This guide takes a deep dive into the ETF vs Mutual Fund debate. We look at how the two assets compare, contrast and help you decide which one is better for your investment portfolio.

Introduction

When it comes to investments, traders and investors are spoiled for choice. There are several avenues to deploy their cash to work for them, including stocks, bonds, bills, funds, forex, and commodities. This list excludes more exotic investment opportunities such as cryptocurrencies or more traditional venues such as real estate. Still, however you look at it, there are tons of options from which to choose.

Including mutual funds and exchange-traded funds (ETFs) within your investment portfolio is an excellent way to cut down on your decisions. Instead of choosing between two stocks within the same industry, funds provide you the opportunity to invest in an entire sector or an index that tracks the performance of stocks within the same industry.

ETFs and mutual funds both serve the same purpose: diversification. But which one should you select among the two fund categories? Which one is better for your portfolio and why? As discussed in this guide, ETFs and mutual funds have several similarities, but they also differ in more ways than one. It is hard to generalize comparisons between ETFs and mutual funds since both can be subdivided into smaller subcategories. These smaller units tend to overlap in terms of features, properties, advantages, and drawbacks.

Continue reading to find out if an ETF or a mutual fund is better for your investment portfolio.

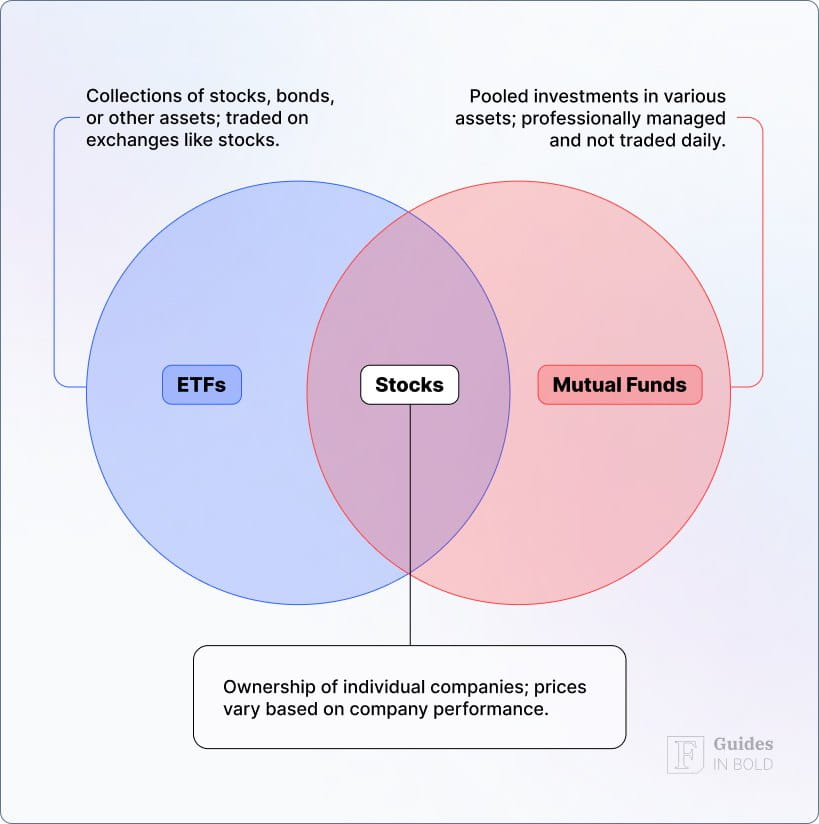

What is a Mutual Fund?

One major characteristic of mutual funds is that they are often actively managed by the fund managers who regularly rebalance the basket’s constituents to try and beat benchmark performance metrics. Because mutual funds are often actively managed, they tend to cost more in expense ratios and tax liabilities than their ETF counterparts.

What is an ETF?

ETFs are often passively managed, which contributes to their lower management costs, and these typically track the performance of an index such as the S&P 500. However, ETFs are increasingly becoming more diverse as fund managers create more actively managed funds that mimic several aspects of mutual funds.

ETFs vs Mutual Funds: Similarities and Differences between

1. Management

Fund management involves measuring the level of involvement an investment company has towards maintaining the fund after its creation. Mutual funds typically have a more involved fund manager compared to ETFs. For example, a fund management team includes researchers, analysts, and financial advisors, among others whose interaction would ideally lead to more informed decisions on what assets should constitute the basket.

On the other hand, most ETFs track indexes such as the S&P 500, requiring minimal maintenance, resulting in fewer team members within the management team. A few ETFs are more actively managed, which means that they are handled just like mutual funds are with a more active and engaged management team.

There is an overlap in terms of management when it comes to comparing ETFs vs. mutual funds. Even though most ETFs are passively managed, there are a few that are actively managed. Likewise, most mutual funds are actively managed, but some are created to track indexes and are thus, often passively managed.

2. Diversification

Diversification is perhaps the main reason why most funds exist. Investors need to reduce their market risk, and investing in several single stocks or assets is a great way to get whipped by the markets. ETFs and mutual funds often comprise a basket of assets such as multiple stocks, bonds, or commodities.

As an investor, you may believe that a particular industry is about to explode, but, of course, not all stocks rise at the same rate, and sometimes some may even fall. Funds provide a great way to hedge against the risk of uncertainty since they average out the performance of the entire basket.

For this reason, both ETFs and mutual funds are great diversification tools.

3. Pricing

At the creation stage, shares of both ETFs and mutual funds are priced by the investment companies that create them based on the net asset value (NAV) and the number of shares in each fund. After the creation, mutual funds are then priced every day at the close of the trading session by determining the NAV of the fund using the closing market prices of the assets within the basket.

Investors and traders cannot buy and sell shares of a mutual fund during regular trading hours, and any orders to purchase these shares are only fulfilled once the market closes. The fund manager thus determines the prices at the time of recalculation of the fund’s NAV.

On the contrary, ETF shares trade on the stock exchanges just like stocks giving investors and traders the chance to buy, sell and exchange the shares as often as they would like as long as the markets are open. It may seem like a great feature of the ETFs that demand and supply market forces determine their prices, but this can easily lead to over or undervaluation of the ETF shares compared to their NAV.

Suppose ETF shares are trading above or below their fund’s NAV. In that case, fund managers can correct this by either redeeming the shares to reduce their supply or creating more shares of the fund, thereby increasing or decreasing the price, respectively.

4. Commissions, Taxes and Expense Ratios

When it comes to investing in either ETFs or mutual funds, costs play a major role in what should belong in your portfolio and what shouldn’t. Generally, the reason for investing is to gain a profit or a justifiable return on your investment, and costs eat into your returns.

The expense ratio is the annual fee rate charged by the fund manager, and this typically varies from fund to fund. Mutual funds have been considered more expensive than ETFs for a long time due to higher expense ratios. This is because mutual funds are typically actively managed, while ETFs are more often passively managed. But now, you can find an ETF with a higher expense ratio than a comparable mutual fund if it is actively managed while the latter is passively managed.

Taxes contribute a significant chunk toward the total costs incurred in fund investment, and in this case, mutual funds are generally less tax efficient. Whenever the fund manager rebalances a fund’s basket, they could buy or sell assets, which constitutes a taxable event called capital gains tax. The tax liability is distributed amongst all shareholders regardless of whether they have sold any of their shares. Whatsmore, the structure of ETFs ensures that the tax liability from share trading is only attributed to the individual seller and not all shareholders within the fund, making it cheaper for an investor who holds their shares for a more extended period.

Other costs such as brokerage commissions are becoming less prominent since most brokers have gotten rid of them to encourage more investments through their platforms. Most brokerage firms may charge zero commission rates, but this may not be the case for all of them. It’s prudent to check to ensure you are well informed about all the costs of investing in a particular fund.

5. How to buy, minimum investments & redemption limits

The way you buy fund shares differs between ETFs and mutual funds. While you can make an order to purchase mutual fund shares at any time within the day, your order will not be filled until the end of the core trading session when the fund manager tallies up and determines the fund’s net asset value. You may end up paying more or less for your investment than initially intended.

ETF shares, on the other hand, provide you access to more options. Given that they are listed on public trading platforms like stocks, you can buy and sell them at any time. Additionally, you have more control over the price you buy or sell your shares through the market and limit orders.

Minimum investment limits are another consideration when it comes to investing in either fund. Typically, most fund managers have a minimum investment limit for mutual funds. For instance, Vanguard, a popular US-based investment company, has a $3,000 minimum investment limit for its mutual funds. Other firms could have a higher or lower limit, but most have these limits in place.

Conversely, ETFs typically have a lower entry barrier allowing investors to purchase as little as one share retailing for as low as $10. ETFs also do not have early redemption fees as mutual funds do. Typically, investment companies charge redemption fees whenever an investor chooses to liquidate their shares before a certain period, usually between 30 and 90 days.

6. Fund returns

When it comes to investment returns, it can be challenging to decide which investment is better than the next, and this is coupled with the fact that there are no guarantees in the business. A good investment today might not be in the future. Past performance does not necessarily represent future outcomes, but past performance can indicate what to expect in the future.

Looking at prior performance metrics, mutual funds, which are often more actively managed, tend to perform less impressively over long periods than ETFs, which are more passively managed. On the other hand, the situation is reversed when it comes to shorter periods.

Actively managed funds are often optimized for current market conditions, which constantly change. A good fund management team should ideally outperform a benchmark metric such as an index, but statistically, over extended periods, this has not been the case.

Outside the fund management arena, investors and traders have more direct control of their returns when investing in ETFs than with mutual funds. Traders can go long or short sell ETF shares taking advantage of both market rallies and drawdowns. They can also take advantage of market/limit orders to reduce their order fees. With these points in mind, it’s easy to see why ETFs are becoming more popular; they provide more opportunities to earn greater returns from the market than mutual funds.

Advantages of ETFs over Mutual Funds

From our arguments in the previous section, you can conclude that both ETFs and Mutual funds have their advantages and drawbacks as investment vehicles. This section highlights these advantages more concisely for easier comparison, and we’ll start with the benefits of ETFs:

- Ease of entry – unlike mutual funds with minimum investment limits, ETFs allow users to invest as little as a single share and sometimes even fractions of shares, making it more convenient and accessible to any investor;

- Ease of trading – ETFs can easily be bought and sold on stock exchanges, just like stocks. ETF investors have access to tools mutual fund investors do not, such as limit orders, real-time order execution, and short selling through margin accounts. Additionally, ETFs have no redemption fees;

- Cost – it’s not entirely accurate to generalize by saying that all ETFs are cheaper than all mutual funds, but typically most ETFs tend to be cheaper than comparable mutual funds. The cost factor is mainly determined by the level of involvement by the fund managers. The more active they are, the higher the expense ratio. Since most ETFs are passively managed, they are cheaper to hold in your portfolio. Additionally, ETFs provide low-cost exposure to a broader range of assets than investing in each asset in isolation;

- Tax efficiency – when investors buy and sell a financial asset, they incur a capital gains tax liability. The structure of an ETF means that an investor who chooses to buy and hold their ETF shares can pay less tax than one who opts to trade more frequently. When it comes to mutual funds, most of which are actively managed, tend to attract higher tax costs, and the capital gains liability is shared amongst all shareholders;

- Niche exposure – there are more ETFs than there are mutual funds that track niche-specific markets. Coupled with the low cost of investing in ETFs, they can be great investment vehicles to more exotic markets.

Advantages of Mutual funds over ETFs

Mutual funds have been around much longer than ETFs and have attracted significantly more investments. But even with the launch of ETFs, mutual funds continue to be a favorite among long-term investors, and for a good reason. Mutual funds have some advantages over their more recent counterparts. Some of these advantages are:

- Better pricing mechanism – the value of mutual funds is regularly recalculated at the close of markets, giving the fund managers more control over the share prices. Unlike ETFs traded on the open markets and prone to market forces of demand and supply, mutual funds are more stable and reliable. Investors are assured that they will purchase shares at net asset value all the time;

- Market performance – most mutual funds are actively managed, and this means that a team of analysts and researchers are always on the lookout for a profitable opportunity. Statistically, actively managed funds perform better than passive funds in the short term and depending on an investor’s goals, this could be a more appealing choice;

- Risk mitigation – investors face many risks, chief among them being a lack of liquidity in their favorite markets. ETFs shares, whose prices depend on market forces, tend to deviate from their NAV, especially for thinly traded markets forcing investors to buy at a premium or sell at a discount. The pricing mechanism of mutual funds is more stable and arguably better suited for the thinly traded markets;

- Cost – for a long time, mutual funds have been believed to have higher expense ratios than ETFs, which has been largely accurate. But there is a growing shift in the market, with some investment companies creating passively managed mutual funds and actively managed ETFs. In this case, the mutual funds would be cheaper to hold in a portfolio.

ETFs Vs. Mutual funds: which one is right for you?

The choice between a mutual fund and an exchange-traded fund that is best for you is determined by your investment profile, your goals, and your risk tolerance. There are several factors to consider, and they are mostly subjective, which means that a great fund to invest in for you might not be suitable for the next investor. They include:

- Risk tolerance – an investor looking for higher returns will have to accept higher market risks. Taking calculated higher risks means investing in exotic assets, thinly traded funds, otherwise inefficient markets, etc. Taking more considerable risks is a better strategy for someone looking to grow their wealth but not so much for someone trying to preserve it;

- Cost-conscious – as we have mentioned before, there are several funds in the market, and each is uniquely presented by their investment companies. They vary in various ways, including costs such as expense ratios, commissions, redemption fees, etc. Tax liabilities are also a factor to consider when calculating how much a fund would cost you in any particular period of investment;

- Niche exposure – the market you may consider participating in may not have a fund in which to invest. For instance, cryptocurrency investors in the United States cannot invest in a Bitcoin ETF or mutual fund as none is available in the domestic market;

- Control over investment – different funds give investors varying degrees of control over their investments. ETFs, for example, can be traded on the stock exchange just like stocks allowing investors to buy, sell or even short sell the fund. Additionally, ETF investors can use various market tools such as limit orders to reduce their costs. Mutual funds don’t provide as much control as you get with ETFs;

- Asset flexibility – mutual funds tend to be highly inflexible assets limiting investors to purchase them directly from investment companies. Shareholders are not free to trade these shares with another fund manager or even trade them with other investors with different brokers. To invest in a similar mutual fund offered by another broker and fund manager, you have to redeem your shares first or hold two funds simultaneously;

- Minimum investment – mutual funds, as opposed to ETFs, often have minimum investment requirements, and this can limit an investor with little capital from investing in them. With ETFs, you can even get in with as little as a single share which could be worth as low as $10. It’s, therefore, easier to invest in an ETF than it is with a mutual fund.

ETFs vs Mutual Funds: Final thoughts

ETFs and mutual funds provide an excellent diversification tool for investors but, as we have highlighted in this guide, choosing which one is right for you may not be as easy as it looks. There are several factors to consider, and no one asset is necessarily better than the other. Your particular circumstances will dictate which works best and which one to avoid.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

Frequently Asked Questions on ETFs vs Mutual Funds

What is an ETF?

The term ETF stands for ‘exchange-traded fund.’ It is a basket of assets such as stocks, bonds, or commodities whose shares are listed on public exchanges for investors to buy, sell and exchange just as they would publicly listed company shares. The price of ETF shares is determined through the interaction of market forces of demand and supply.

What is a mutual fund?

A mutual fund is a pool of investor resources used to purchase a basket of assets such as stocks, bonds, or commodities. Unlike ETFs, shares of mutual funds are not listed on exchanges but are instead sold by the investment company directly to the investors. Redemption is also done through the fund manager and not traded on exchange platforms.

Why choose an ETF over a mutual fund?

The comparison between ETFs vs. mutual funds is not a clear-cut answer where you can say that ‘all’ ETFs are better than ‘all’ mutual funds. However, some situations may favor ETFs over mutual funds. For instance, a situation where the ETF under consideration is cheaper to hold in your portfolio, more tax-efficient, or it offers you exposure to the kind of assets you are targeting, assuming you can’t find a comparable mutual fund. Generally, ETFs are cheaper in terms of expense ratios, tax efficiency, and they are easier to invest in since they offer lower entry investment minimums.

What is the downside of ETFs?

Every asset class has a downside, and ETFs are no exception. Their drawbacks include a tendency towards offering lower returns in the short term since most are passively managed. ETFs also employ the market-forces pricing mechanism that is at a disadvantage when it comes to inefficient and thinly-traded markets.