Take-Two Interactive (NASDAQ: TTWO) shares fell after Rockstar confirmed another delay to Grand Theft Auto VI, shifting the launch to November 19, 2026.

The announcement came with a statement acknowledging the already extended development timeline, noting that the additional months are intended to ensure the final game meets Rockstar’s typical level of ‘polish.’

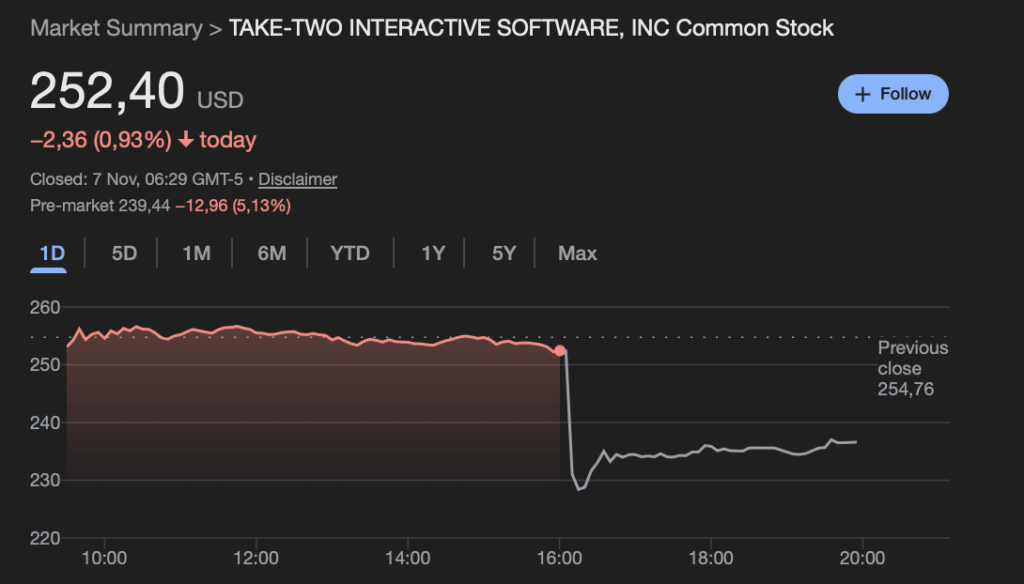

Notably, the update on the latest GTA triggered a sharp reaction in the market trading, with an initial drop of up to 18% after news of the delay circulated. Currently at the time of publication TTWO stock is down over 5% in pre-market.

Take-Two Q2 earnings

The setback arrived alongside otherwise strong fiscal second-quarter results. Take-Two reported adjusted earnings per share of $1.46 compared to analyst expectations of $0.94 , on revenue of 1.96 billion dollars against a consensus view of $1.74 billion.

Net bookings also reached $1.96 billion, up 33% year over year. Recurrent consumer spending rose 20 percent and now accounts for 73% of total bookings, supported by titles including NBA 2K26, Mafia: The Old Country, and several mobile franchises. However, the GTA VI delay overshadowed the earnings performance and remains the primary variable in investor sentiment.

Wall Street TTWO stock price targets

Recent price target updates include Jefferies, Benchmark, and DA Davidson, all holding Strong Buy ratings and guiding toward a $300 target. Wells Fargo maintains a Buy rating with a revised target of $277, while CICC initiated coverage at $272. The consensus across major research desks continues to frame Take-Two as a beneficiary of long-cycle franchise economics, even with extended development timelines.

The critical question now shifts from delay reaction to launch valuation. Based on historical price behavior leading into prior Rockstar releases, combined with a larger global install base and higher-margin digital sales, ChatGPT-5 forecasts Take-Two trading at approximately $247.50 on November 19, 2026, assuming GTA VI launches on schedule and receives broadly favorable reception.

That scenario reflects a re-rating in forward earnings expectations rather than speculative momentum. If the title is delayed again, shares would likely retrace toward the mid-$160s before consolidating ahead of a new schedule.