The downfall of Super Micro Computer (NASDAQ: SMCI) continues to stir market uncertainties. After a series of serious allegations, investors have abandoned ship in droves — but that is not the primary concern on the minds of investors.

As a key player in the semiconductor space, and thus, an important player in the burgeoning AI market, SMCI’s goings-on could stand to have an impact on market favorite Nvidia (NASDAQ: NVDA).

Supermicro is a significant customer for the chipmaker — and seeing as how it could be delisted from the NASDAQ on November 16, just days ahead of Nvidia’s upcoming earnings call, the timing couldn’t be worse

Picks for you

NVDA stock is trading at an all-time high (ATH), and the business, worth roughly 12% of the United States GDP, has just surpassed Apple (NASDAQ: AAPL) to become the world’s most valuable publicly-traded company in terms of market capitalization.

As institutional investors are already mistrustful of ever-increasing AI spending, a further shift in sentiment could potentially see plenty of Nvidia’s impressive 193.29% gains on a year-to-date (YTD) basis erased.

A strategic pivot and strong demand will likely protect NVDA stock

After an August 27 report from Hindenburg Research alleged widespread accounting fraud, the semiconductor venture delayed the filing of its annual report to the SEC, and SMCI stock fell by 30% in short order.

On October 30, it became public that its auditor, Ernst & Young, had resigned six days earlier — and another 30% crash ensued.

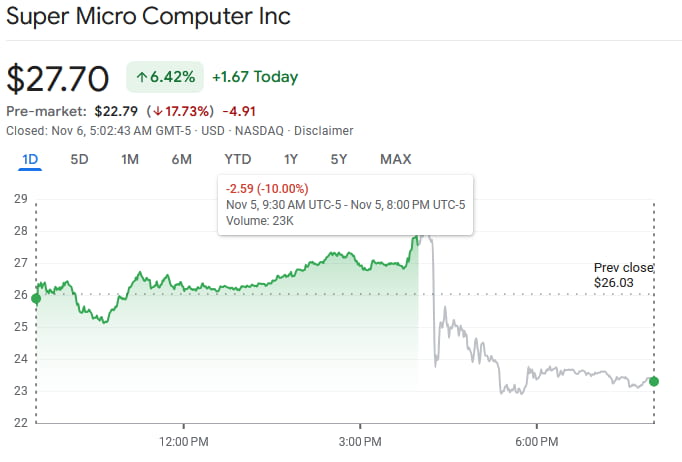

On November 5, the company released its Q1 2025 earnings report. Amidst significant losses, Super Micro Computer also announced that it is unable to predict when it will be able to file its delayed 10-K form, increasing the risk of delisting. In the immediate aftermath of the announcement, SMCI’s share price plummeted by 10%, currently at $23.30.

Nvidia does not directly name its largest customers. A look at the semiconductor titan’s latest 10-Q filing reveals that 46% of total revenue comes from just 4 customers. Per Bloomberg supply chain analysis, in August, SMCI accounted for 9% of total revenue.

While that is worrisome at first glance, the chipmaker has already taken steps to shift SMCI orders to other clients — and with the latest line of Blackwell architecture chips being sold out for the next 12 months, there’s little doubt that Nvidia can successfully pivot.

Investors should note, however, that markets could react intensely to SMCI’s delisting, even though it would not fundamentally alter NVDA’s growth prospects. The worst-case scenario would be panic caused by delisting followed by an unexpectedly weak earnings call from Nvidia, although the latter is unlikely. For the time being, the brainchild of Jensen Huang maintains a competitive edge in a high-demand market strong enough to weather the storm.

Featured image via Shutterstock