Social media giant Meta Platforms (NASDAQ: META) is facing renewed Wall Street caution after MoffettNathanson lowered its price outlook.

The firm’s analyst Michael Nathanson reduced the META target to $750, citing mounting concerns over margin deterioration as the company accelerates its AI infrastructure spending. Notably, the new target still implies a 25% surge from the last closing value of $597.

According to the assessment, Meta is entering a cost cycle unlike previous periods of technology-sector resets.

While revenue remains solid, visibility on future costs is becoming increasingly difficult as the company’s capital outlays expand and its operating structure absorbs the weight of long-term AI bets.

The analyst noted that the lack of a mature enterprise or cloud business to offset these expenses adds to the risk profile, raising doubts about whether earlier efficiency gains can be preserved.

Nathanson added that the company had been too relaxed in managing expenses earlier this year, allowing pressure to build as its spending trajectory steepened.

The firm now expects margin compression in the fourth quarter and through 2026, noting that Reality Labs’ rising costs and heavy AI infrastructure build-out represent sizable incremental burdens.

At the same time, operating margin pressure may persist for up to two years as these investments move through the system.

Wall Street bullish on META stock price

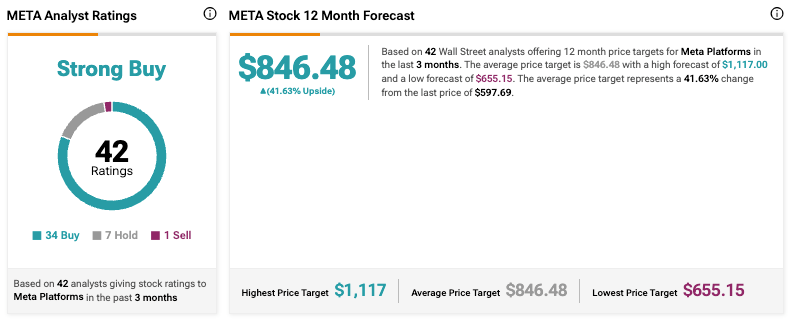

Despite the warning, the broader Wall Street community remains bullish on META stock. Over at TipRanks, 42 analysts maintain a consensus ‘Strong Buy’ rating, comprising 34 ‘Buy’ recommendations, seven ‘Hold’, and only one ‘Sell’.

The analysts project an average 12-month price target of $846.48, representing a 41.63% upside from Meta’s price at press time. Forecasts range from a high estimate of $1,117.00 to a low of $655.15, indicating broad confidence in Meta’s growth trajectory despite market uncertainties.

Featured image via Shutterstock