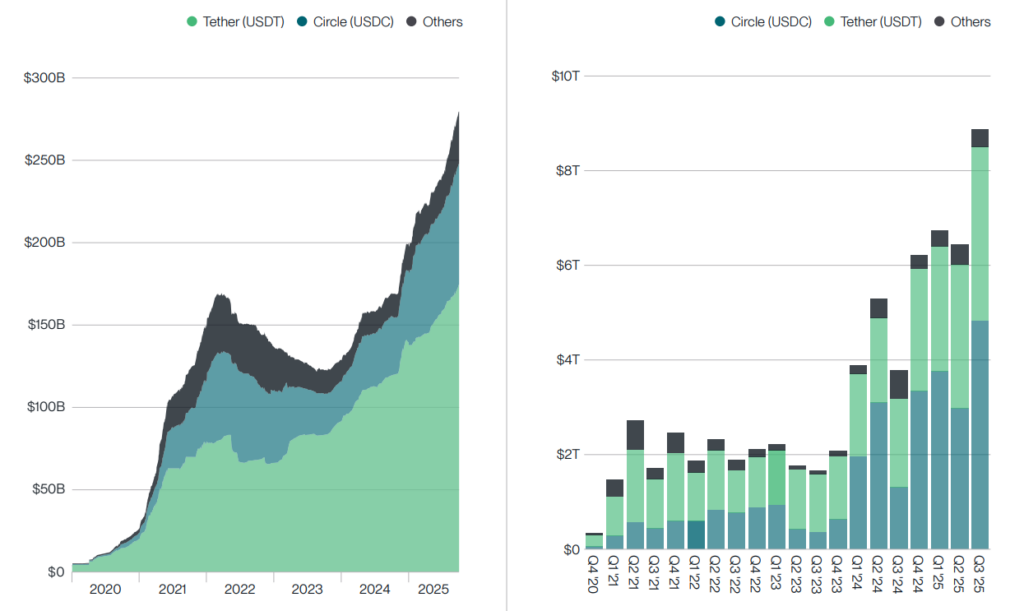

Despite the immense technological and social promise put forth by stablecoins (i.e., digital assets pegged to fiat), scaling payments using this asset class, particularly at an enterprise level, has been quite challenging. Regardless, settlement volumes have continued to explode, with on-chain stablecoins facilitating $33 trillion worth of transactions last year, quite handily beating the annual throughput of giants like Visa, which handled $16.7 trillion during the same time period.

If that wasn’t enough, as of Q3 2025, stablecoins accounted for roughly 30% of all on-chain crypto transactions globally, with over $4 trillion moved in just the first seven months of the year (an 83% year-on-year increase). Even during the current market slump, which started last December, stablecoin usage has continued to hit new peaks seemingly every other week.

Fig1. Stablecoin market capitalization Fig2.Stablecoin Transaction Volumes (source: Bitwise)

Making speed, cost, and global reach accessible for everyone

From the outside looking in, the most efficacious use case for stablecoins in enterprise payouts centers on efficiency and reach because transactions that once took days via legacy rails can now be settled in seconds, unhindered by banking hours or holidays. Similarly, fee rates that clients have dished out thanks to multiple bank jumps and systems like SWIFT have been fractionized.

To this point, McKinsey analysts have posited that non-traditional providers leveraging stablecoin rails charge approximately. one-fifth of the fees of traditional players, indirectly translating into major cost savings for the end user.

Moreover, because stablecoins operate on a borderless infrastructure, an Internet connection and a digital wallet are all that’s needed to receive funds. This is a game-changer for the unbanked as well as contractors/customers working in emerging markets.

From a regulatory aspect, too, there have been numerous laws that have helped push forth this change of guard. For starters, last year the United States government passed its first comprehensive stablecoin law (the GENIUS Act) so as to open the floodgates for stablecoins in cross-border payments.

Simultaneously, the European Union’s MiCA framework also came into effect last year, with jurisdictions like Hong Kong, the UAE, Japan, and Singapore also introducing their own stablecoin rules in parallel.

An enterprise-grade stablecoin payout system by OpenPayd

With the industry racing to bridge the gap between crypto’s promise and enterprise reality, players like OpenPayd have devised future-ready, end-to-end solutions to serve such long-standing issues. The London-based fintech infrastructure provider operates reliably at scale, supporting millions of transactions per month and high-value settlements, all via a single API and unified governance framework that meets strict treasury and compliance standards.

The platform’s overarching theme from the get-go has been “rail-agnosticism,” with early adopters having found success by dynamically routing each payout through the optimal rail (be it traditional bank networks, alternative payment methods, or blockchain) based on aspects like different corridors, cost, speed, and risk considerations.

To put it simply, every transaction taking place via OpenPayd automatically switches between SWIFT, local bank transfers, or blockchain networks depending on which is optimal, thus avoiding vendor lock-ins and improving reliability. As an example, if an on-chain network is congested or a banking route is down, the system fails over to alternatives without manual intervention.

Moreover, OpenPayd treats wallets like bank accounts, pairing them with virtual IBANs on the fiat side, making reconciliation and reporting far easier (as finance teams can easily see exactly which funds are where, and even automate daily sweeps of balances, all while preserving audit trails).

Another important facet of the platform is that it integrates compliance, such as sanctions screening, Travel Rule data capture, and on-chain analytics checks directly into the transaction pipeline. In layman’s terms, OpenPayd enforces the same safeguards as any other payment rail, a stance increasingly expected by most UK and EU regulators.

The impact is there for everyone to see

The approach outlined above has already yielded tangible results and recognition. As late last year, OpenPayd signed a partnership with Circle (issuer of the popular stablecoin USDC) to integrate the latter’s stablecoin infrastructure into its ecosystem platform.

As a result, the firm was able to merge its massive payments volumes (over €130 billion annually at the time) with on-chain USDC capabilities, enabling enterprise clients to seamlessly convert between fiat and the US Dollar. Not only that, earlier this year, the infrastructure provider won the “Best Early-Stage or Future Payments Initiative” award at the 2026 Cards and Payments Awards.

Therefore, as the journey towards enterprise-scale stablecoin payouts remains underway (fueled by a potent mix of improved technology, regulatory green lights, and real demand for better cross-border payments), it will be interesting to see how the use of these assets continues to become an even bigger part of the global finance ecosystem. Interesting times ahead!

Featured image via Shutterstock.