Palantir Technologies Inc. (NYSE: PLTR) has had a standout year in 2024, emerging as a key player in the artificial intelligence (AI) space. The company’s platforms—Gotham, Foundry, Apollo, and AIP—have driven investor interest, showcasing Palantir’s strength in AI innovation.

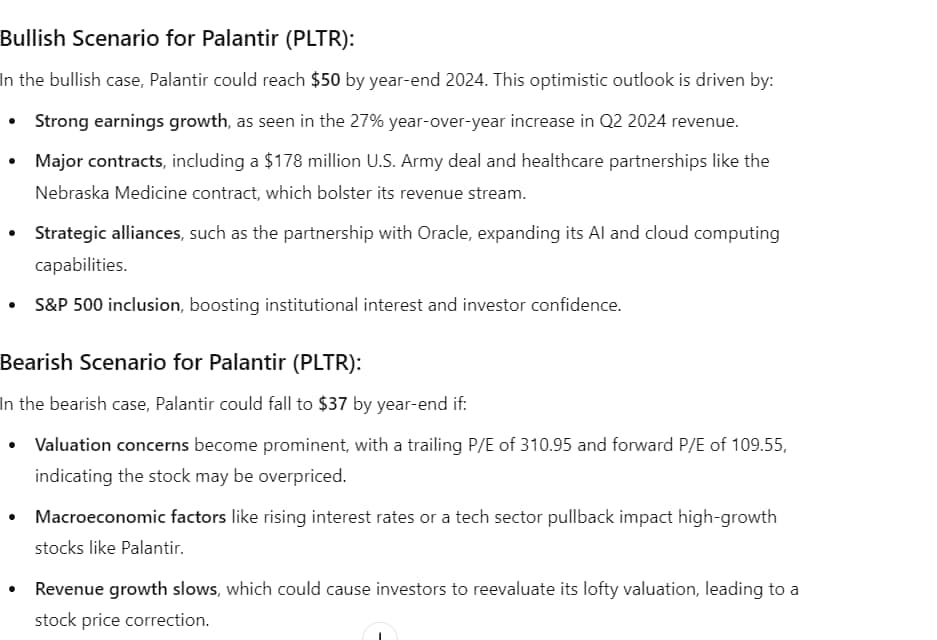

Palantir’s inclusion in the S&P 500 on September 23 added further momentum, pushing its stock to a record high of $43.87 on October 10, 2024. With robust earnings and strategic partnerships fueling its rise, investors are now left wondering how far Palantir can go by the end of the year.

In fact, Palantir shares have surged 25% in just the past month, boosting their year-to-date (YTD) increase to an impressive 156.76%. This strong performance leaves investors optimistic about the company’s future trajectory.

AI prediction: Palantir stock to hit $50 by year-end

To provide insight into Palantir’s future, Finbold consulted OpenAI’s AI tool, ChatGPT-4o, which projects Palantir stock to trade between $37 and $50 by the end of 2024.

In the bullish outlook, the model predicts Palantir’s stock could rise to $50 by the close of 2024, which hinges on several factors, such as robust earnings, high-profile contracts, and strong investor sentiment following its inclusion in the S&P 500.

Given its momentum and growing role in the AI space, Palantir appears poised for continued growth, although challenges such as revenue consistency could influence the final outcome.

On the flip side, if Palantir experiences a slowdown in revenue growth or broader market conditions turn unfavorable for high-growth tech stocks, the stock could retrace to $37. With its current high valuation, the stock is more likely to fall if earnings or growth don’t meet expectations

Factors influencing Palantir’s price surge

In Q2 FY 2024, Palantir reported a 27% YoY revenue increase, pulling in $678.1 million. The company’s expanding contracts in government and healthcare sectors continue to drive sustained growth.

Palantir’s upcoming earnings date on October 31, 2024, will provide a clearer view of its financial outlook, and the results could act as a catalyst for further price action.

Palantir’s contract pipeline also remains robust, with key projects such as the $99.8 million U.S. military deal and the $178 million U.S. Army contract for Project TITAN, a battlefield AI system. Palantir is also making strides in healthcare, having secured a multi-year contract with Nebraska Medicine to implement its AI-driven Foundry platform.

“Palantir will continue to work with Nebraska Medicine by providing AI software to help orchestrate patient flow, nurse allocation, clinical supplies management and revenue cycle optimization at scale, while expanding Nebraska’s Medicine core Foundry Ontology to additional high-priority areas through a single connected platform”

Source: Palantir Technologies Inc.

The company’s recent partnership with Oracle (NYSE: ORCL) to enhance cloud computing capabilities further underscores its growth potential. Palantir’s collaboration with Oracle enables it to scale AI solutions faster, leveraging cloud infrastructure to serve more clients in various sectors.

The company’s recent acquisition of an 8.7% stake in EV startup Faraday Future also highlights its diversified interests, with any recovery by the EV startup potentially boosting Palantir’s valuation further.

Bulls vs. Bears: Can Palantir keep growing?

While bulls are excited about Palantir’s improved profitability and strategic deals, there are concerns among some investors about whether the company can maintain its current growth trajectory.

The forward price-to-sales ratio of 23.57 suggests high expectations for continued growth. Any slowdown in revenue growth could lead to a significant pullback. The trailing P/E ratio of 310.95 and forward P/E ratio of 109.55 further highlight that Palantir is expensive relative to earnings, raising questions about sustainability.

Moreover, Palantir’s relatively low free cash flow yield of 0.71% further adds to these concerns. While the company continues to reinvest in its growth, it hasn’t yet shown the kind of free cash flow generation that would justify its current market value in the eyes of more conservative investors.

In conclusion, with an AI-predicted price target of $37 to $50 by year-end, Palantir appears to be on track for continued upward momentum.

However, concerns about its high valuation and the sustainability of its revenue growth loom large. Investors should closely monitor upcoming earnings reports and revenue trends, as these will be crucial in determining whether Palantir can justify its current lofty valuation.