PayPal (NASDAQ: PYPL) is once again in the spotlight as analysts evaluate its trajectory heading into 2025. With its fourth-quarter earnings report set for February 4, investors are closely watching whether the fintech giant can sustain its recent rebound amid lingering uncertainties.

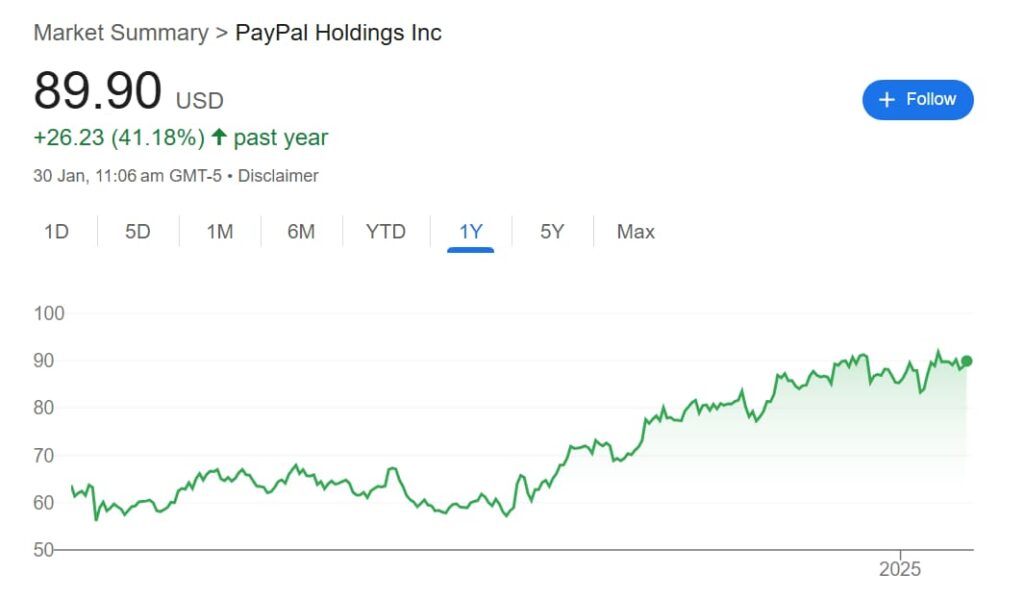

Over the past year, PayPal’s stock has surged nearly 40%, trading at $89.90 at the press time. However, despite the recovery, the stock remains more than 70% below its 2021 all-time high of $308.53.

PayPal’s key growth drivers

PayPal remains a major player in digital payments, processing transactions worldwide. However, growing competition from Apple Pay and emerging fintech firms has forced the company to shift its focus from traditional e-commerce tools and peer-to-peer transfers.

While its active user accounts have held steady at nearly 432 million, PayPal is focusing on increasing transaction volumes and deepening customer engagement. Recent partnerships with Amazon (NASDAQ: AMZN) and Shopify (NYSE: SHOP) have strengthened its position.

By integrating PayPal into Amazon’s ‘Buy with Prime’ program and handling U.S. credit and debit card transactions for Shopify, the company is expanding its presence in the online payments space.

To counter margin pressures, PayPal has rolled out Fastlane, a one-click checkout feature designed to reduce cart abandonment and compete directly with Apple Pay and Shopify’s Shop Pay. Launched in August, Fastlane has already gained traction, with fintech platform Adyen introducing it to U.S. businesses.

Partnerships with Fiserv and Global Payments have further strengthened PayPal’s foothold in digital commerce,

Moreover, PayPal’s expansion into cryptocurrency services marks a bold move in tapping into the growing retail demand for digital assets.

Analyst outlook: A battleground stock with catalysts in play

Amid these shifts, investment firm Bernstein has raised PayPal’s price target to $94 from $90, describing it as a ‘catalyst-rich battleground stock in 2025.’ However, the firm remains divided, citing a mix of positive catalysts and lingering challenges.

Analyst Harshita Rawat highlights several positive catalysts, including gains from expanded merchant solutions, operational efficiencies, and a new management team driving improved execution. PayPal’s strong cash reserves also support buybacks, and its valuation remains reasonable at 18 times the price-to-earnings (P/E) ratio for 2025, making it a valuable fintech play.

“PayPal is a catalyst-rich battleground stock in 2025. The stock path, however, is uncertain in 2025 due to the push/pull dynamics around intense competitive pressures on the cash-cow branded business on one hand, and tailwinds from buybacks/opex cuts, OVAS (ex float), new strong management team, incrementalism (with improved product velocity and execution) on the other hand.” – Harshita Rawat

Yet, significant headwinds persist. PayPal’s branded checkout business, a key profit driver, faces increasing competition from Apple Pay. Further risks include tax policy uncertainties and lower interest rates, which could weigh on gross profit growth.

With its fourth-quarter earnings report on February 4 and investor day set for February 25, all eyes are on PayPal’s ability to sustain its recovery and drive long-term growth.

Whether it emerges as a long-term winner or remains a battleground stock will depend on its ability to navigate intense competition in the digital payments space.

Featured image via Shutterstock