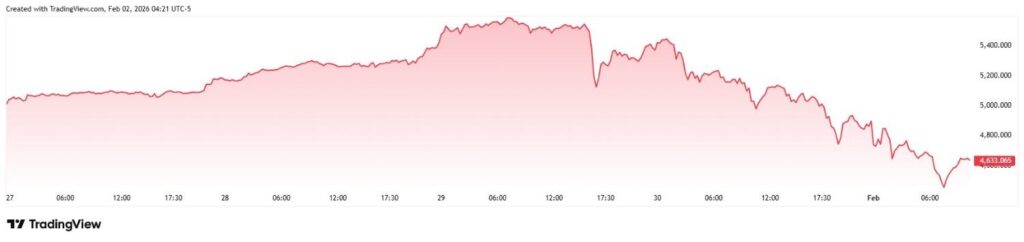

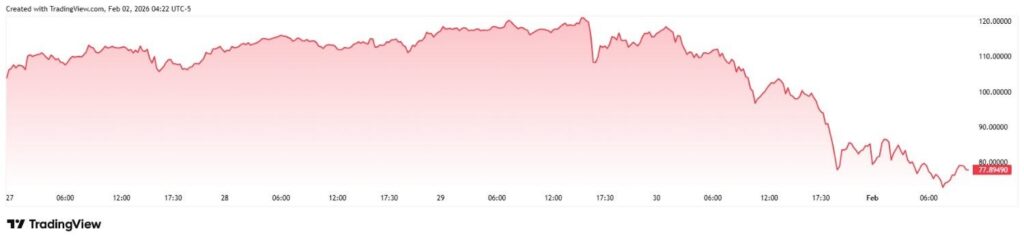

The two main traditional ‘safe haven’ assets – Gold and Silver – underwent a massive bloodbath in late January and early February after previously rallying to a series of new all-time highs (ATH) in early 2026.

Together, the two precious metals annihilated an estimated $8 trillion from their market capitalization in just three days as they fell to their press time prices of $4,533 for Gold and $77 for Silver on Monday, February 2.

Gold accounted for approximately $5.5 trillion of the commodity market wipe, given that there is an estimated 216,265 tons of the metal above ground.

Silver, despite suffering a greater drop from about $118 to $77, is responsible for the erasure of some $2.5 trillion, assuming the 1.6 million ton estimate is correct.

Still, it is worth noting that the above-reserve reserves for both commodities are relatively unreliable estimates, meaning the actual losses could be trillions of dollars larger or smaller.

While gold’s nearly $1,000 and silver’s $30 crash – both larger than the typical annual commodity moves – are alarming in their own right, perhaps the greater concern is from the wider pattern seen across the financial markets.

What Gold and Silver crash means for investors

The two precious metals tend to rise in a climate of economic uncertainty as they are seen as a way to store value securely, and they usually stagnate or fall during a boom as investors are transferring their wealth into riskier investments with a greater growth potential.

Although such a traditional pattern would otherwise present good news for investors and workers, the two hedge commodities have been maintaining a high correlation with some of the riskiest assets in the world.

Specifically, recent trading witnessed cryptocurrencies like Bitcoin (BTC), the S&P 500 benchmark stock market index, and ‘safe haven’ gold and silver all crash simultaneously.

Along with being unusual, the move is odd as no clear trigger for the downfall can be easily identified.

Is the Fed behind the Silver and Gold crash?

Thus, it appears likely that a mix of factors is behind the bloodbath. Perhaps the chief and most direct reason for the downturn can be found in President Donald Trump selecting Kevin Warsh as Jerome Powell’s successor at the Federal Reserve.

Warsh is an especially sensitive nomination since his name only served to increase uncertainty. President Trump’s conflict with Powell largely stems from the commander-in-chief’s desire to lower rates and introduce a more dovish Fed.

Historically, Kevin Warsh has been a fiscal hawk, opposed to many of the Federal Reserve’s market-stimulating actions.

Beyond the turmoil at the Fed, numerous other factors have likely been contributing to the price crash.

The U.S. Government entered a partial shutdown at the end of January and, at the same time, a new contingent of the Epstein Files implicated numerous political heavyweights and captains of industry in highly disturbing activities, albeit largely via allegations of uncertain veracity.

How global tensions fed into market instability

Externally, the rift between the U.S. and its allies remains open following President Trump’s most recent round of posturing regarding the annexation of Greenland, and the American armed forces appear to be amassing for an assault on Iran.

Lastly, and perhaps as importantly as the other factors, investors themselves have likely been exceptionally jittery and eager to sell.

The deep uncertainty about the future of the economy that arose from the simultaneous sale of risk-on and risk-off assets has been relevant in other forms for years, especially as various recession indicators kept flashing their warnings despite the markets continuing to record multiple new all-time highs.

Featured image via Shutterstock