Wall Street analyst Gordon Johnson of GLJ Research has warned that Tesla (NASDAQ: TSLA) stock could experience losses in 2025, citing severe distress for the company’s business.

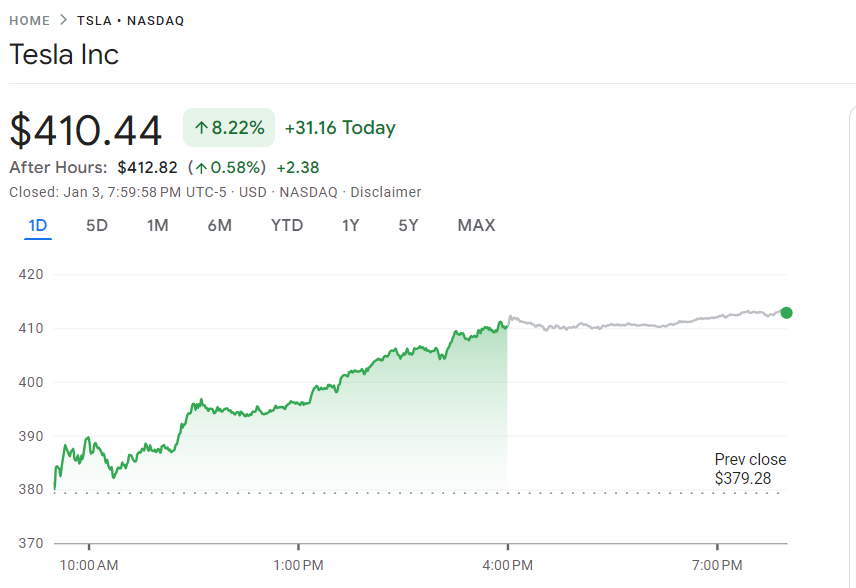

His warning comes after Tesla’s deliveries for the last quarter of 2024 failed to meet analyst consensus. Despite this, the stock has exhibited bullish sentiments in the short term, ending the January 3 session up over 8%, valued at $410.44.

According to Johnson, Tesla’s business is showing concerning signs, with sales declining for the first time in its history and margins likely to experience a ‘blood bath’ when 2024 earnings are released, he said in an X post on January 4.

“Things are bad for $TSLA’s actual biz. Sales just went ex-growth for the first time ever, and margins will likely see an absolute bloodbath when Q4 earnings are reported,” he said.

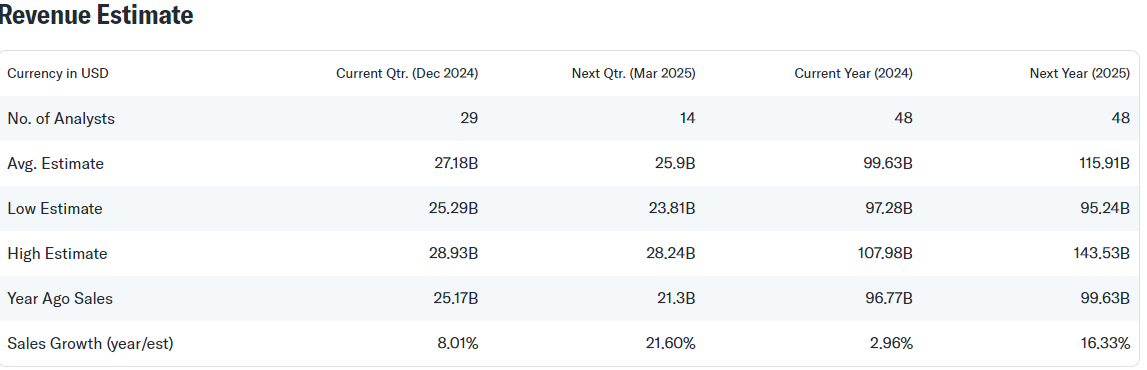

Notably, for Q4 2024, analysts expect an average Tesla revenue of $27.18 billion, an 8% increase from $25.17 billion in Q4 2023. Full-year 2024 revenue is projected at $99.63 billion, a modest 3% growth from $96.77 billion in 2023.

Tesla’s disappointing Q4 2024 deliveries

In Tesla’s Q4 report, the company posted 495,570 deliveries for the quarter, slightly below the 504,770 deliveries analysts had forecasted. Total annual deliveries for 2024 came to 1,789,226, down from 1.81 million in 2023.

While production numbers were close, the first annual drop in deliveries raises concerns, especially considering Tesla’s recent aggressive market share growth buoyed by CEO Elon Musk’s close ties to President-elect Donald Trump.

Tesla’s challenges in Q4 were compounded by a decline in demand and increased competition, with rivals like Hyundai and China’s BYD gaining ground. Notably, Musk had warned of slower growth in 2024, and the company appears to be facing the reality of that forecast.

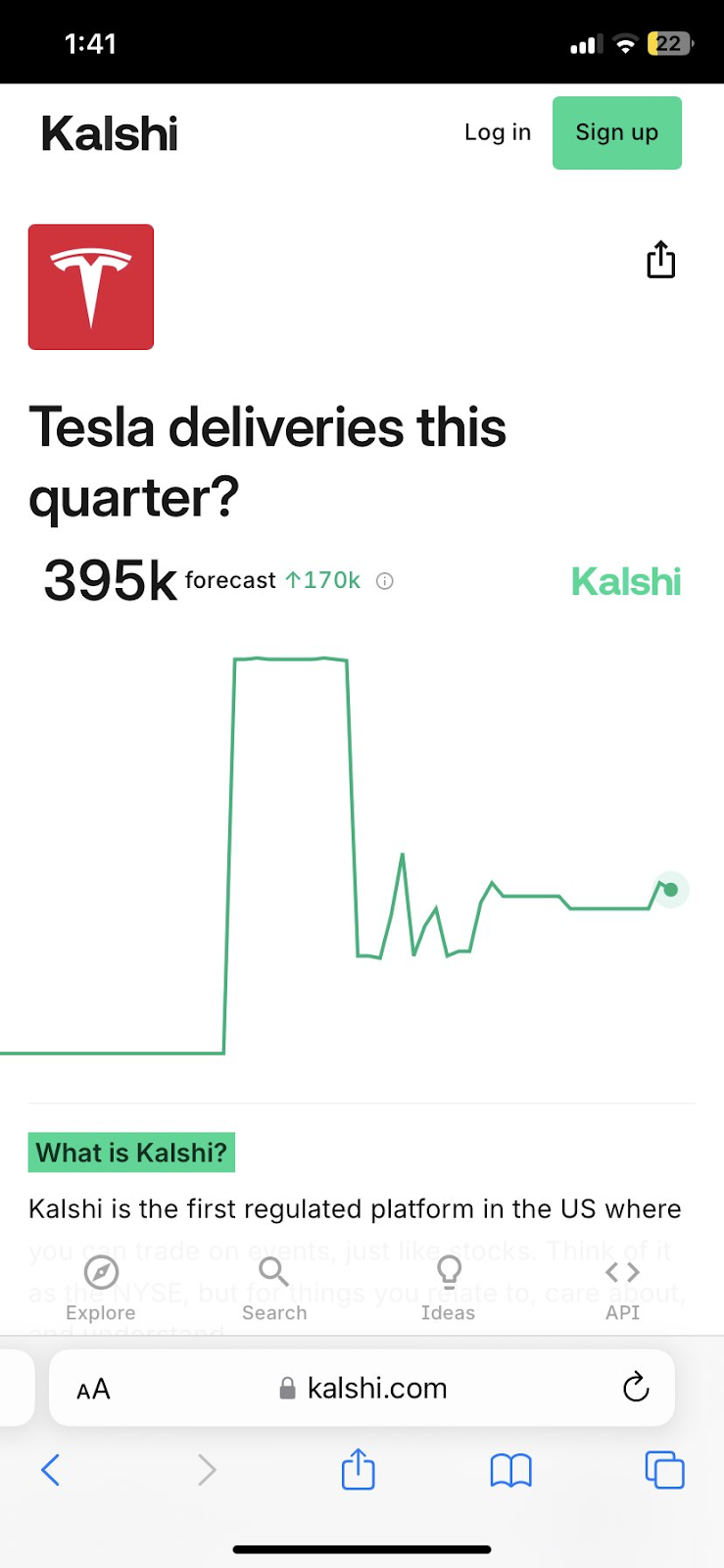

Johnson also cited forecasts from prediction markets for Tesla’s first-quarter 2025 sales, which are expected to fall to 395,000 vehicles, a 20% drop from Q4. Johnson described this decline as a “disaster,” suggesting that the company’s sales trajectory could worsen in the coming months.

What next for TSLA stock price

It’s worth noting that despite Tesla failing to meet analysts’ expectations on deliveries, the stock’s ability to rally during the January 3rd session led Johnson to attribute the move to a surge in options trading, with heavy call option buying helping to prop up its stock price.

To this end, he suggested that these moves, driven by speculative investors, are “legally manipulating” the stock price, allowing the “stock price bros” to ignore the company’s deteriorating fundamentals for now.

Looking ahead, Johnson predicted that 2025 will be “the year of the TSLA bear,” signaling a tough year for Tesla’s stock as it grapples with waning growth and increasing competition.

Johnson has long retained a bearish outlook on Tesla, warning that the stock is likely to crash and that the company is overvalued.

JPMorgan (NYSE: JPM) also shared a bearish outlook, warning that delivery issues and regulatory changes, like the expiration of the Clean Vehicle Credit and reduced zero-emission vehicle credits, could cost Tesla $3.2 billion—40% of its 2024 EBIT estimate. Consequently, JPMorgan maintained an ‘Underweight’ rating on Tesla with a $135 price target.

Regarding Tesla’s future, as reported by Finbold, Canaccord Genuity analyst George Gianarikas raised TSLA’s share price target from $298 to $404, maintaining a ‘Buy’ rating due to optimism about its growth in EVs, AI, and robotics.

Wedbush’s Dan Ives sees Tesla as a strong buy, highlighting its broader tech potential, while Truist’s William Stein anticipates challenges from additional discounts impacting Tesla’s financials.

Counter-narrative to Tesla’s bearish views

Indeed, while Tesla faces delivery challenges and competition, its advancements in Full Self-Driving (FSD) and AI development provide a counter-narrative to bearish views.

Although currently speculative, these technologies are projected to help the EV maker solidify its market position, with some analysts projecting that the company is likely to thrive under a Donald Trump administration with friendly regulations.

At the same time, despite competition from BYD, Tesla’s vision-based AI, strong brand, and integrated ecosystem create significant barriers, suggesting its innovations could help navigate a slowing EV market.

Featured image via Shutterstock