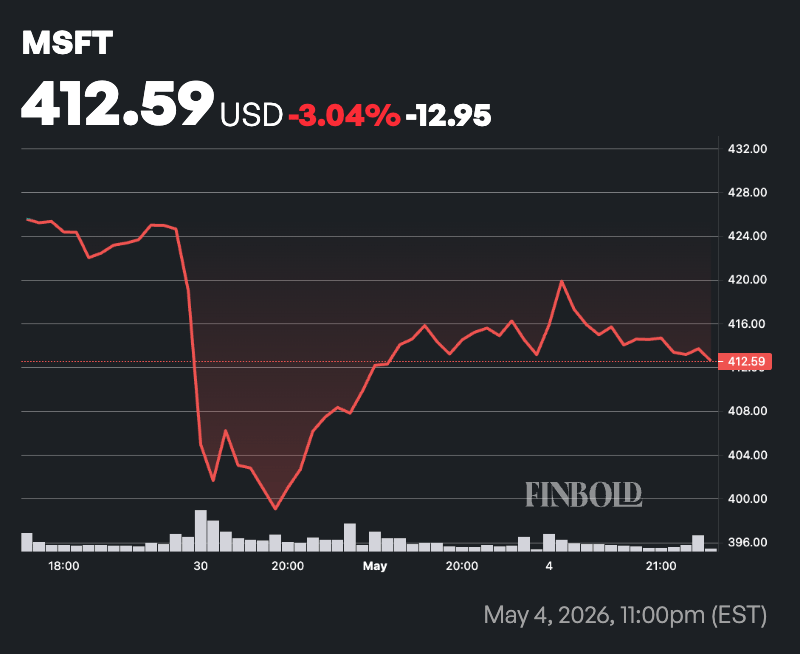

Microsoft’s (NASDAQ: MSFT) continued advances in the artificial intelligence space are prompting bullish projections from Wall Street analysts.

In the latest update, KeyBanc analyst Jackson Ader reiterated an ‘Overweight’ rating on Microsoft and maintained a $600 price target, implying about 45% upside from the stock’s recent trading level near $413.

The analyst maintained a positive outlook on Microsoft’s cloud and artificial intelligence businesses, citing continued Azure growth, rising adoption of Copilot products, and improving operating efficiency as key drivers of the company’s long-term expansion.

According to the update, Microsoft’s operating margins exceeded expectations, with forecasts calling for more than 100 basis points of expansion in fiscal 2026. Ader also highlighted that headcount is expected to decline by fiscal 2027, a move viewed as supportive of margin improvement and cost discipline.

The report further noted that Microsoft’s “leases not yet commenced” increased by more than $40 billion during the quarter, signaling significant future data center and AI infrastructure capacity as the company continues investing heavily to meet artificial intelligence demand.

Despite the bullish outlook, the analyst flagged some weakness in Microsoft’s Windows OEM and Devices segment, where revenue declined about 3% in constant currency. Further softness in the PC market is also expected in coming quarters.

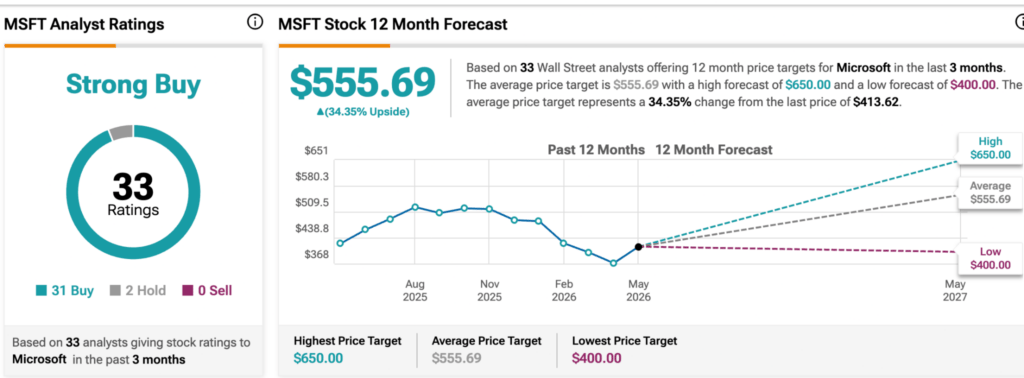

Meanwhile, broader Wall Street sentiment remains firmly positive on Microsoft stock. Based on ratings from 33 analysts tracked by TipRanks, the stock currently has a ‘Strong Buy’ consensus rating, with 31 buy ratings, 2 holds, and no sells.

Analysts’ average 12-month price target stands at $555.69, representing roughly 34% upside from current levels, while forecasts range from a low target of $400 to a high target of $650.

Microsoft stock fundamentals

The bullish outlook comes as Microsoft stock continues to attract strong investor sentiment following robust fiscal third-quarter 2026 results that topped Wall Street estimates on revenue and earnings.

The company posted revenue of $82.9 billion, up 18% year over year, while operating income climbed 20% to $38.4 billion. Microsoft Cloud revenue rose 29% to $54.5 billion, with Azure growth accelerating 40%, slightly ahead of expectations.

Despite the strong performance, investors reacted cautiously after Microsoft projected capital expenditures of about $190 billion for calendar 2026, significantly above previous forecasts. Third-quarter capital expenditures rose 49% year over year to $31.9 billion as the company expanded AI data center and infrastructure capacity.

Management pointed to strong long-term demand trends, supported by a $627 billion remaining performance obligation and continued enterprise AI adoption. CEO Satya Nadella also highlighted Microsoft’s growing focus on “agentic computing” and broader multi-model AI initiatives.