As Nvidia (NASDAQ: NVDA) remains a dominant force in the artificial intelligence sector, investor attention is on the company’s upcoming earnings set for release after the market close on February 25.

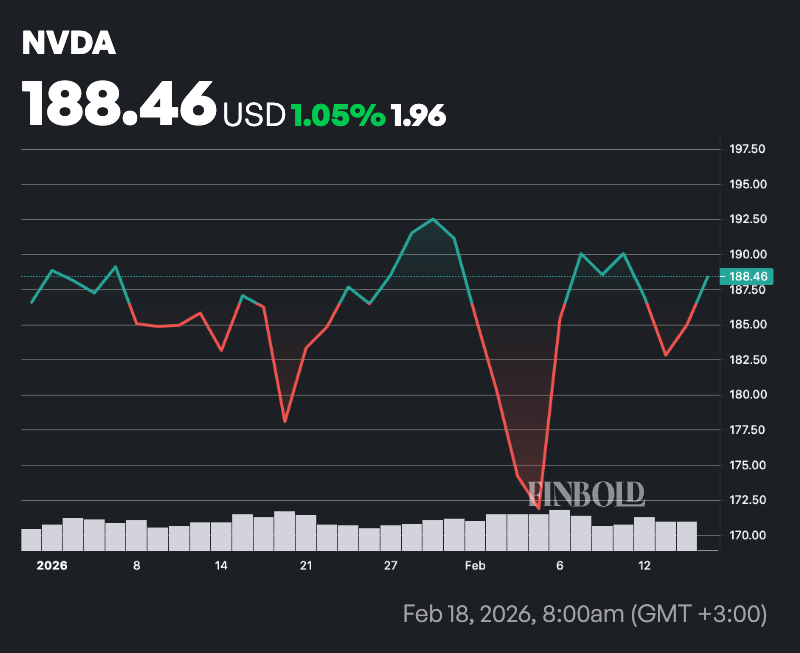

By press time, NVDA shares were valued at $188, up just 1% on a year-to-date basis.

Analysts anticipate strong results for the quarter ending January 25, 2026, with consensus estimates calling for adjusted earnings of approximately $1.52 per share and revenue around $65.6 billion.

These figures would represent a year-over-year growth of roughly 71%, continuing Nvidia’s pattern of outperforming expectations in recent periods. The prior quarter delivered adjusted earnings of $1.30 per share and revenue of $57 billion, surpassing forecasts.

A key focus for the upcoming report will be progress on the Blackwell architecture, which CEO Jensen Huang has characterized as experiencing exceptional demand.

Production ramps and supply fulfillment for hyperscalers and enterprise clients are expected to drive significant contributions.

Recent announcements, including major multi-year GPU supply agreements with partners like Meta (NASDAQ: META) for Blackwell and the forthcoming Rubin platforms, highlight sustained momentum in AI infrastructure investments across global markets.

Wall Street bullish on NVDA stock

Meanwhile, Wall Street analysts remain overwhelmingly bullish on Nvidia with the chipmaker earning a ‘Strong Buy’ consensus based on 39 recent ratings over at TipRanks.

According to the latest 12-month forecast data, 37 analysts rate the stock a ‘Buy’, one recommends ‘Hold’, and one suggests ‘Sell’. The average price target stands at $260.38, implying a potential upside of 40.77%.

The highest price target among analysts is $352, while the lowest estimate is $200, indicating a wide but generally optimistic outlook.

The projected upside points to confidence in Nvidia’s growth, driven by demand for artificial intelligence chips and data center solutions. If results meet or exceed expectations, bullish targets could fuel further stock momentum.

However, the wide gap between high and low forecasts signals potential volatility tied to earnings performance and broader market conditions.

Meanwhile, elevated expectations mean that even strong results may not prevent swings if forward guidance disappoints, particularly regarding competition from custom chips, a possible slowdown in AI spending, or supply-chain constraints.

Some views suggest the stock could face pressure after February 25 if the report fails to surpass the high bar set by prior beats.

Featured image via Shutterstock