While most investors have been focusing on oil and its derivatives amidst the Iran War, major U.S. hedge funds have been quietly making bets on an entirely different commodity: food.

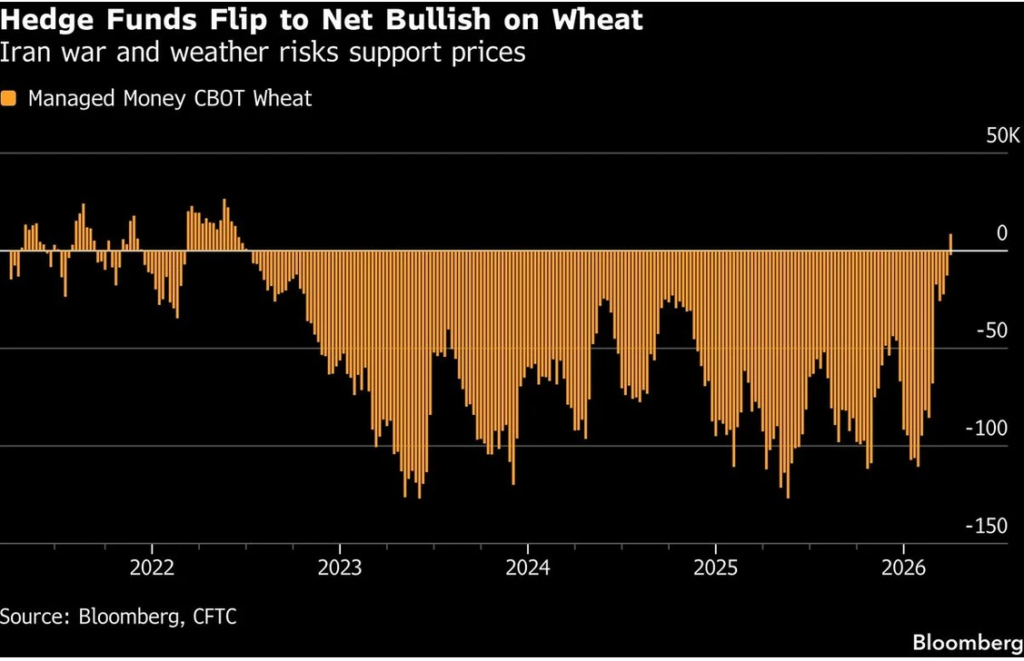

Specifically, March saw a major reversal in the attitude toward wheat, per the data published by the Commodity Futures Trading Commission (CFTC). Indeed, the number of long positions exceeded the number of short bets by 8,641 contracts, per an April 6 Bloomberg report.

Overall, there were 117,375 bullish and 108,734 bearish bets in Chicago at the end of the previous month.

Such a market setup represents a substantial reversal to the net short balance that has been active since 2022 as food abundance continued pressuring the world’s agriculture sectors.

Why Hedge Funds are going long on wheat

The change in attitude toward wheat prices among hedge funds can be linked directly to the Iran war and the effective blockade of the Strait of Hormuz.

At the surface level, the halt to traffic in a waterway responsible for approximately 20% of the world’s crude supply has led to substantial price increases both for the American WTI standard and the British Brent, and led both to ongoing and anticipated shortages of various types of fuel.

Under the circumstances, food prices were expected to run higher even based solely on the mounting costs of products such as the diesel needed to run agricultural machinery.

Simultaneously, the Persian Gulf is responsible for the production of numerous other resources necessary for the global economy, with fertilizer – along with LNG and helium – being among the most important.

So far, farmers have been reportedly scrambling both to acquire sufficient fertilizer and to pivot production to crops that are less dependent on nutrients.

Elsewhere, weather also contributed to the rising prices and fears of looming shortages as there was a period of prolonged dryness in the US Plains, expected to break only in the second week of April.

Why wheat prices are likely to remain elevated through 2026

Lastly, at press time, there appears to be little chance of the supply chain issues easing significantly in the short term. While the financial markets reacted rapidly and positively to the latest rumors of ongoing negotiations, an end to hostilities appears out of sight.

Furthermore, even if a ceasefire is reached, many of the production facilities in the Persian Gulf would require weeks, months, or even years to get repaired and to restart production, meaning that the reopening of the Strait of Hormuz would only be the start of a long journey toward recovery for the global economy.

Featured image via Shutterstock