Wall Street analysts are reassessing their outlook on Rivian Automotive (NASDAQ: RIVN) as the electric vehicle maker navigates a volatile start to the year.

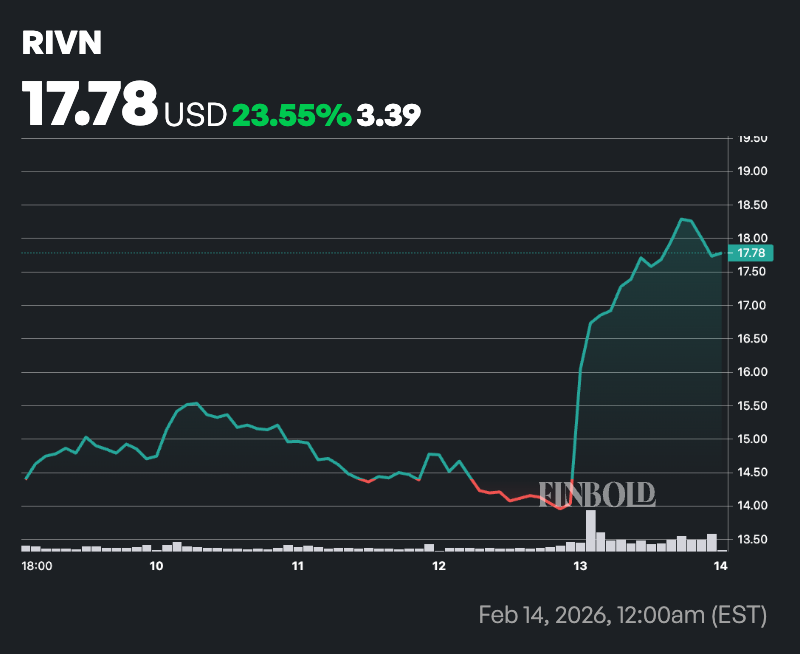

Notably, the stock surged significantly in the last trading session after the company beat earnings expectations.

For the fourth quarter of 2025, Rivian reported an adjusted loss of $0.54 per share, narrower than the $0.68 loss analysts had projected. The earnings beat highlights improved efficiency at a time when many EV peers are facing margin pressure.

For the full year 2025, consolidated revenue rose 8% year over year to $5.39 billion, up from $4.97 billion in 2024.

Investors also welcomed Rivian’s updated 2026 delivery guidance of 62,000 to 67,000 vehicles, reflecting expected growth as production of its next-generation R2 platform ramps up. The outlook signals the company’s shift toward becoming a higher-volume EV competitor.

In response, RIVN shares jumped 26% at the close of Friday’s session to trade at $17.73. However, year to date, the stock remains down nearly 9%.

Wall Street’s take on RIVN stock

Regarding the stock outlook, UBS moved its rating to ‘Neutral’ from ‘Sell’ and raised its price target to $16 from $15. The firm’s analyst, Joseph Spak, said the risk-reward profile now appears more balanced following a valuation reset in the stock.

UBS also pointed to Rivian’s 2026 delivery guidance of 62,000 to 67,000 vehicles, which came in better than feared and could support a stronger exit rate into 2027 if execution improves.

At the same time, UBS cautioned that near-term risks remain. The bank highlighted limited upside to 2026 guidance and flagged execution challenges tied to a sharp production ramp in the second half of the year, implying a significant increase in output.

It also noted that while initial demand appears intact, Rivian may require near-term price reductions to sustain momentum. The company is still burning cash, and positive EBITDA is not expected for several years.

In a more bullish call, Deutsche Bank upgraded Rivian to ‘Buy’ from ‘Hold’ and raised its price target to $23 from $16. The bank’s analyst, Edison Yu, cited inflecting fundamentals, a de-risked 2026 outlook, and improving vehicle costs and margins as key drivers behind the more optimistic stance.

Deutsche Bank also emphasized that Rivian’s upcoming R2 launch, expected in the second quarter, could mark an important milestone for the company. According to the firm, cost improvements and a stabilizing competitive landscape, as some peers slow their electric vehicle transitions, are helping strengthen Rivian’s positioning heading into the next phase of growth.

Featured image via Shutterstock