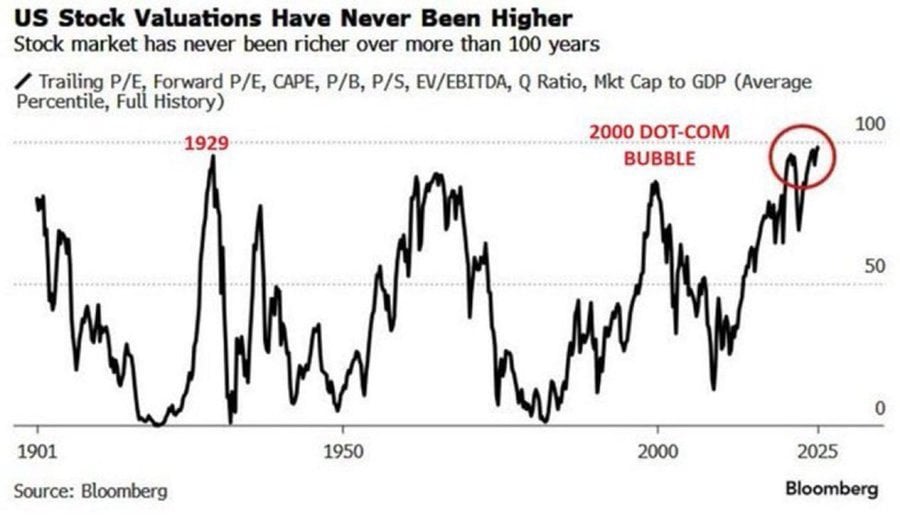

U.S. stock valuations have reached their highest levels in more than a century, surpassing both the peak of the Dot-Com Bubble in 2000 and the market conditions that preceded the Great Depression in 1929.

The finding is based on a Bloomberg valuation composite that combines trailing and forward price-to-earnings ratios, the Shiller CAPE ratio, price-to-book, price-to-sales, EV/EBITDA, Q Ratio, and market capitalization-to-GDP.

The indicator has now exceeded previous peaks recorded before the 1929 crash and the 2000 tech bubble, fueling debate over a potential stock market correction.

The milestone comes as U.S. equities continue to rally in 2026, driven largely by artificial intelligence-related stocks and strong earnings growth among a small group of mega-cap technology companies.

As of press time, the S&P 500 was trading at 7,511, up nearly 10% year-to-date.

According to the Bloomberg tracker, which measures the average percentile ranking of several major valuation metrics throughout market history, the latest reading places the U.S. stock market at its highest valuation level on record.

The Shiller CAPE ratio remains near 40, a level previously seen only during major market bubbles, including the late-1990s tech boom.

Meanwhile, the Buffett Indicator, which measures total stock market capitalization relative to U.S. GDP, has climbed above 230%, a level widely viewed as historically overvalued.

AI stocks leading stock market surge

The surge in valuations has been fueled by AI optimism, with heavy investment in data centers, semiconductors, cloud computing, and other AI infrastructure boosting earnings expectations. Cooling inflation and expectations for supportive monetary policy have also helped sustain demand for U.S. equities.

At the same time, several Wall Street firms have raised their year-end S&P 500 targets, citing AI-driven productivity gains and resilient corporate profits.

However, the market’s reliance on a small group of technology stocks has heightened concerns that any slowdown in AI-related growth could trigger a broader selloff.

The extreme valuation backdrop has prompted warnings of a stock market crash from some analysts, who argue that elevated multiples leave little room for disappointment.

Historically, periods of exceptionally high valuations have often been followed by weaker long-term returns and, in some cases, sharp corrections. Risks cited by bears include slowing economic growth, weaker earnings, AI spending fatigue, geopolitical tensions, and shifts in monetary policy.

While a downturn is not inevitable, comparisons with 1929 and the 2000 Dot-Com Bubble point to the unprecedented scale of today’s valuation extremes.