Banking giant UBS has reaffirmed its bullish stance on Nvidia (NASDAQ: NVDA), citing strong long-term demand visibility and sustained margin strength.

In a March 2 note, analyst Timothy Arcuri reiterated a ‘Buy’ rating on the stock with a $245 price target, implying nearly 40% upside.

The update followed meetings with Nvidia CFO Colette Kress, after which UBS expressed greater confidence in the company’s networking expansion and long-term profitability.

Arcuri said hyperscale cloud providers are already planning 2027 compute capacity expansions, with current demand pointing to another strong year.

UBS added that solid balance sheets and cash flows allow hyperscalers to invest ahead of revenue growth and AI profits, echoing the cloud infrastructure buildout of the past decade.

Nvidia’s management noted that financing for large infrastructure projects is expanding beyond traditional capital expenditures to include leases, special-purpose vehicles, and other structures, giving hyperscalers more flexibility to sustain growth.

At the same time, UBS identified Nvidia’s accelerating networking business as a key growth driver, noting the company views itself as the largest global networking player and aims to surpass the combined revenue of all other networking semiconductor suppliers by year-end.

Wall Street bullish NVDA shares

On margins, Nvidia expects product performance advantages to support profitability, but does not see gross margins exceeding 75%. UBS maintained its 2027 and 2028 earnings per share estimates at about $12.50 and $15.

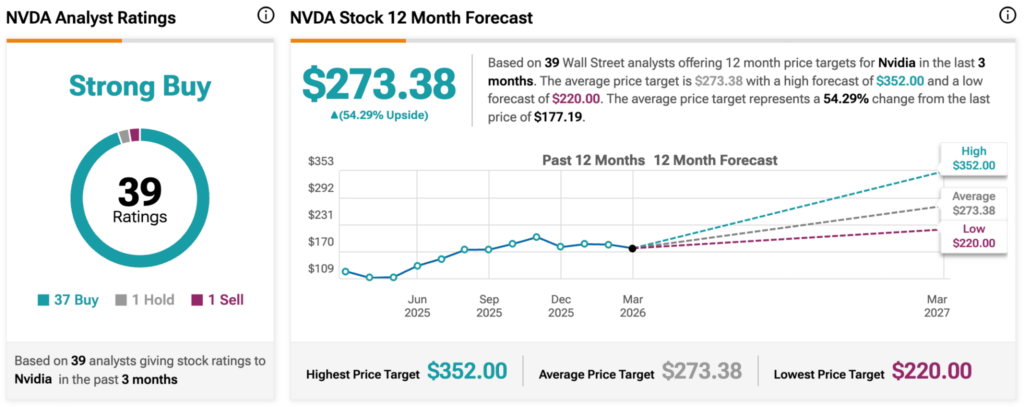

Across Wall Street over at TipRanks, Nvidia holds a ‘Strong Buy’ consensus based on 39 analyst ratings: 37 recommend buying, one suggests holding, and one advises selling.

The average 12-month price target is $273.38, implying about 54% upside from the last traded price. Targets range from $220 to $352.

Nvidia stock fundamentals

Overall, the semiconductor giant continues to post strong fundamentals. In its February 25 earnings report, the company delivered record quarterly revenue of $68.1 billion, up 73% year over year and 20% sequentially. Data center revenue rose 75% annually to $62.3 billion on robust AI chip demand.

Nvidia also announced a strategic partnership with Coherent to advance optics technology for next-generation data centers, including a $2 billion investment to expand supply, research and development, and U.S.-based manufacturing.

Demand for its Blackwell GPUs remains strong, driving record data center growth and supporting nearly 9 gigawatts of infrastructure deployments across hyperscalers, enterprises, and sovereign clients.

Despite these strengths, the stock faces near-term pressure from broader market rotations, profit-taking after its post-earnings rally, and concerns about the durability of AI spending.

Finally, geopolitical risks, including potential China sales restrictions and export controls, continue to cloud the outlook.

Featured image via Shutterstock