At a time of growing uncertainty, a key recession indicator is offering hints about where the economy might land next.

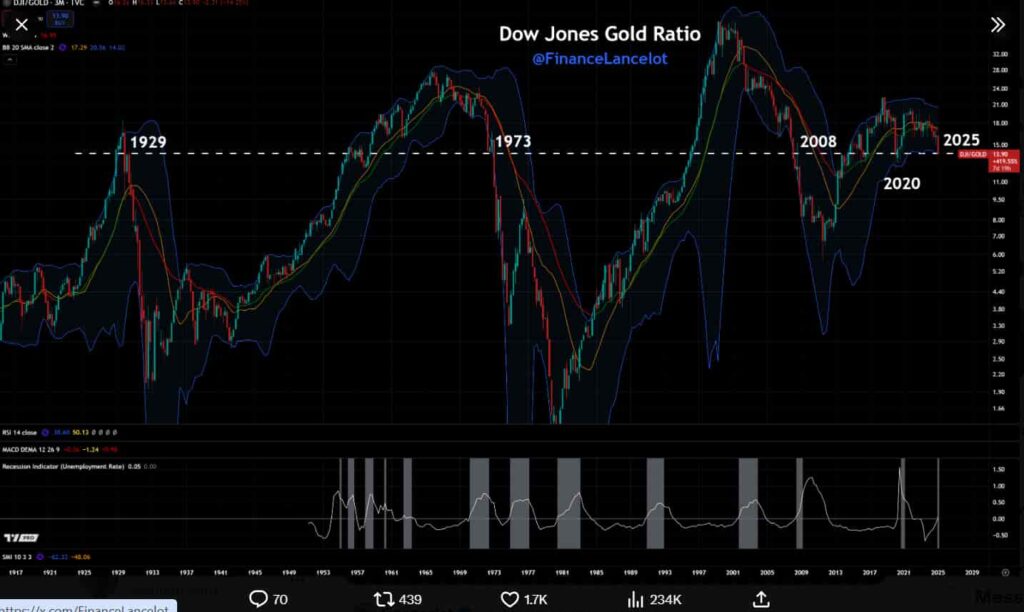

Specifically, the Dow Jones to Gold Ratio, which measures the relative value of equities to gold, is approaching a critical support level that has historically signaled the onset of severe economic downturns, according to an outlook by FinanceLancelot in an X post on March 24.

Dow to Gold ratio as a key recession indicator

The Dow to Gold Ratio represents the amount of gold, measured in ounces, needed to purchase one unit of the Dow Jones Industrial Average (DJIA).

It shows the relative performance of U.S. stocks versus gold, with a high ratio indicating strong stock market performance and a low ratio signaling gold’s outperformance, often viewed as a sign of market weakness or broader economic instability.

Historically, each time the Dow to Gold Ratio declined and crossed below this critical threshold, it has coincided with the onset of significant economic downturns, typically lasting around 18 months. This includes the Great Depression, the 1973 stagflation crisis, the 2008 financial meltdown, and the 2020 COVID-19 crash.

Now, in 2025, the ratio is once again edging toward this historically significant level, heightening concerns that another substantial economic shift may be on the horizon.

Adding to these concerns, bearish momentum reflected in key technical indicators such as the MACD and RSI, combined with rising unemployment-linked recession signals, suggests that current market conditions closely resemble the patterns seen prior to previous downturns.

Wall Street ramps up recession warnings

The Dow to Gold Ratio’s movement is just one of several flashing indicators contributing to growing recession concerns. Wall Street’s recession talk has intensified in recent weeks, fueled by growing economic uncertainty.

Economists at Goldman Sachs (NYSE: GS) have raised their expectations for a U.S. recession over the next year, pointing specifically to policy shifts in Washington as a key source of risk.

In their latest outlook, the team led by Jan Hatzius increased the 12-month recession probability to 20%, up from 15% previously, citing potential tariffs and trade policy uncertainty.

Echoing these fears, Bank of America’s March survey revealed that 55% of fund managers now view a global recession as the top tail risk. Moreover, the survey showed that cash levels jumped to 4.1%, up from 3.5% in February, marking the highest level since 2010 and signaling a classic flight to safety.

Consumer sentiment and economic data fuel the bearish outlook

Consumer confidence has also taken a hit, with the University of Michigan’s Sentiment Index dropping sharply in March amid fears over economic stability, employment, and inflation.

Moreover, leading indicators are signaling clear signs of economic weakness. The Conference Board’s Leading Economic Index (LEI) has posted consecutive declines, falling by 0.3% in February 2025 after a 0.2% drop in January, pointing to slowing industrial production, weakening retail sales, and declining new home sales, suggesting a cooling economy.

Adding to the pressure, a global economic slowdown is also weighing on U.S. exports and trade balances. Sluggish growth in key markets such as China and Europe is further exacerbating risks, potentially undermining GDP growth projections for the remainder of the year.

Featured image via Shutterstock