Nvidia’s (NASDAQ: NVDA) powerful multi-year rally may be entering a decisive bearish phase, according to market analyst TradingShot.

In this outlook, the analyst argued that technical signals now point to the start of a broader correction toward the $100 region. Such a move would imply a drop of about 47% from the stock’s last closing price of $189.

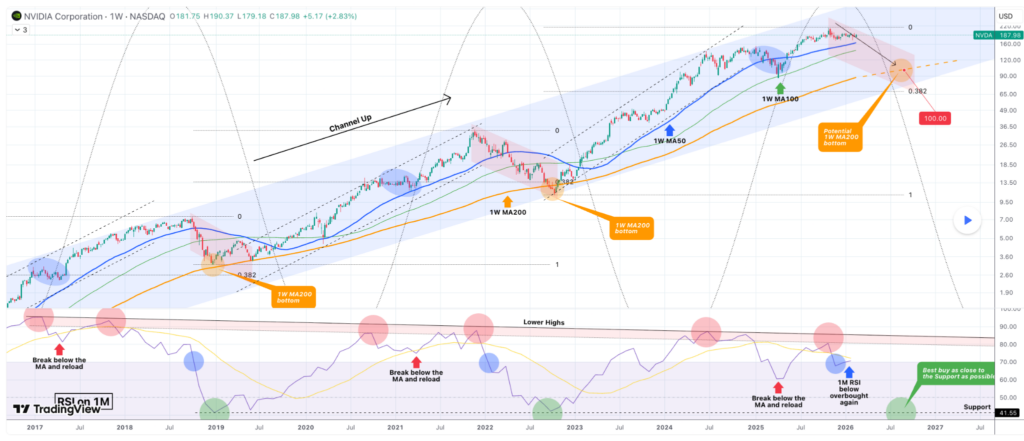

Nvidia stock price outlook

In a February 19 TradingView post, the analyst noted that Nvidia has traded within a well-defined ascending channel for about 12 years, spanning multiple bull and bear cycles.

The price has repeatedly rallied to the upper boundary before correcting toward key moving averages, and the latest rejection near the top in late October 2025 mirrors prior cycle peaks.

The analyst added that Nvidia recently tested a lower-highs zone near the channel’s upper boundary before pulling back sharply. The monthly RSI shows a clear bearish divergence, with momentum failing to confirm new highs, a pattern that has previously marked the end of bullish legs.

The RSI has also rolled over from overbought levels. On the weekly chart, Nvidia has broken below its 50-week moving average, a level that has historically signaled deeper bear phases when lost.

Past corrections within this channel have typically extended to the 200-week moving average, where prior bear cycles bottomed. In October 2022, the stock briefly dipped below the 0.382 Fibonacci retracement before starting a new uptrend.

The 200-week moving average now sits near $100, forming the current downside target. A move to that level would still keep the price above the 0.382 retracement, aligning with historical corrections rather than extreme weakness. Meanwhile, the monthly RSI continues to trend lower. TradingShot noted that a drop into the 43–41 range could signal a developing long-term buying opportunity.

Nvidia fundamentals

This outlook comes as the American semiconductor giant gears up for its next earnings report. Nvidia’s fiscal Q4 2026 results, due February 25, are projected to show revenue of $65.6–$65.9 billion, up 67% year-over-year, driven by surging AI demand.

Analysts forecast adjusted EPS of $1.52, with gross margins around 75%. The consensus price target stands at $255.82, implying 36% upside from $188.

Notably, analysts remain bullish on hyperscaler capex and Blackwell ramps, but high expectations could spark volatility if results fall short.