Mathematical or Quantitative finance is a field of applied mathematics concerned with the modeling of financial markets. It overlaps heavily with other closely related fields such as computational finance and financial engineering. Quantitative finance makes extensive use of stochastic calculus (mathematics which deals with random processes) and mostly requires mathematical consistency – not necessarily compatible with any particular economic theory. It’s applications are mostly in the areas of derivatives pricing and risk and portfolio management.

The two foundational components of quantitative finance as a discipline are:

- the theorem of arbitrage-free pricing (meaning that when building/applying mathematical models, for the sake of convenience, an ideally efficient arbitrage-free, and complete market is assumed);

- and the perhaps the most famous in all of the finance – Black-Scholes formula which has become the industry standard for pricing options.

Quantitative finance really emerged as a discipline in the 1970s following the work of Fischer Black, Myron Scholes, and Robert Merton on options pricing theory for which they were awarded the Nobel Prize in Economics.

The Black-Scholes model was first published in the Journal of Political Economy by Black and Scholes and was later expanded upon by Robert Merton in 1973 going to become the first mathematical framework for approaching options pricing with some precision (as prior to that there were no agreed-upon ways to how one would make these estimates realistically).

To give one an idea, the global financial derivatives market has grown from little over a trillion U.S. dollars in the 1970s to more than 1,2 quadrillion U.S. dollars today. This is a good measure of how we’ve gone from the era of industrial capital to that of financial capital over the past few decades.

The Black-Scholes model captures an important market heuristic and a basic intuition in how financial markets are reasoned about in practice. Depending on the needs and circumstances of the context, the model can be adapted, expanded upon and modified depending on what it needs to accommodate and account for.

However, despite the existence of other, more complex models the Black-Scholes remains the gold standard in options pricing and the epitome of modern finance since its inception and to this day.

In this article, we’ll explain what options are, how the Black-Scholes model applies to pricing options and its fundamental significance to contemporary modern finance.

Options pricing and financial derivatives

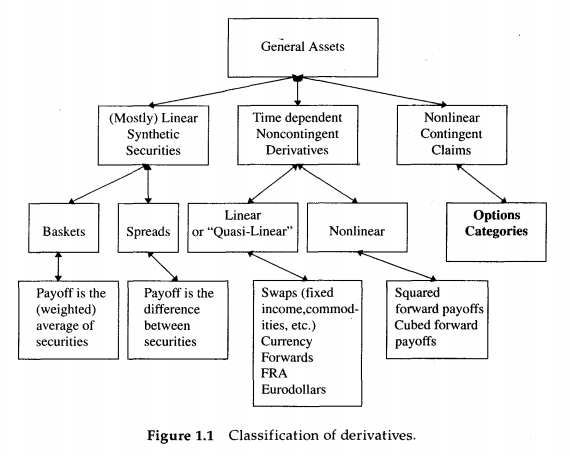

Options are a category of financial derivatives. Financial derivatives are instruments or assets that constitute an abstract form of capital whose value derives from and is contingent upon some underlying asset (usually just called the underlying or sometimes spot or cash price). That could be foreign currencies, stocks, commodities, equity, etc.

Options have expiry dates and can be either put options or call options. A put option gives the owner the right (but not the obligation, hence the optionality) to sell an asset at a specified price (as determined by the option) by a certain date to a given party.

Puts & Calls

Purchasing put options (“put” as in “put up for sale”) on a stock or an asset usually indicates negative sentiment about their future value. A call option, on the other hand, is a contractual agreement between a buying and a selling party where the buyer of the call option has the right to buy an agreed-upon quantity of the underlying asset from the seller of that option at a specified price in at a certain time.

Puts and calls can sometimes be confused. For a currency pair, for example, a put-on USD/EUR (right to sell USD and buy EUR) is a call on USD/EUR. Similarly, a put-on yield is a call on bonds. Also, there’s a difference between American and European options.

A European option can only be exercised on the last day (and is therefore mathematically simpler) while an American option can be exercised any time between its issuance and its expiry date. A hybrid, the Bermudan option can be exercised on a set number of days between inception and expiration.

The strike price

The strike price, also known as the exercise price, is the fixed price at which the owner of an option can buy or sell the underlying asset or security. The strike price may be set in reference to the spot (market) price of the underlying or it may be fixed at a discount or a premium.

“In the money” (ITM) is a term used in regards to options that refers to an option that has intrinsic value, that is its strike price is favorable relative to the current market price of its underlying asset.

To test whether an instrument is an option look if the payoff involved is asymmetric and if there is a strike price. For example, a call option is priced at expiration as:

Max(S – K, 0)

Where S is the price of the underlying at expiration and K the strike price, so the above reads as the greater of the two possible options – the difference between price of underlying and the strike or zero, since one can choose not to use the option and if the S – K difference ends up negative then the owner of the option would naturally prefer to receive nothing). A put option is then expressed as:

Max(K – S, 0)

Options are non-linear derivatives more specifically due to their price being time-dependent and contingent upon whether or not specific events occur. In other words, they’re contingent claims which distinguish themselves from other financial products in being a potential asset for one party and potential liability for another.

This property of options subjects them to probability theory and the practice of option pricing is one dealing with probability. Non-linear derivatives afford a specific kind of exposure and opportunity to profit from market volatility and instability.

However, it may also require dynamic hedging and as with most sophisticated financial instruments, options, while simple to understand how they work in principle have to be engaged with to understand how they actually trade in practice.

A philosophical approach to Options trades

The earliest option trade recorded in Western literature, interestingly enough, was a bet on the future crop by Thales of Miletus (recounted by Aristotle in his Politics). Thales, like Greeks, mostly just wanted to make a point that philosophers who so desire can actually achieve material success and live wealthy.

So, in order to profit from better than expected olive crop, Thales went on to put a deposit on every olive press in his vicinity and then later as demand for these presses grew he went on to lend them for a good profit – in other words, he went on to buy a call on olive presses in view of anticipating certain future events taking place.

Such a model is based on two fundamental assumptions which constitute the philosophical essence of the model:

- on one hand, taking the market price movement of assets to be a random walk [continuous process] following geometric Brownian motion with the property of being memoryless;

- on the other hand assuming a frictionless market (that is, complete markets, without any transaction costs or taxes involved, no adjustments, assuming perfect information, etc.).

The Black-Scholes model

The Black-Scholes model essentially captures the risk-neutral replication of securities in a market which is said to be complete (i.e., there’s a price for every asset in every possible state of the world). So, every trader, market maker, and risk/portfolio manager usually needs to spend some time working around some of the assumptions implied in the Black-Scholes model to make it stand.

Elie Ayache even claims that the derivatives market follows its own logic quite different from the theory and that the formalism of theory is only initially necessary while the sense and phenomenology of the market are acquired in the process of being immersed in its dynamics which paradoxically inverse the logic of the theory.

The Fundamentals

Seasoned and experienced traders have learned the necessary heuristics and tricks needed to make the Black-Scholes model work and overall tend to be weary of trading it for any other pricing tool or whatever other more advanced or complex a pricing model.

One important reason for that is because Black-Scholes gives one a sense of a unified measure of the price of an option on the basis of a small number of parameters that need be estimated. Nonetheless, traders can still build on the foundation of the Black-Scholes and introduce additional parameters as needed or when dealing with more exotic options.

The Formula

Now, the Black-Scholes model or formula is used to calculate the theoretical value of options and their price variation overtime on the basis of what we know at the given moment – current price of the underlying, exercise or strike price of option, expected risk-free interest rate, time to expiration of the option and expected implied volatility of the underlying (as the standard deviation of the logarithm of returns – more on that later).

In options by volatility, it is always meant implied volatility and not historical volatility. And naturally, options are more valuable the higher the volatility of their underlying security (i.e., the more it deviates in either direction from the exercise price of the option). So, the basic formula is expressed as:

C – denotes a call option,

S – the current stock price of the underlying,

t – the time until the option expires,

K – the strike price,

r – is the risk-free interest rate,

e – the exponential term

N – represents a cumulative distribution function for a standard normal distribution (which can be any other type of probability distribution instead and the stock price as weighted by that probability).

d1 and d2 – denote the formulas which compute the implied volatility.

The implied volatility

Implied volatility is one of the most important variables which determine the value of an option and it differs from historical volatility (which is calculated from known past returns) in that it is a forward-looking subjective measure.

There are various approaches to measuring implied volatility. One is entering the market price of the option into the Black-Scholes formula and back-solving the value of the volatility.

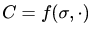

Other methods may utilize iterative searches, trial, and error, etc. Generally, the value of an option depends mainly on an estimate of the underlying security’s future realized price volatility (usually denoted with the Greek sigma, σ). Expressed mathematically:

C – the theoretical value of a call option,

f – the pricing model employed such that it depends on σ in addition to whatever other variables and inputs.

So, basically Black-Scholes for a call computes the calculus of the movement of the strike price at any point in the time interval of the option’s life cycle as deduced from the value of the market price of the underlying at the same point of its price trajectory which gives us the theoretical price of the option.

For a put option, the order is reversed and the price of the underlying is subtracted from that of the option’s exercise price.

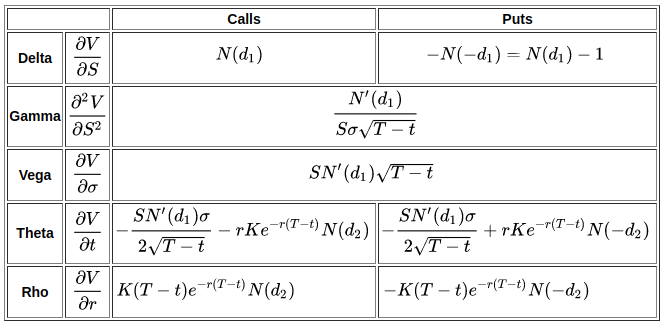

The Greeks [dimensions of risks]: delta, vega, theta, gamma, and rho

You will also often hear options traders refer to “the Greeks”- the term refers to the different dimensions of risks involved in taking an options position and the primary ones are delta, vega, theta, gamma, and rho – each calculated as a first partial derivative (as in a derivative function) of the options pricing model used (i.e., Black-Scholes).

The Greeks provide a way to measure the sensitivity of an option’s price with respect to a number of quantifiable factors (as arguments of its function) – they’re also called risk measures or hedge parameters. To explain each very briefly:

- Delta (Δ) represents the rate of change or price sensitivity of the option relative to the underlying. The delta of a call option has a range between zero and one, while that of a put option between zero and negative/minus one.

- Theta (Θ) measures time sensitivity and represents the rate of change between the option price and time. Also known as an option’s time decay, it indicates how much an option’s price decreases as its expiration point comes closer.

- Gamma (Γ) represents the rate of change between an option’s delta and the underlying’s price – a second-order (secondary derivative function) price sensitivity. It indicates how much the delta would change given a price move in the underlying.

- Vega (v) represents the rate of change between an option’s value and the underlying asset’s implied volatility, measuring the option’s sensitivity to volatility.

- Rho (p) represents the rate of change between an option’s value and a 1% change in the interest rate, i.e. sensitivity to the interest rate.

As partial derivatives of the price with respect to other parameter values, “the Greeks” are as important in quantitative finance theory as they are in practice when actively trading financial instruments.

Financial institutions typically calibrate threshold values (risk limits) for each of the Greeks that their traders must not exceed – Delta usually being the most important one as it tends to confer the largest risk.

Black-Scholes in practice

One can easily pull a Black-Scholes calculator, put an option’s parameters and compute its theoretical price at that time and given those values. But like most things, while in theory there may not be much of a difference between theory and practice, in practice and when dealing with dynamic reality where things aren’t as neat and clear-cut as the idealized model might lead us to believe at first. Above all, it must be understood that models are approximation heuristics rather than recipes for getting repeatable and precise results.

In the Black-Scholes model it is especially important to first consider the particulars of the option one is dealing with and thus the kinds of probability distributions most accurately applicable to describing the behavior of the option. And perhaps even more importantly, the implied volatility of an option is often considered a more useful measure of that option’s relative value than its price as such.

In general, supply and demand and time value are the main determining factors in estimating implied volatility – which overall tends to increase in bearish markets and decrease when markets are bullish. It quantifies uncertainty solely on the basis of prices, fundamentals do not come into play. It predicts movement, but not direction and tends to be sensitive to unexpected factors.

Indices and instruments such as the VIX (CBOE Volatility Index), the VXN Index and IVX (Implied Volatility Index) track the value of the implied volatility of various derivative securities (for example, the VIX is the from a weighted average of implied volatilities of various options on the S&P 500 Index).

In conclusion

In conclusion, getting a good sense of implied volatility is key to making the Black-Scholes model work for you. There’s many tools online (e.g., CBOE’s implied volatility calculator available here) and software available for options trading which automatically compute your variables and indicators in real time.

We’ll explore the concepts of implied volatility and statistical probability distributions in more depth and further detail in future articles.