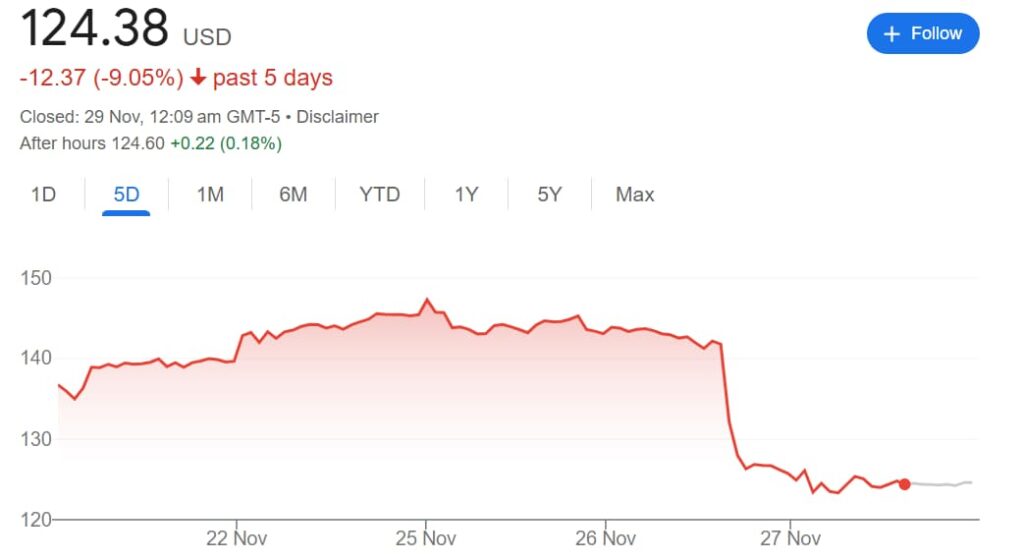

Dell Technologies (NYSE: DELL) faced a sharp selloff on November 27, with its shares dropping 11% following the release of mixed Q3 earnings results.

While the company delivered better-than-expected earnings per share, its cautious revenue forecast for Q4 and softer-than-expected sales in certain segments sparked investor concerns.

Despite the drop, analysts remain largely optimistic about Dell’s long-term growth, driven by its strong position in artificial intelligence (AI) infrastructure.

At the close of the latest trading session, Dell was trading at $124, ending the day down 12%. This marked a 9% weekly decline, though the stock remains up 66% year-to-date.

Earnings beat and revenue miss

Dell reported adjusted earnings per share of $2.15, exceeding analysts’ expectations of $2.06. However, revenue came in at $24.4 billion, slightly below the forecast of $24.7 billion. Despite this miss, total sales grew 10% year-over-year, driven by impressive performance in certain segments.

The Infrastructure Solutions Group (ISG), which includes server and networking solutions, saw a significant 34% year-over-year increase in revenue, with server and networking sales alone jumping 58%.

This growth reflects a strong demand for AI servers as enterprises increasingly invest in artificial intelligence infrastructure.

On the other hand, the Client Solutions Group (CSG), which includes PCs and similar devices, faced challenges, posting a 1% decline in revenue due to weaker consumer demand. While commercial client revenue rose by 3%, it wasn’t enough to offset the broader segment’s slowdown.

Profitability also improved, with non-GAAP adjusted profits increasing 14% and GAAP profits climbing 16% year-over-year. However, the disparity between GAAP earnings of $1.58 per share and non-GAAP results raised questions about Dell’s core profitability.

AI growth: A bright spot in the storm

The main driver of the stock’s decline was Dell’s Q4 revenue guidance, which the company expects to range between $24 billion and $25 billion, falling short of Wall Street’s consensus estimate of $25.57 billion.

This conservative forecast reflects multiple challenges, including continued PC demand weakness and enterprise server upgrade delays as customers wait for Nvidia’s (NASDAQ: NVDA) next-generation Blackwell chips.

Despite these headwinds, Dell highlighted a record $3.6 billion in AI server orders for Q3, with its AI product pipeline growing by over 50%. COO Jeff Clarke emphasized Dell’s strategic focus on AI, calling it a significant and growing opportunity, reflecting confidence in the company’s long-term growth

“AI is a robust opportunity for us in both ISG and CSG and interest in our portfolio is at an all-time high, with no signs of slowing down. That said, this business will not be linear, especially as customers navigate an underlying silicon roadmap that is changing.”- Jeff Clarke

Analysts maintain optimism, adjust price targets

In response to Dell Technologies’ mixed Q3 earnings report and cautious Q4 guidance, several analysts have revised their price targets while maintaining a positive outlook on the company’s long-term potential.

Mizuho’s Vijay Rakesh lowered the price target to $150 from $155 following the earnings report but reiterated an “Outperform” rating, citing Dell’s strong positioning in AI servers and the PC refresh cycle as key growth drivers through 2025.

Meanwhile, Melius Research’s Ben Reitzes raised his target to $155 from $140 and maintained a Buy rating, describing the Q4 outlook as a temporary “blip” while highlighting improving margins and growing demand for 2026.

Adding to the bullish sentiment, Citigroup’s Asiya Merchant raised the target to $160 from $156, reiterating a Buy rating and emphasizing record-breaking AI server demand.

Similarly, Evercore ISI’s Amit Daryanani kept a Buy-equivalent Outperform rating with a $150 price target, underscoring opportunities in Dell’s high-efficiency AI server sales.

Long-term growth potential

While the stock’s sharp decline reflects immediate concerns over weak PC sales, delayed server upgrades, and softer Q4 forecasts, Dell’s leadership in AI infrastructure points to strong long-term potential.

The company’s record-breaking AI server demand and expanding product pipeline highlight its ability to capitalize on the growing demand for AI-driven solutions.

With strategic investments and a solid foothold in infrastructure solutions, Dell is positioned to remain a leader in the evolving AI landscape. Despite short-term challenges, its focus on innovation makes it an attractive option for long-term investors.

Featured image via Shutterstock