Palantir Technologies (NASDAQ: PLTR) has received a fresh vote of confidence from Wall Street, as Wedbush Securities reaffirmed its bullish stance on the stock.

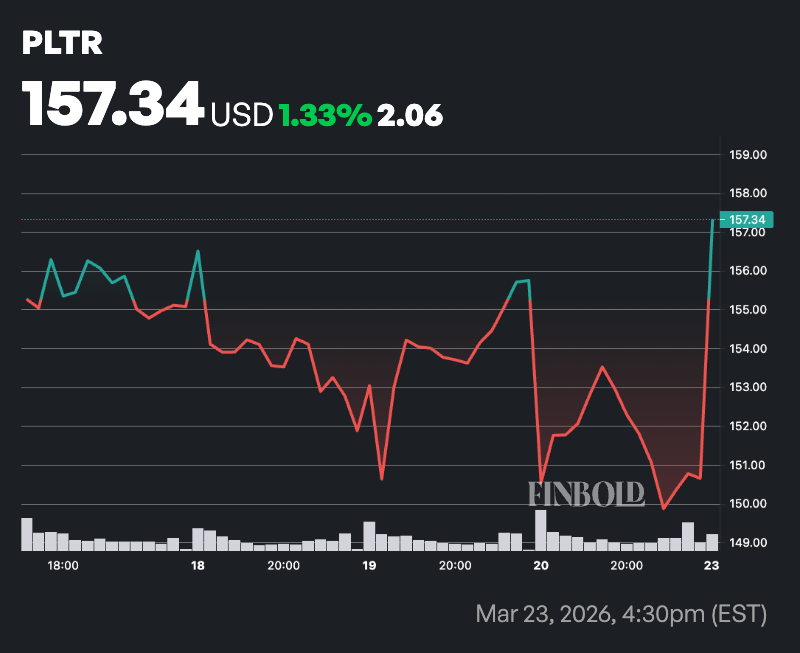

The firm’s analyst, Dan Ives, reiterated an ‘Outperform’ rating and maintained a price target of $230. With shares trading around $157 the target implies a potential upside of roughly 52%.

According to Ives, Palantir is gaining momentum across U.S. government agencies, particularly within the Department of Defense, where increasing exposure to IT budgets is helping drive new deal activity.

The note highlighted that federal contract traction is strengthening, supported by the company’s alignment with complex geopolitical and security needs.

Ives also pointed to Palantir’s software as well-positioned to address evolving defense and intelligence challenges, enabling the company to expand its footprint across key programs tied to the Pentagon.

Beyond government, the analyst sees Palantir on a strong path within the AI landscape, with its platforms increasingly embedded in high-value use cases. This positioning, combined with sustained deal wins across its federal portfolio, is expected to support long-term growth.

Wall Street bullish on PLTR stock

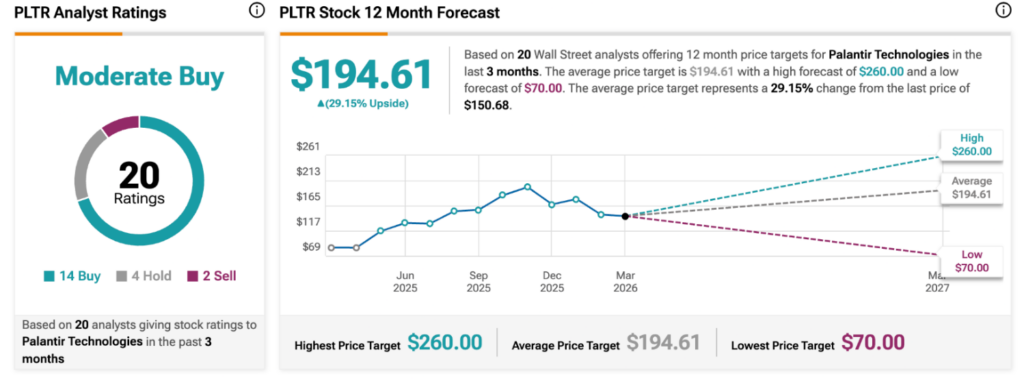

Beyond Ives, the broader Wall Street consensus remains bullish on the American software giant, which has enjoyed massive gains in recent years. Analysts tracked by TipRanks assign PLTR shares a ‘Moderate Buy’ rating based on 20 analysts.

The breakdown includes 14 buy ratings, four holds, and two sell recommendations, reflecting a broadly positive, though not unanimous, outlook on the company’s trajectory.

The average price target stands at $194.61, implying a potential upside of about 29.15% from the last recorded price of $150.68. The highest estimate stands at $260.00, while the lowest target is $70.

Despite the bullish outlook, analysts have flagged valuation concerns. Palantir’s forward price-to-earnings ratio exceeds 200x, with a price-to-sales multiple ranging from about 44x to 80x based on forward estimates, well above typical software and AI peers.

Critics argue this “priced for perfection” scenario means even minor slowdowns in growth, increased competition from tech giants, or macro headwinds such as tariff uncertainty could trigger downside risk.

Still, Palantir’s fundamentals remain strong, particularly in earnings performance. In Q4 2025, revenue surged 70% year over year, with 2026 guidance targeting roughly $7.19 billion.

Featured image via Shutterstock