SoFi Technologies (NASDAQ: SOFI) has drawn significant attention from analysts following its Q4 2024 earnings report and cautious fiscal guidance for 2025.

While the fintech giant exceeded Wall Street expectations on revenue and earnings for the fourth quarter, concerns about profitability have led to divergent analyst outlooks and a sharp decline in its stock price.

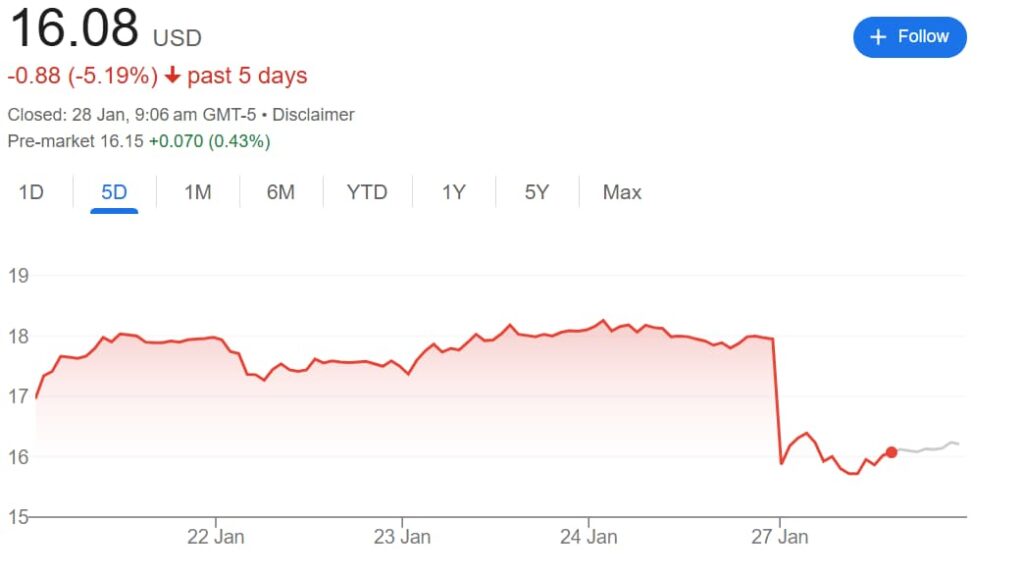

Shares of SoFi dropped over 10% to close at $16.08 on January 27, marking a 5% decline over the past five days and cutting into gains accumulated earlier in the year.

Despite the recent pullback, the stock remains up 13% year-to-date. On a broader scale, SoFi has soared 44% in the past three months and 76% over the past year, showing strong investor confidence in the company even amid short-term volatility.

SoFI strong Q4 performance, clouded by FY2025 guidance

SoFi reported adjusted net revenue of $739.1 million for Q4, a 24% year-over-year increase, well above the analyst consensus of $674.6 million. Adjusted earnings per share rose 150% to $0.05.

CEO Anthony Noto described 2024 as the company’s ‘best year ever,’ with record member additions of 785,000 and over 1.1 million new product additions in the quarter.

However, the company’s Fiscal Year 2025 (FY2025) guidance has raised investor concerns. For the first quarter of 2025, SoFi anticipates adjusted net revenue between $725 million and $745 million, exceeding Wall Street projections of $699 million. However, its EPS forecast of $0.03 falls short of analysts’ expectations of $0.06.

The company also expects adjusted EBITDA to range from $175 million to $185 million, below the consensus estimate of $192 million, highlighting challenges in meeting profitability targets.

Diverging analyst views on SoFi’s prospects

The mixed results and guidance have prompted analysts to revise their price targets, with contrasting views on SoFi’s growth potential and near-term challenges.

Bank of America analyst Mihir Bhatia raised the firm’s price target to $13 from $12 but maintained an ‘Underperform rating.’ Bhatia noted SoFi’s Q4 performance showed impressive revenue upside driven by customer acquisition, albeit at higher near-term costs.

The analyst noted that SoFi’s shares appear priced for perfection, making other opportunities in the sector more attractive.

Conversely, Needham analyst Kyle Peterson expressed a more optimistic outlook, raising the price target to $20 from $13 and reiterating a ‘Buy’ rating.

Analyst Kyle Peterson highlighted SoFi’s strong Q4 performance, driven by higher net interest income and a non-recurring tax benefit that boosted capital ratios.

Peterson viewed the 10% pullback in shares as a buying opportunity, emphasizing future growth from high-profile deals such as the U.S. Treasury Direct program and capital-light tailwinds from a major loan platform deal with Blue Owl Capital, both expected to contribute meaningfully by FY2026.

“While the results were strong, the shares pulled back ~10% yesterday due to a light profitability outlook, which we attribute to the ramping of some high-profile deal wins (US Treasury Direct program, hotel co-brand win), expected to be bigger contributors in FY26 and beyond.”

– Kyle Peterson

JPMorgan, meanwhile, maintained a Neutral stance with a $16 price target. While acknowledging strong Q4 revenue and adjusted EBITDA that exceeded expectations, the firm raised concerns over FY2025 EBITDA guidance, which fell short of Street estimates as the company emphasized plans to reinvest earnings into the business.

Nevertheless, JPMorgan recognized record member growth and originations as positive indicators, though this momentum was overshadowed by near-term profitability concerns.

“On the bright side, full-year revenue growth guidance of ~25% came in well ahead of estimates. All told, it was a strong quarter highlighted by record Member growth and originations, though overshadowed, at least for the near term, by soft EBITDA guidance.”

That being said, the recent pullback in SoFi’s stock could offer a compelling entry point for long-term investors. However, near-term profitability challenges continue to cast uncertainty over its outlook.

Featured image via Shutterstock