As artificial intelligence (AI) demand soars, Nvidia (NASDAQ: NVDA) and Palantir (NYSE: PLTR) have emerged as top players in the AI-driven stock rally, with shares up 206% and 252%, respectively, in 2024.

Currently, Nvidia’s stock is priced at $147.63, while Palantir trades at $58.39. Both stocks are among the top performers on the S&P 500, reflecting strong investor enthusiasm for AI-focused companies.

However, despite their impressive gains, Nvidia and Palantir have distinctly different business models and valuation profiles, making the choice between them complex for investors looking toward 2025.

To provide clarity, Finbold consulted ChatGPT-4 for insights on which stock is likely to outperform in the year ahead.

Nvidia: The backbone of AI hardware with proven profitability

Nvidia is widely recognized for its dominance in AI hardware, particularly with its graphics processing units (GPUs) that are critical to training and running large-scale AI models.

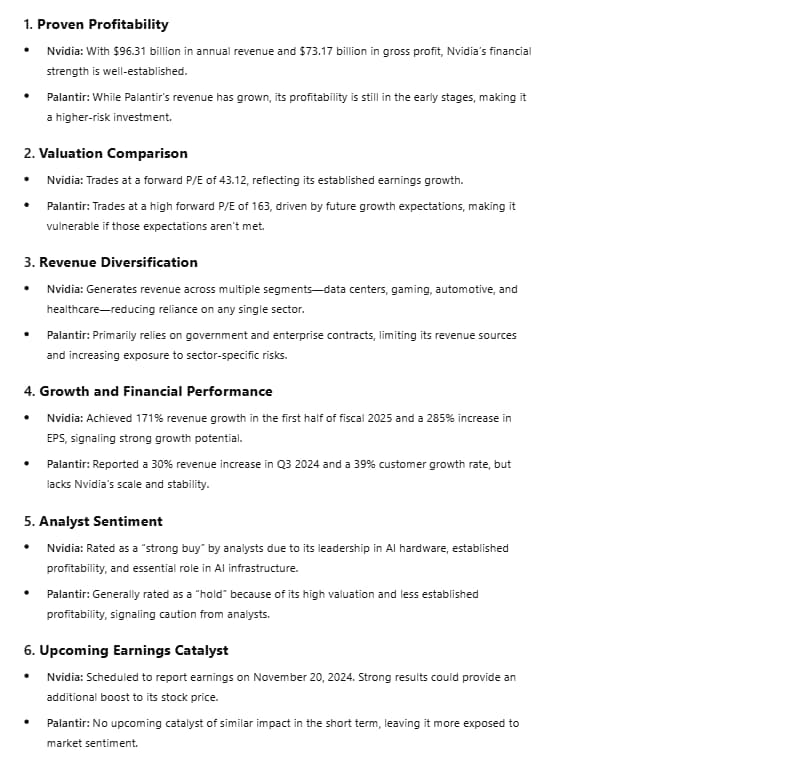

Its Data Center segment, powered by these GPUs, generated $26.3 billion in Q2 2024, marking a 154% year-over-year increase and strengthening its critical role in AI infrastructure.

Nvidia’s growth prospects remain robust, with its Data Center business, the upcoming Blackwell chips, and continued demand for the Hopper architecture driving future potential.

The advanced Blackwell B200 GPUs, initially delayed due to a design flaw, are now set to resume shipments by year-end, following a design fix in collaboration with Taiwan Semiconductor Manufacturing Company (NYSE: TSM), as Reuters reported.

Beyond Blackwell, Nvidia’s H100 chips are critical to powering generative AI platforms like ChatGPT, further solidifying its dominance in the AI landscape.

Nvidia’s stronghold in gaming and automotive adds further stability, diversifying its revenue streams and supporting long-term financial health.

The company’s financials are equally impressive. Nvidia holds a substantial market cap of $3.6 trillion, with a forward price-to-earnings (P/E) ratio of 43.41, reflecting high expectations that align with its proven profitability and growth trajectory.

Analysts anticipate Nvidia’s earnings per share (EPS) to grow by 37.36% over the next five years, thanks to strong demand in its Data Center and AI segments.

Additionally, Nvidia is scheduled to release its earnings report on November 20, 2024, which could further shape investor sentiment and potentially serve as a catalyst for further gains.

Palantir: High-growth AI software leader with valuation challenges

Unlike Nvidia’s hardware focus, Palantir specializes in AI software, particularly data analytics and machine learning solutions for government and commercial clients.

Its flagship Artificial Intelligence Platform (AIP) has seen substantial adoption in 2024, especially among U.S. commercial customers, contributing to a 30% year-over-year revenue increase in Q3.

Palantir’s stock has been on a notable upward trajectory, climbing 252% year-to-date. However, it trades at a steep valuation, with a price-to-sales (P/S) ratio of 49 and a forward P/E of 128, making it highly expensive by industry standards.

Analysts have expressed concern over this high valuation, with most issuing a “hold” recommendation due to Palantir’s reliance on high growth expectations, which makes it more vulnerable to setbacks as its profitability metrics continue to develop.

Despite these valuation concerns, Palantir’s growth in sectors like defense and finance continues to attract investors. In Q3 2024, Palantir posted its highest-ever quarterly profit, with a net income of $144 million and an adjusted operating margin of 38%, up from 29% the prior year.

Additionally, the company closed 104 deals worth over $1 million each, raising its total contract value (TCV) to $1.1 billion, a 33% year-over-year increase.

That being said, Palantir’s future largely hinges on the success of AIP, as the company seeks to position itself as an indispensable AI software provider across industries.

ChatGPT-4o verdict: Nvidia or Palantir for 2025?

While both companies hold strong potential amid rising AI demand, AI models suggest that Nvidia stands out as the safer and potentially more rewarding long-term investment.

Additionally, analysts anticipate that Nvidia’s market cap could keep growing, potentially reaching $4 trillion or more if AI demand remains robust, according to Fortune. Nvidia’s essential role in AI development further solidifies its edge in the AI revolution.

In contrast, Palantir offers compelling growth potential but comes with higher volatility due to its elevated valuation and early-stage profitability.

However, looking toward 2025, Nvidia appears to be the preferable option for risk-averse investors, while Palantir may appeal more to those seeking aggressive, high-growth opportunities.

Featured image via Shutterstock