For all of its undeniable successes, Nvidia (NASDAQ: NVDA) has been suspected of being significantly overvalued in the stock market. Indeed, though the semiconductor giant recorded a substantial revenue increase in recent years, to many, the accompanying $3 trillion valuation surge in about two years appeared oversized.

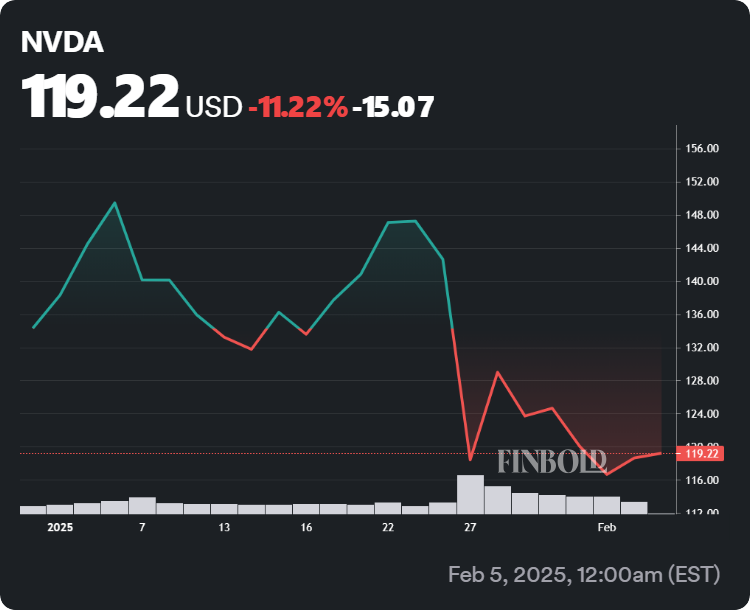

At no point was this uncertainty more evident than in the wake of the release of the novel Chinese DeepSeek artificial intelligence (AI) model, which saw NVDA stock plunge 19.02% from $147.22 to $119.22 between January 23 and February 5.

A major reason for the drop was the reported efficiency of the AI, especially compared with the more mainstream U.S. models, and analysts and investors have become uncertain if the chipmaking powerhouse can sustain its rapid growth.

Did DeepSeek invalidate the 2025 NVDA stock bull case?

Following last week’s events, Morgan Stanley (NYSE: MS) revised its forecast for Nvidia’s shipments of the large language model (LLM) inference-focused GB200 NVL72 from between 30,000 and 35,000 to between 20,000 and 25,000 with a related pessimistic scenario even seeing a drop below 20,000 possible.

Should the banking giant prove correct in its reassessment, it would mean Nvidia’s revenue for 2025 would be severely impacted as the reduction in sales of the advanced component would amount to at least 16.67% and might, at worst, go beyond 42.86%.

The headwinds generated by the major industry shift caused by DeepSeek were only compounded by President Trump’s preference for tariffs. Specifically, the new U.S. administration already implemented a 10% tariff on China and is expected to levy more dues on Taiwan later in February.

Though the tariffs on Taiwanese companies might be postponed – only days elapsed between Trump’s ordering a 25% tariff on Canada and Mexico and his postponing their implementation – the prospect nonetheless raises significant concerns for investors.

Taiwan is a global semiconductor manufacturing hub as it boasts multiple foundries with the biggest – Taiwan Semiconductor Manufacturing Company (NYSE: TSM) – being responsible for more than 50% of total production.

With Nvidia being a customer of TSMC, it is in danger of experiencing simultaneous supply and demand shocks arising, on the one hand, from the alleged efficiency of DeepSeek and, on the other, from the higher prices of Taiwanese goods.

Why Nvidia stock might still reach new highs in 2025

Despite the turmoil, disaster is not guaranteed. The fact that both a supply and demand reduction could occur simultaneously could provide Nvidia with breathing room to reorganize and focus toward, for example, TSMC’s foundry located in the U.S.

Simultaneously, a true demand shock may never materialize. As Meta Platforms’ (NASDAQ: META) Yann LeCun pointed out, investors may have severely misinterpreted the implications of DeepSeek.

Indeed, higher efficiency isn’t guaranteed to invalidate the massive Western infrastructure investments, but could instead help speed up the progress as, at least in theory, developed infrastructure paired with efficiency breakthroughs should lead to substantially more powerful AI models.

Featured image via Shutterstock