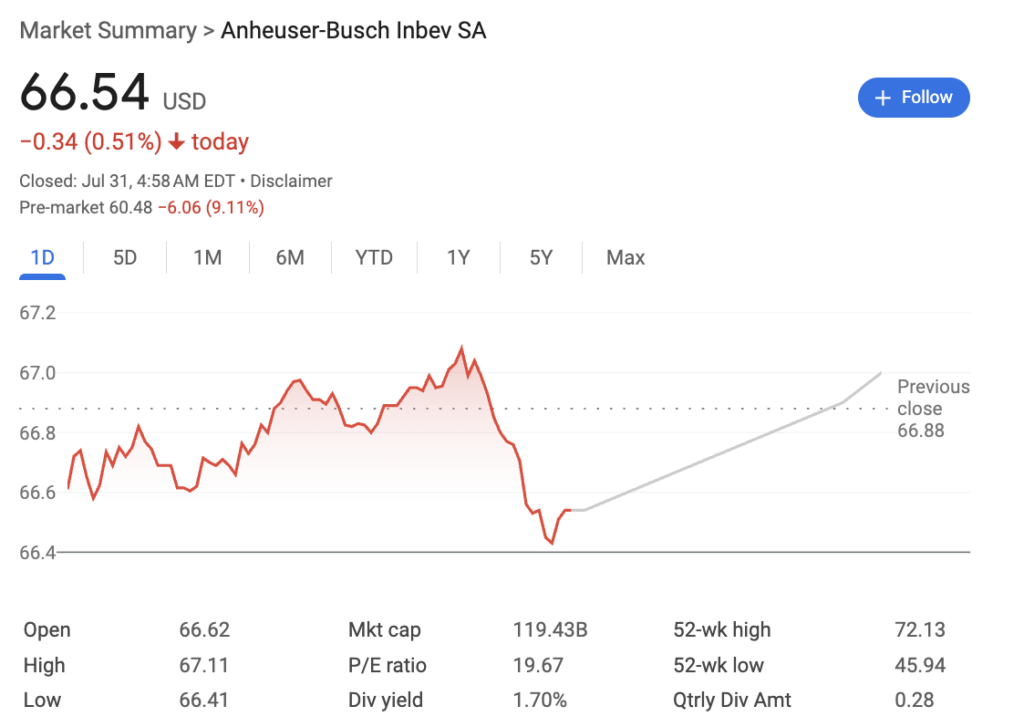

Anheuser-Busch InBev (NYSE: BUD), the parent company of Bud Light, reported mixed second-quarter results on Thursday, July 31, that failed to impress investors despite revenue growth of 3.0% to $15.004 billion and normalized EBITDA gains of 6.5%.

The stock fell 9.1% in pre-market trading, marking its worst session since the COVID-19 pandemic.

The decline came as the world’s largest brewer missed expectations on beer volumes, the metric that matters most for beverage companies since it shows whether people are actually drinking more or less of your products, stripped of pricing effects and financial maneuvering.

Volume miss, led by China and Brazil

AB InBev’s beer volumes declined 1.9% year-over-year during the quarter, significantly worse than the 0.3% decline analysts had forecast. The miss on this crucial metric overshadowed otherwise solid financial performance.

The problems were concentrated in two major markets. China saw volumes plunge 7.4%, with the company admitting it was “underperforming the industry.” Meanwhile, Brazil wasn’t much better with a 6.5% decline that AB InBev blamed on tough comparisons with last year and bad weather.

Despite the volume challenges, the company demonstrated pricing power by growing revenues while selling less beer. Normalized EBITDA exceeded expectations, rising 6.5% with margin expansion of 116 basis points to 35.3%.

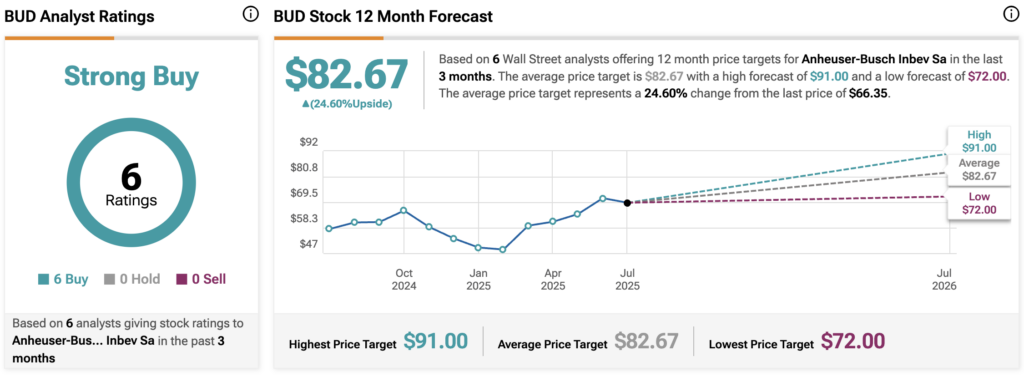

Wall Street price targets as high as $91

According to market analysis platform TipRanks, the average target price for BUD sits at $82.67 for the next 12 months, while the most optimistic analysts predict it could go as high as $91.00. The most bearish outlook, on the other hand, sees the stock reaching $72.00.

Based on six analysts covering the stock, all maintain Strong Buy ratings with no Hold or Sell recommendations among them. No analysts have updated their price targets following Thursday’s earnings release at 7 AM CET.

Featured image via Shutterstock.