Eli Lilly (NYSE: LLY), one of the U.S.’s foremost pharmaceutical giants, faced a sharp 8% drop in its stock price after reporting disappointing third-quarter results, erasing nearly $70 billion from its market value.

The pharmaceutical giant missed both earnings and revenue expectations, prompting several analysts to lower their price targets.

At the time of writing, LLY stock is down over 8% in the 5-day chart to its press-time price of $818.

Sales miss sparks investor concerns

Eli Lilly posted adjusted earnings of $1.18 per share for the third quarter, well below Wall Street’s forecast of $1.47. Revenue came in at $11.44 billion, missing the projected $12.11 billion.

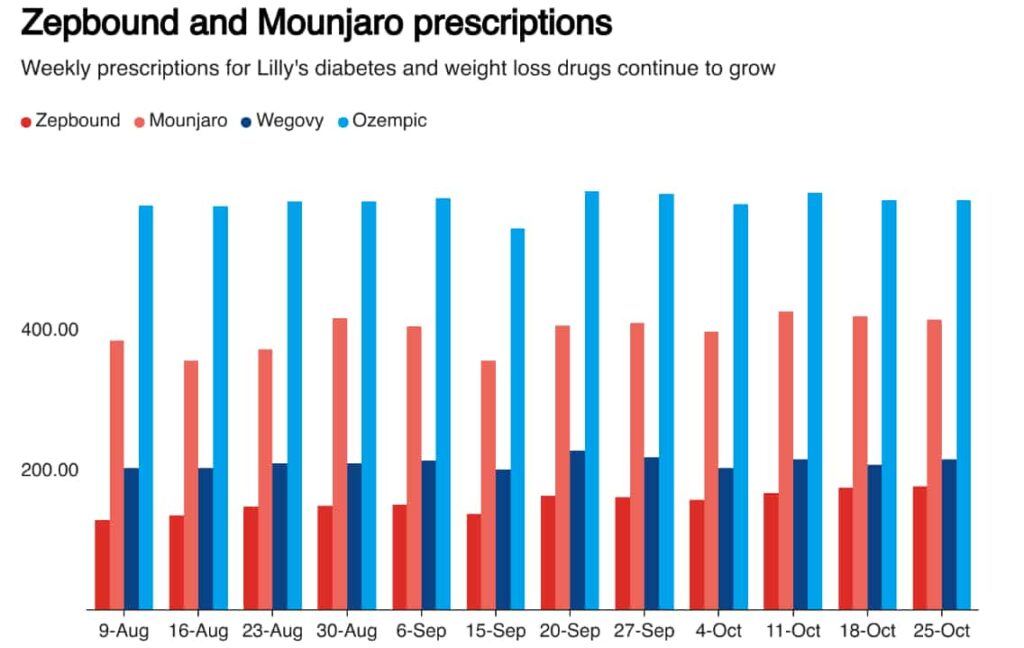

Much of the shortfall largely stemmed from weaker-than-anticipated sales of its blockbuster drugs, Mounjaro and Zepbound.

Mounjaro, a diabetes drug, brought in $3.11 billion, while the weight-loss drug Zepbound generated $1.26 billion in sales. Both figures missed analysts’ expectations of $4.20 billion and $1.69 billion, respectively.

Eli Lilly CEO David Ricks attributed the sales miss primarily to inventory management by wholesalers and retailers rather than a decline in demand.

He said that these downstream customers made independent decisions on how much of each dosage form to stock, driven largely by physical constraints, particularly the limited capacity of cold chain storage.

“I think what we really don’t control and don’t attempt to, but as a reality, is that downstream customers from Lilly—wholesalers and retailers—are making their own decisions about which of the 12 different dosage forms they want to stock and at what level. There are some physical constraints to that. Cold chain capacity is constrained.

– David Ricks

Despite the sales miss, prescriptions for Zepbound surged, averaging 140,000 per week in Q3, up from just over 93,000 in the previous quarter, according to IQVIA data reported by Reuters.

To address supply stability in the U.S., Eli Lilly delayed its advertising and international launch of Zepbound. Ricks indicated that promotional efforts are set to begin in November, which could help reignite demand.

In light of these issues, Eli Lilly revised its full-year guidance, now projecting adjusted earnings of $13.02 to $13.52 per share, down from the previous $16.10 to $16.60. The revenue forecast has been lowered to between $45.4 billion and $46 billion from a prior estimate of up to $46.6 billion.

Adding to the quarterly woes, a $2.8 billion charge related to the acquisition of Morphic Holding dented results further.

Analysts slash price targets, but long-term confidence remains

Analysts responded to the mixed earnings by revising their outlook on Eli Lilly’s stock.

JPMorgan maintained an ‘Overweight’ rating but reduced its price target to $1,100, citing the dip in the stock as a buying opportunity.

The firm expressed confidence in the company’s long-term growth, anticipating a significant sales rebound in the fourth quarter as Eli Lilly ramps up promotional activities.

Deutsche Bank also lowered its price target to $1,015 while reiterating a ‘Buy’ rating, highlighting continued strong demand for the company’s GLP-1 drugs despite the inventory-driven sales miss.

Similarly, BofA reduced its target to $1,100 from $1,150 but remained optimistic about Eli Lilly’s future prospects, noting that the sales miss was inventory-related rather than demand-driven.

Looking ahead, Eli Lilly is poised to bounce back. With marketing efforts for Zepbound kicking off in November and strong underlying demand for its flagship drugs, the company is expected to regain momentum in the quarters ahead.