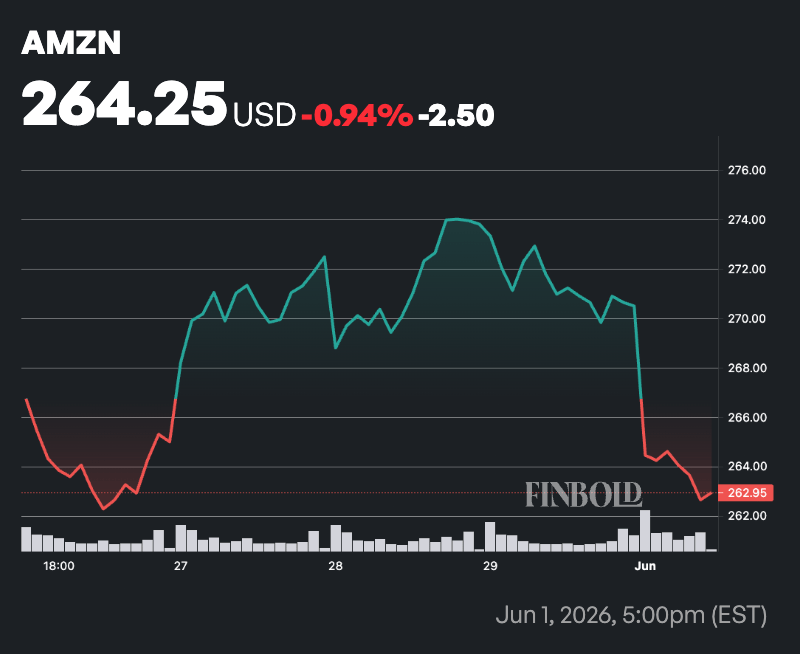

Although Amazon (NASDAQ: AMZN) stock has faced increased weakness in recent weeks, an analyst at Truist Securities has raised his price target on the e-commerce giant while reiterating a ‘Buy’ rating.

Truist analyst Youssef Squali increased Amazon’s price target to $320 from $310, implying about 15% upside from the stock’s press-time price of $261.

Squali raised estimates for AWS revenue growth in fiscal 2027 and beyond, arguing that market expectations may be underestimating the cloud platform’s expansion potential.

According to the analyst, AWS is positioned to benefit from large-scale artificial intelligence investments and partnerships, including reported commitments worth up to $100 billion involving AI companies Anthropic and OpenAI.

These agreements are expected to contribute to future revenue growth as related workloads move into production.

The analyst also pointed to Amazon’s next-generation AI chips as a potential catalyst. Expectations include the continued rollout of Trainium3 processors and the planned launch of Trainium4 in the second half of fiscal 2027.

While Amazon is expected to increase capital expenditures to support AI infrastructure, Truist believes revenue growth could outpace those spending increases.

The firm noted that consensus forecasts may be underestimating AWS revenue growth while overestimating the impact of higher capital expenditures.

Wall Street remains bullish on AMZN shares

As a result, Truist’s AWS projections remain above broader Wall Street estimates, which remain generally bullish on AMZN shares.

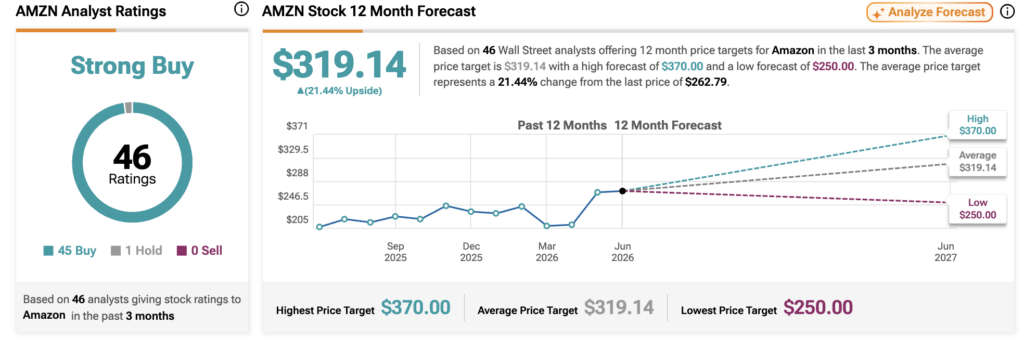

According to analyst consensus data from TipRanks, Amazon holds a ‘Strong Buy’ rating based on 46 analyst reviews issued over the past three months. Of those ratings, 45 analysts recommend buying the stock, while one suggests holding. No analysts currently rate Amazon as a sell.

The average 12-month price target for Amazon stands at $319.14, implying potential upside of 21.44%.

The highest price target on Wall Street is $370, representing potential gains of more than 40% from current levels. Meanwhile, the lowest target is $250, indicating limited downside risk relative to the current share price.

The consensus outlook reflects continued confidence in Amazon’s long-term growth prospects, supported by its dominant position in e-commerce, expanding advertising business, and leadership in cloud computing through Amazon Web Services (AWS).