (NASDAQ: LCID) has continued to face headwinds since its 2021 IPO, falling short on production and delivery targets while battling mounting financial losses and stock dilution concerns.

Despite strong backing from the Saudi Public Investment Fund (PIF), fears of further dilution persist, and the company’s high-end pricing limits its market reach as affordability becomes an increasing priority in the EV sector.

However, the start of 2025 provided a rare boost for the struggling luxury EV maker. Lucid’s stock hit a five-month high after the company delivered stronger-than-expected Q4 production and delivery figures, igniting market optimism.

Picks for you

The momentum continued on February 25 as Lucid posted a rare double beat in Q4 and FY 2024 earnings, surpassing analyst estimates with $234.47 million in revenue, a 48.9% increase year-over-year, and a narrower-than-anticipated loss of $0.22 per share. The upbeat results sent LCID shares soaring 10.71%, peaking at $2.86.

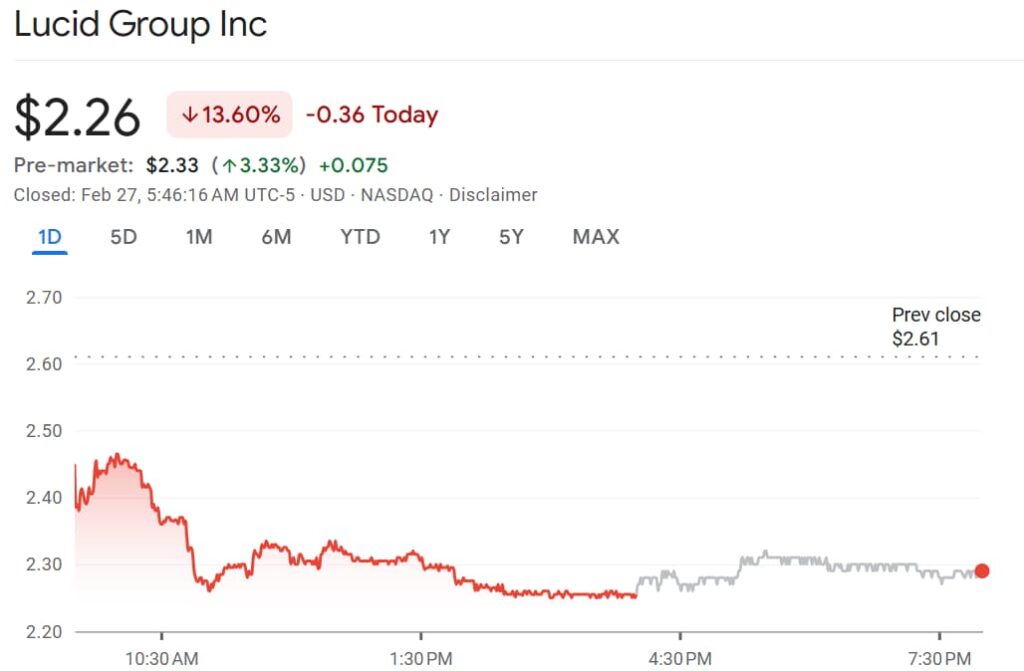

Yet, the optimism was short-lived. The abrupt resignation of CEO and CTO Peter Rawlinson triggered a sharp sell-off, with investor confidence further shaken by a Bank of America downgrade. As a result, LCID shares tumbled over 13% on February 26, closing at $2.26.

With analysts revising their price targets, concerns over Lucid’s leadership stability, production scalability, and competitiveness in an increasingly price-sensitive EV market have resurfaced, adding further uncertainty to the company’s outlook.

Analysts update Lucid stock price target

Following Rawlinson’s unexpected departure, analysts have reassessed their outlook on Lucid, with many expressing skepticism about the company’s long-term prospects.

On February 26, Bank of America analyst John Murphy slashed Lucid’s stock price target from $3 to $1 and downgraded it to ‘Underperform,’ calling Rawlinson’s exit ‘much more consequential than understood by the market.’

The analyst believes key product launches, including the highly anticipated 2026 mid-size platform ‘Space,’ could face delays or never materialize, further threatening Lucid’s production scale.

He also noted that the leadership turmoil could drive well-informed consumers toward competitors, further impacting sales. Given these risks, the analyst cut volume estimates and pushed back the timeline for Lucid to achieve positive gross profit.

Meanwhile, Needham analyst Chris Pierce reiterated a ‘Hold’ rating on LCID stock, acknowledging the company’s progress in deliveries and its increased advertising push for the upcoming Gravity SUV.

However, he noted that the timeline for achieving profitability remains unclear, and the leadership transition has created uncertainty about the company’s strategic direction.

At the same time, Stifel Nicolaus analyst Stephen Gengaro viewed Lucids’ updated financial outlook as ‘subtle positive’ but remained cautious, maintaining a ‘Hold’ rating on the stock with a $3.50 price target.

Cantor Fitzgerald analyst Andres Sheppard also reaffirmed a ‘Hold’ rating on LCID with a $3 price target, acknowledging the company’s technological edge in battery efficiency, longer range, superior performance, and faster charging compared to other EVs.

However, Sheppard remains cautious due to high negative gross margins, capital needs, leadership uncertainty, and worsening macro conditions, keeping a neutral stance on the stock.

Featured image via Shutterstock