Chamath Palihapitiya, once the face of the SPAC boom, is now at the center of controversy as investors face massive losses from the companies he took public.

Known as the ‘SPAC King,’ the former Facebook executive leveraged the hype around special-purpose acquisition companies (SPACs)—shell entities that provide companies with a backdoor entry to public markets as an alternative to traditional IPOs.

SPACs have a primary backer, sometimes called a sponsor, who raises money from investors and uses the funds to acquire a private company. While this model has been around for some time, it gained immense popularity during the pandemic.

Palihapitiya capitalized on this momentum, selling retail investors on the idea that these blank-check firms offered them the chance to get in early on high-growth companies. He launched a series of SPACs under his Social Capital brand, all carrying ticker symbols beginning with ‘IPO’—from IPOA to IPOF.

These vehicles attracted massive investor interest, largely due to his aggressive media appearances and social media promotions. But as the market turned, many of his once-hyped deals collapsed by more than 90%, leaving everyday investors with heavy losses.

Receive Signals on SEC-verified Insider Stock Trades

This signal is triggered upon the reporting of the trade to the Securities and Exchange Commission (SEC).

Investor Adam Rossi has now exposed the full extent of Palihapitiya’s SPAC dealings, highlighting the massive financial damage incurred by everyday investors.

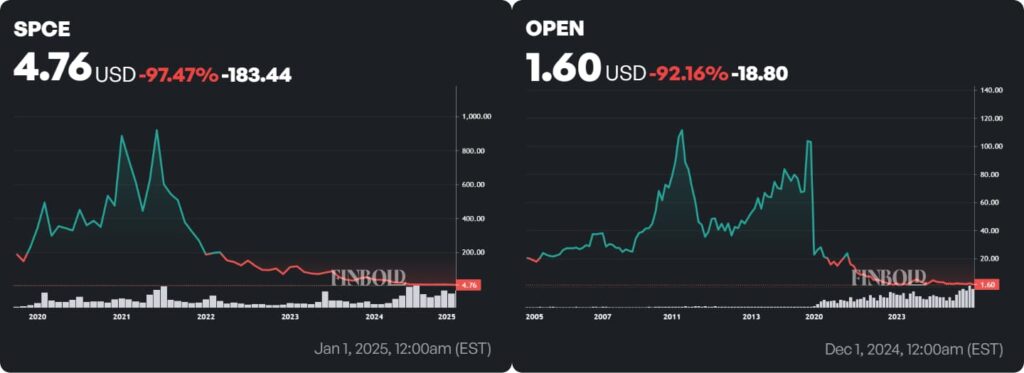

Virgin Galactic (NYSE: SPCE)

Originally IPOA, Virgin Galactic (NYSE: SPCE) was one of Palihapitiya’s most well-known deals, which he took public via SPAC in 2019, touting it as the future of space tourism.

The excitement around commercial space travel sent the stock soaring above $60 in 2021, with Wall Street analysts drawing comparisons to Tesla (NASDAQ: TSLA).

Retail investors piled in, but as the hype peaked, Palihapitiya dumped all of his personal shares for $213 million, cashing out right before the stock crashed. At press time, SPCE is trading at $4.12.

Opendoor (NASDAQ: OPEN)

Palihapitiya merged his SPAC IPOB with Opendoor (NASDAQ: OPEN), hyping it as the ‘Amazon of real estate’. The stock surged to $34 in early 2021, fueled by aggressive marketing and the broader SPAC frenzy.

However, by 2022, Opendoor posted a staggering $1.4 billion loss in a single quarter and was forced to lay off 18% of its workforce. At press time, Opendoor is trading at $1.39, down over 95% from its all-time high.

Clover Health (NASDAQ: CLOV)

In 2021, Palihapitiya merged his IPOC SPAC with Clover Health (NASDAQ: CLOV), touting it as the future of Medicare insurance.

However, just days after going public, Hindenburg Research exposed Clover Health for hiding an active DOJ investigation. The stock initially surged to $28, but as the scandal unfolded, it crashed to just $0.80. At press time, the stock trades at $4.18, still a fraction of its early hype.

SoFi (NASDAQ: SOFI)

SoFi Technologies (NASDAQ: SOFI) went public through a merger with IPOE, with Palihapitiya promoting it as a ‘fintech revolution’.

Investors initially bought into the hype, sending the stock to $25. However, before insiders’ lock-up restrictions expired, Palihapitiya cashed out $200 million, securing his profits while retail investors remained exposed.

SoFi’s stock has since fallen to $14 at the press time, with concerns about profitability and stock dilution weighing on its performance. While one of the better-performing SPACs, investors who bought in at peak valuations remain deep in the red.

Why these deals were ‘Predatory’

While many SPACs have struggled, investor Adam Rossi highlights that the structural flaws of these investment vehicles overwhelmingly benefit sponsors at the expense of retail investors.

This thread has almost 3M views 🤯

— Adam Rossi (@rossiadam) February 23, 2025

Here is a video clarifying what I think was predatory about the @chamath SPACs

It is my belief that public figures with a huge audience have a moral obligation to give ample disclosures when they are pitching investments

Also expand on $SOFI pic.twitter.com/M7sYv3EoUz

Their priority, as Rossi notes, is not necessarily to bring strong companies to market but rather to complete a merger and cash out. When these financial incentives are not properly disclosed, retail investors are left exposed to high-risk deals with little transparency.

One of Rossi’s biggest concerns is Palihapitiya’s use of PIPEs (Private Investment in Public Equity). Unlike traditional IPO investors, PIPE participants are not subject to lock-up restrictions, allowing them to sell early while retail investors remain trapped.

In the case of SoFi, Palihapitiya dumped hundreds of millions of dollars worth of shares while everyday investors had no option but to hold—a move Rossi compares to a classic rug pull.

While technically legal, Rossi believes that Palihapitiya’s lack of transparency and self-serving actions were unethical. With many SPAC-backed companies now trading far below their peak values, investors continue to debate whether these declines were simply market-driven losses or the result of a system that prioritized early backers over long-term shareholders.

Featured image via Shutterstock