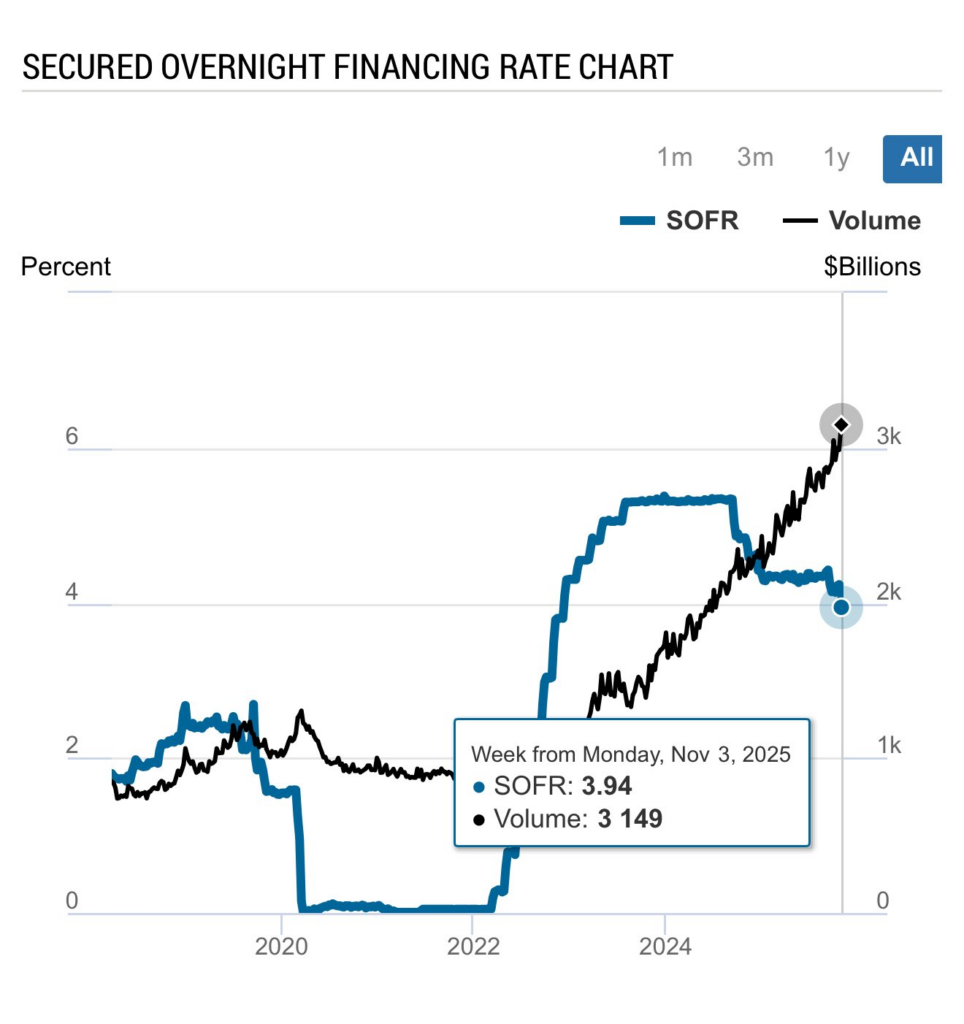

On November 6, the Secured Overnight Financing Rate (SOFR) plunged to 3.92%, its lowest point in two years, setting off alarm bells across global markets.

The sudden drop of 30 basis points from 4.22% on October 31 marked a significant shift in the financial landscape, with an expert warning it could signal something much more severe.

Notably, SOFR is a key benchmark governing $397 trillion in financial contracts worldwide, and when it moves, the effects ripple through everything from corporate loans to adjustable-rate mortgages.

Reacting to the data, science author Shanaka Anslem Perera pointed out in an X post on November 9 that this decline is not just a rate cut but a massive liquidity influx.

While the drop could save borrowers up to $50 billion annually, Perera cautioned that it signals rising systemic stress.

“The benchmark that controls $397 trillion in global contracts just signaled something catastrophic.This is not a rate cut. This is a liquidity flood,” he said.

Since replacing LIBOR in 2023, SOFR has underpinned financial products like derivatives and corporate loans, impacting trillions in assets. A sub-4% SOFR has often preceded major asset bubbles, and Perera warned that cheap credit doesn’t solve economic growth issues, it merely masks them.

Masking a recession

It’s worth noting that the Federal Reserve has already cut interest rates by 150 basis points this year, injecting liquidity into markets. While this might seem like relief, the surge in SOFR is raising concerns about global contagion.

Perera noted that the sudden crash of this metric suggests that central banks are preparing for a recession they may not yet be willing to admit.

“SOFR is not just a rate. It is the early warning system for systemic stress. When the world’s most important number collapses this fast, it means central banks are terrified. They are easing into a recession they cannot admit is coming,” he added.

At the same time, Perera warned that the situation remains precarious. If Q4 GDP falls short or inflation accelerates, SOFR could sharply reverse, potentially triggering another liquidity crisis like the 2019 repo disruptions.

Now, if the Fed continues on its current path, credit bubbles could continue inflating, eventually bursting with widespread global repercussions.

Featured image via Shutterstock