Shares of the leading fintech company PayPal (NASDAQ: PYPL) are down 60% year-to-date (YTD) despite little change to their underlying business. The core business of the company relates to offering payment solutions to merchants and consumers worldwide.

The current market cap of the company is $89.9 billion, which puts them up with the payment giants such as MasterCard (NYSE: MA) and Visa (NYSE: V), both of which have been in business much longer than PayPal.

Competition seems to be strong in this area; therefore, innovation and adaptation of business models could serve the company well going forward.

Growth trends

PayPal benefited from the Pandemic years leading to strong financial results for 2020 and 2021. Revenues in 2021 amounted to $25.4 billion, an increase of 18.4% year-on-year (YoY).

For Q1 2022, the revenue growth has started off solid; however, the full-year growth expectations are between 11% and 13%, which is slower than in the pandemic years.

During the investor day events, the company outlined its goal of reaching 750 million active accounts by 2025, indicating that the company could grow at a compound annual growth rate of 20%. With Q1 results, these lofty goals might seem out of reach unless new tailwinds appear and propel client acquisition.

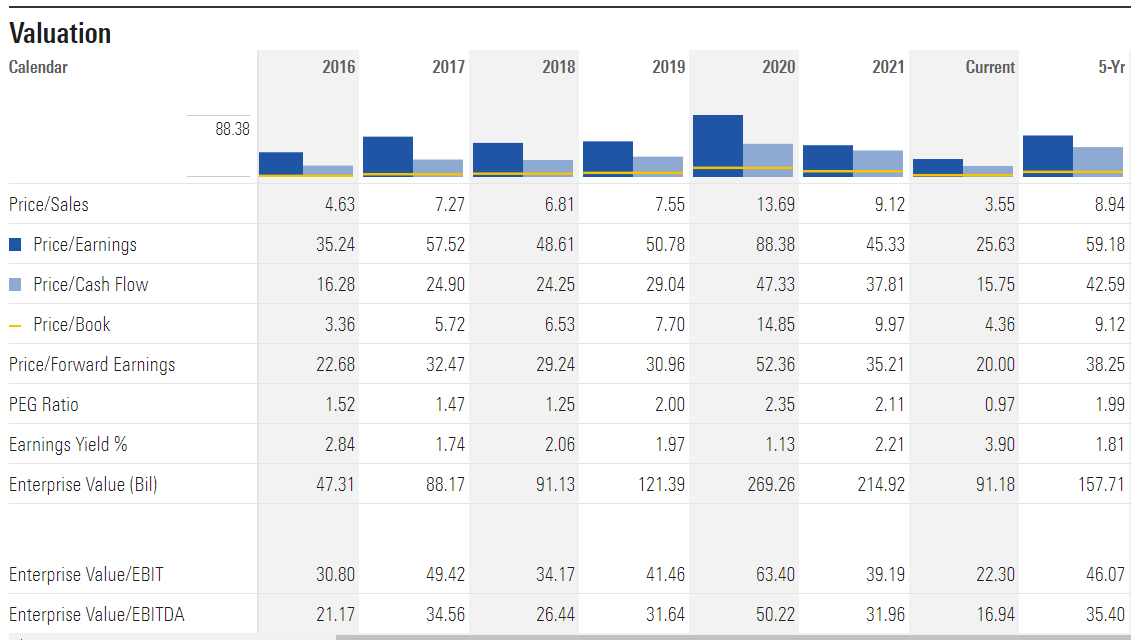

Valuation and conclusion

PayPal was trading at a peak valuation in 2020, where the price to earnings ratio (P/E) was at 88 while the 5-year average ratio is at 59. Currently, the P/E stands at 25, showing that the correction was particularly hard on PYPL.

In Q1 earnings, the company adjusted its estimates for earnings per share (EPS) for the full year to $3.81-$3.93, which is a reduction from its initial estimate of $4.60-$4.75.

With the revised EPS from analysts for 2025, the company’s fair value could lie between $160 and $180. If no further downward revisions for EPS are made, this would imply a potential upside of over 100% from the current trading price of $80.38.

Despite recent headwinds that have brought tech stocks down to their knees, PayPal seems to have a solid grasp of its business and is growing well. There could be more volatility in price, but anything between $60 and $80 for the stock could be a bargain based on the historical valuation of the stock and predictions of future growth.

Personal risk appetites of investors and opportunity costs should factor in when deciding to pull the trigger on PYPL shares.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.