As the third quarter of 2026 begins, markets continue to reward artificial intelligence exposure and growth stocks, but not every company is benefiting from the trend.

Concerns over weakening fundamentals, stretched valuations, and persistent cash burn have raised risks for several names.

With that in mind, Finbold has identified three stocks investors may want to avoid in Q3 2026 despite their potential upside.

Robert Half (NYSE: RHI)

Robert Half (NYSE: RHI) is still working to stabilize its business after a difficult period for the staffing industry. In the first quarter, revenue fell 4% year-over-year, while a temporary 56% tax rate hurt profitability.

The company cited economic uncertainty, conflict in the Middle East, and higher energy costs as headwinds, while weaker demand for compliance and risk-remediation services weighed on its Protiviti division.

To improve results, Robert Half implemented cost cuts expected to generate $30 million in annualized savings and is targeting third-quarter net income and earnings per share growth of 8% to 12%.

However, the turnaround remains unproven. The stock trades at roughly 25 times earnings, above the industry average of 18 and peer-group average of 16.

With revenue still declining and valuation elevated, Robert Half’s recovery story depends largely on future execution rather than current results.

As of press time, RHI stock traded at $30.70, up about 13% year-to-date.

SanDisk (NASDAQ: SNDK)

SanDisk (NASDAQ: SNDK) has been one of 2026’s top-performing stocks. As of press time, shares traded at $2,273, up 757% year to date and roughly 4,000% since its February 2025 spinoff from Western Digital.

The rally has been supported by strong operating performance. Data center revenue jumped 233% sequentially, total revenue rose 251% year over year, and gross margin expanded to 78.4% from 22.5% a year earlier.

Quarterly revenue reached $5.95 billion, while management expects up to $8.25 billion in fourth-quarter revenue. The company also has $3.74 billion in cash and no debt.

The bull case hinges on AI infrastructure spending and long-term hyperscaler agreements permanently reducing the industry’s cyclicality. However, memory markets have historically swung from shortages to oversupply when capacity expands or demand growth slows.

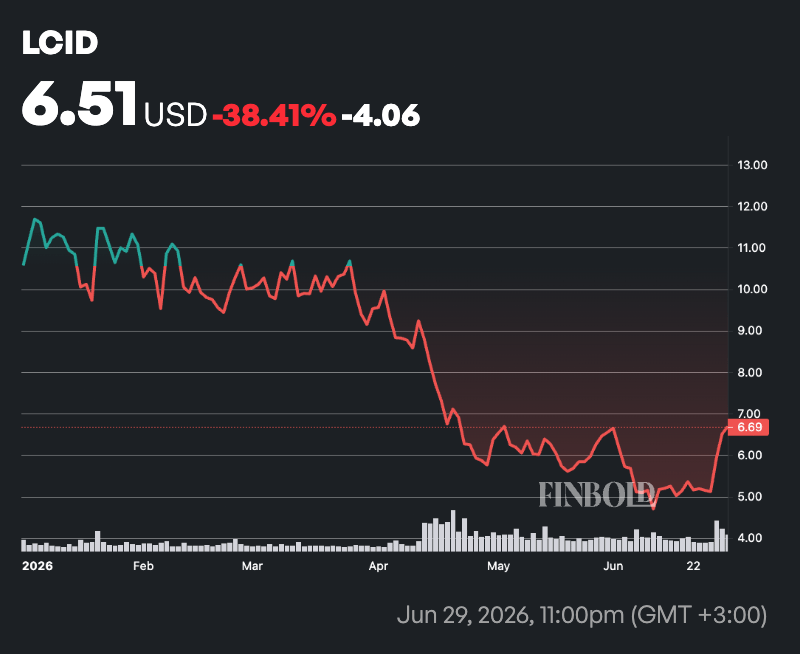

Lucid Group (NASDAQ: LCID)

Lucid Group (NASDAQ: LCID) remains one of the most financially challenged companies in the electric vehicle sector.

In its latest reported quarter, the company generated approximately $523 million in revenue while posting a net loss of about $814 million. Free cash flow was negative $1.24 billion, and gross margin stood near negative 93%.

Lucid reported first-quarter 2026 earnings per share of negative $2.82, missing analyst estimates by nearly $0.29. A year earlier, its net profit margin stood at approximately negative 291%, underscoring its ongoing profitability challenges.

Cash burn remains a major concern with the EV maker spending roughly $3.8 billion annually against about $3 billion in cash and investments, implying a runway of three to four quarters, or six to seven quarters including available credit facilities.

The company has also relied on fresh capital. For insurance, in April 2026, Lucid raised $300 million through a common stock offering and secured an additional $550 million in convertible preferred investment from Ayar Third Investment, which is linked to Saudi Arabia’s Public Investment Fund.

Meanwhile, 69 million shares remain registered for future resale, increasing dilution risk for existing shareholders.

Operational challenges have further weighed on sentiment. A seat-supplier issue forced a 29-day halt in Gravity SUV deliveries, disrupting production and prompting a shareholder-rights law firm to launch a securities-law inquiry. As of press time, LCID stock traded at $6.69, down about 40% year to date.

While backing from Saudi Arabia’s Public Investment Fund reduces near-term insolvency risk, Lucid’s path to sustainable profitability remains uncertain, and continued capital raises could further dilute shareholders.