Summary

⚈ Strong fundamentals support recent gains, but risks remain due to industry volatility.

⚈ Analysts expect a potential 20% stock drop despite upcoming earnings growth.

Cargo company ZIM Integrated Shipping Services (NYSE: ZIM) has the highest annual dividend yield, 41.73%, which is attractive to income-seeking investors.

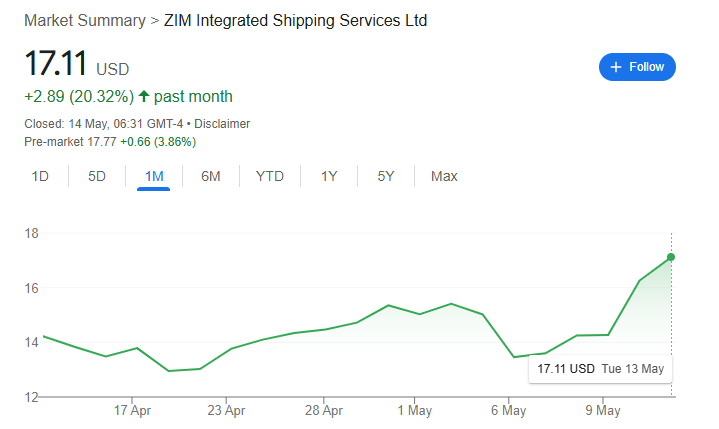

Currently offering a quarterly dividend of $1.79, ZIM’s share price has surged more than 20% in the past month, closing at $17.11 in the latest session. This rally follows renewed optimism after the U.S. and China made progress in ending the trade tensions, a development that could spur global shipping activity.

For investors considering a position in the cargo giant, ZIM appears undervalued, especially with a price-to-earnings (P/E) ratio of 0.96. This suggests the company is earning nearly as much per share as its current stock price, a rarity in today’s market.

Still, such high yields can raise red flags. ZIM’s 41.73% dividend might appeal to short-term income chasers, but it also reflects the volatile nature of the shipping industry, which is subject to swings in freight rates, fuel prices, and global trade flows.

Moreover, dividend yields above 10% often signal market caution. At 41%, any earnings or shipping demand decline could force ZIM to slash its payout.

ZIM stock fundamentals

That said, the company still boasts emerging fundamentals that may support future growth. ZIM could be poised for a broader rebound, potentially echoing its explosive 2020–2021 performance, when soaring container rates drove profits sharply higher.

With most of its fleet serving the Asia–North America trade route, ZIM is well-positioned to benefit from any increase in shipping demand as trade tensions continue to ease.

The firm has also been active in terms of innovation. Back in November last year, ZIM launched a global rollout of smart containers using Hoopo’s solar-powered trackers, improving cargo visibility and tracking efficiency.

Meanwhile, in April, the firm secured 10 new dual-fuel LNG vessels in a $2.3 billion, 10-year charter deal, expanding its capacity ahead of anticipated demand.

Investors are now watching closely for ZIM’s upcoming earnings report on May 19. Analysts expect earnings per share (EPS) of $1.66, up 121% year over year, and revenue of $1.73 billion, up 11%.

Is ZIM stock a buy?

Despite these positives, Wall Street remains cautious. A consensus from three analysts surveyed by TipRanks projects a 20% decline in ZIM’s stock over the next year, with a target price of $13.60.

ZIM’s unusually high dividend yield makes it compelling, but investors should understand the underlying risks. A low P/E ratio and exposure to a volatile industry mean this could be a high-risk, high-reward play.

Featured image via Shutterstock