Across 2024, the general economy has faced several headwinds impacting stocks in various ways, which has had the potential to trigger a shift in investor psychology.

In this light, analysis indicates that amid the current economic situation, where data is expected to influence investor sentiment, the current stock market investment behavior appears bulletproof to any outcomes, according to The Kobeissi Letter’s observation in an X post on October 4.

Specifically, the analysis centered on the jobs report and elaborated how beating, missing, or aligning with expectations, the message is simple: “Buy stocks.”

In arriving at this analysis, The Kobeissi Letter noted that the Labor Department’s September jobs report showed the U.S. economy added 254,000 jobs—107,000 more than anticipated. Markets reacted predictably by pushing the S&P 500 up 48 points, even though the “Fed pivot” had already been priced in. At this point, investors are anticipating the index will push to a record high of 6,000.

This market response is even more surprising because the unemployment rate fell to 4.1%, just shy of breaking the 4.0% threshold. This should have been viewed as a “hawkish” sign, indicating economic strength that could dissuade the Federal Reserve from cutting rates.

Yet, the market interpreted this as a buying opportunity. Even with the 10-year Treasury note yield soaring toward 4%, a level that typically cools equity markets, the risk appetite is stronger than ever.

Historically, positive job data might have caused markets to anticipate tighter monetary policy, pulling back from stocks. Conversely, weaker-than-expected jobs data would signal a possible recession, which would also be a bearish indicator. But 2024 seems to have turned these rules upside down.

Anticipation for more rate cuts

As The Kobeissi Letter pointed out, investors are convinced the Federal Reserve will either cut rates soon or engineer a “soft landing” for the economy regardless of what happens. This confidence is driving a near-universal belief that all news is good news—whether it shows strength or weakness.

The analysis also identified how the job data report influences investor psychology. For instance, a better-than-expected jobs report makes investors see this as a sign that the economy is strong enough to avoid a recession, thus signaling the need to buy equities.

On the other hand, a worse-than-expected jobs report leads investors to predict that the Federal Reserve will be forced to cut rates, injecting more liquidity into the market and prompting them to buy stocks.

Lastly, when the job report aligns with expectations, investors believe the Federal Reserve is on track for a soft landing—balancing inflation and growth without triggering a recession. Once again, the response is to buy stocks.

To this end, this thinking pattern, where every scenario leads to stock-buying, demonstrates the power of investor sentiment in driving markets, even when traditional signals suggest caution.

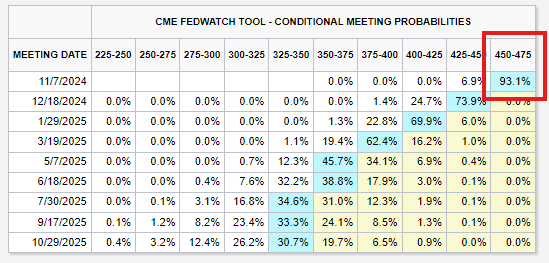

What’s remarkable is how markets have priced in the “Fed pivot,” where the central bank may reverse course and cut rates. Following the September jobs report, the likelihood of a 25-basis point rate cut in November soared to 93%, up from 50% before the data release. Investors seem unfazed that rate hikes are off the table for now and remain bullish on equities.

Market ignores job revisions

The upward revision of August’s jobs report—from 142,000 to 159,000—further fueled the stock market rally. Job numbers were revised higher for the first time since April, a move that would typically temper market exuberance. But in today’s environment, even this was seen as bullish.

The S&P 500, which recently dropped to 5680, quickly rebounded and is now flirting with the 5750 mark. The Kobeissi Letter anticipated this “higher low” and predicted further gains. But the question remains: can this seemingly invincible stock-buying mentality last?

Meanwhile, as bullish sentiments seem to dominate the market, some analysts are warning that it could be a precursor to a recession. Specifically, Henrik Zerberg maintains that the market will rally to a new high before crashing to historical levels.