Over the past week and a half, Campbell’s (NASDAQ: CPB) has been at the center of one of the most controversial lawsuits in the market this year.

The case involves the company’s former vice president and chief information security officer, Martin Bally, who allegedly mocked low-income consumers, belittled the company’s own products as “3-D printed meat,” and made racist remarks about colleagues.

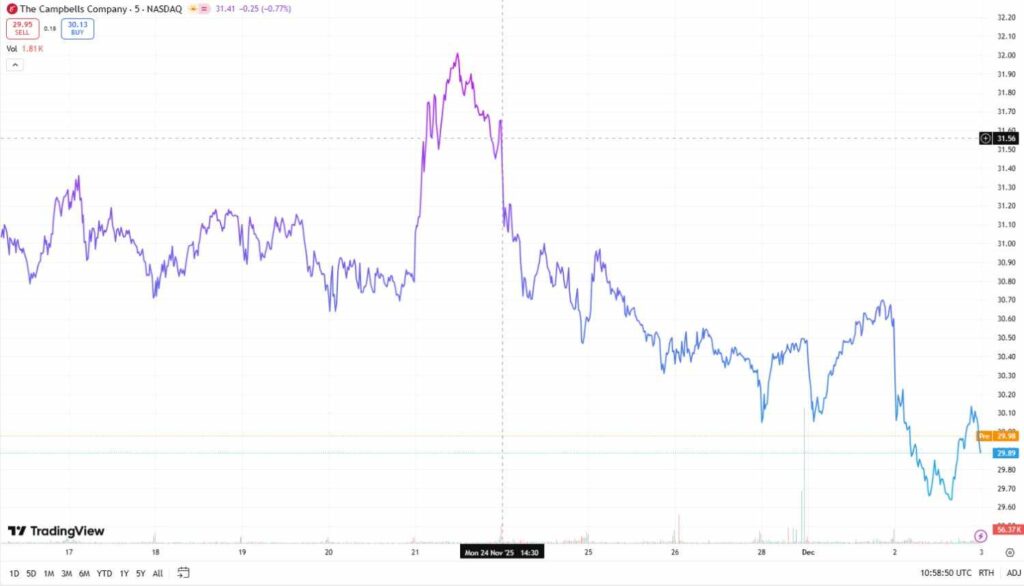

In light of the accusations captured in an audio recording created by former cybersecurity analyst Robert Garza, the food processor’s shares dropped more than 3 on November 24, and by November 26, they had sunk to lows approaching those seen during the Global Financial Crisis.

At the time of writing, December 3, Campbell’s stock was trading at $29.89, the price having dropped around 5.3% in total from around $31.56 on November 24, when the news of the scandal broke.

Analysts cautious ahead of Campbell’s first-quarter earnings report

Campbell’s is scheduled to release its fiscal first-quarter earnings report on December 9, and some predictions are understandably mixed. For instance, Evercore ISI reaffirmed its “In Line” rating and $36 price target for Campbell Soup on December 1, but it still expects declines in both sales and profit.

Overall, Campbell’s is projected to report quarterly earnings of $0.74 per share (EPS), a 16.9% drop from a year ago, according to the Zacks Consensus Estimate. Similarly, revenue is expected to hit $2.66 billion, down 3.9% from the same period last year. While a negative ESP doesn’t necessarily signal a miss, it does lower the overall investor confidence.

However, the long-term outlook for the stock does not appear bearish. The majority of the analysts rate it a “Hold” and project the average CPB stock price target for the next 12 months at $33.21, which suggests an 8.56% upside from the current levels, as per TipRanks.

All in all, the soup maker likely won’t see a strong earnings beat this quarter, but its long-term prospects could be different.

Featured image via Shutterstock