As the S&P 500 seeks to claim the 7,000 record high, insights from a trading expert suggest the benchmark index could be headed for a correction in the coming months.

Notably, the index has seen volatility in recent months but remains near record levels. As of press time, the S&P 500 was trading at 6,941, down 0.33%.

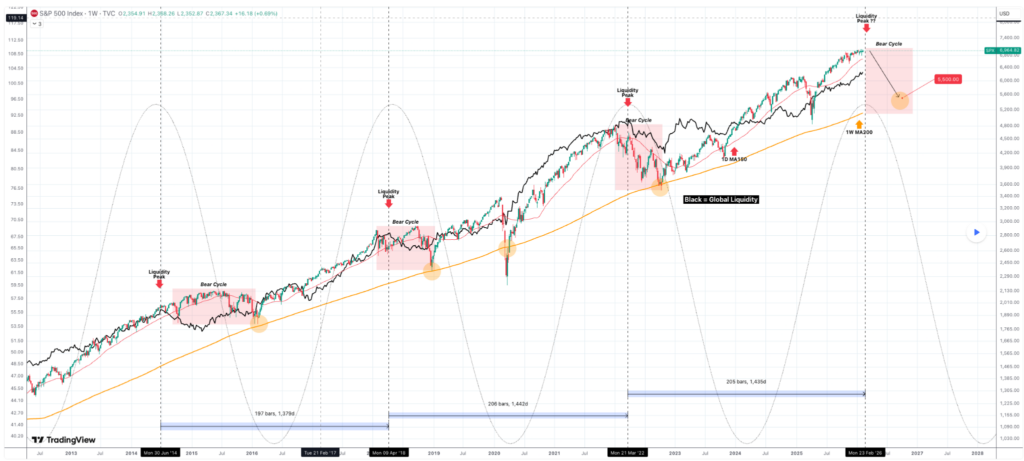

Regarding the outlook, analysis from TradingShot suggests the S&P 500’s three-year bull cycle, which began after the October 2022 bottom, may be nearing a critical turning point, with liquidity indicators flashing warning signs.

Since the 2009 housing crisis low, major bear cycles have typically bottomed at or near the 200-week moving average (MA).

Notably, the 2022 inflation-driven decline followed that pattern, rebounding precisely from that level.

However, since October 2022, the index has not retested the 200-week average, and even last year’s tariff-related correction failed to reach it, a stretch that historically signals overheated, late-stage bull market conditions.

At the same time, the M2 Global Liquidity Index appears to be entering a cyclical peak zone. Liquidity has historically peaked roughly every four years, aligning with major market tops. The next projected peak falls around the week of February 23, 2026, placing the market within that window.

Key S&P 500 levels to watch

If liquidity is topping, the implication is that the S&P 500 could transition into another systemic bear cycle, with a typical retracement potentially pulling the index back toward the rising 200-week moving average, projected near the 5,500 level.

At the same time, U.S. equities are also flashing a historic valuation signal, with the S&P 500 earnings yield falling to near century lows based on Shiller CAPE data.

In this line, according to Barchart, the yield is hovering around 3%, a level only breached during the late 1990s dot-com bubble.

As the inverse of the P/E ratio, the earnings yield shows how much investors earn per dollar invested. Lower yields signal higher valuations, indicating investors are accepting thinner returns for exposure to U.S. stocks.

Historically, yields surged above 15% during crises such as the Great Depression and rose again in the 1970s and early 1980s, while strong growth periods pushed them lower.

Although not a guaranteed warning of a downturn, current levels suggest valuations are stretched, leaving little room for disappointment in earnings or the broader economy.

Featured image via Shutterstock