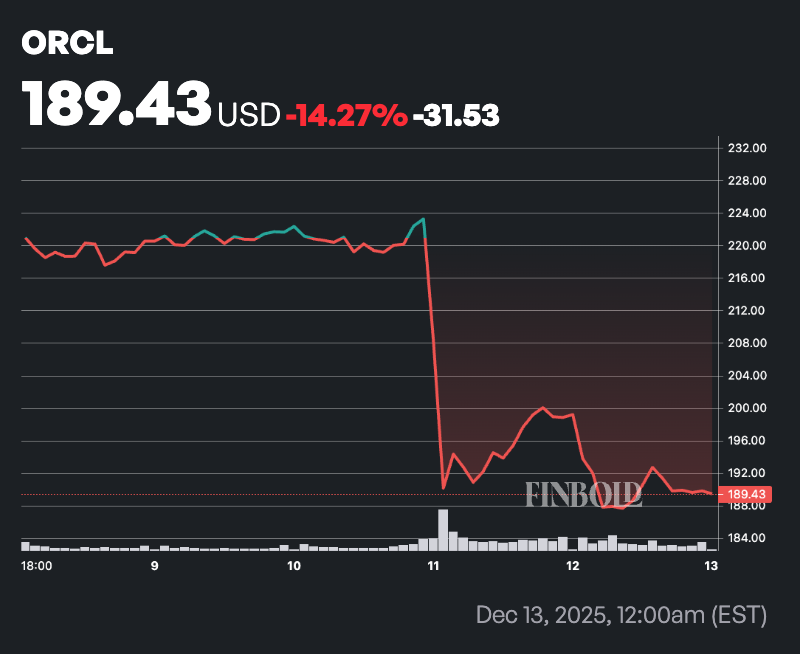

Although Oracle’s (NYSE: ORCL) stock price plunged on Friday in reaction to the company’s financials, a section of Wall Street remains confident the equity is likely to rally over the next 12 months.

As of press time, ORCL shares traded at $189.97, down more than 4% at the close of the Friday session. Meanwhile, year-to-date, the stock is up nearly 15%.

Notably, Oracle shares fell after the company reported second-quarter earnings that beat expectations but issued weaker-than-forecast guidance and flagged sharply higher spending on artificial-intelligence infrastructure.

Adjusted earnings came in at $2.26 per share, well above Wall Street estimates, driven largely by a $2.7 billion sale of its Ampere stake. Revenue rose 14% year over year to $16.06 billion but missed forecasts.

The correction emerged as investors focused on rising costs, after Oracle lifted its full-year capital expenditure outlook to $50 billion, largely to build out AI-optimized data centers and cloud infrastructure.

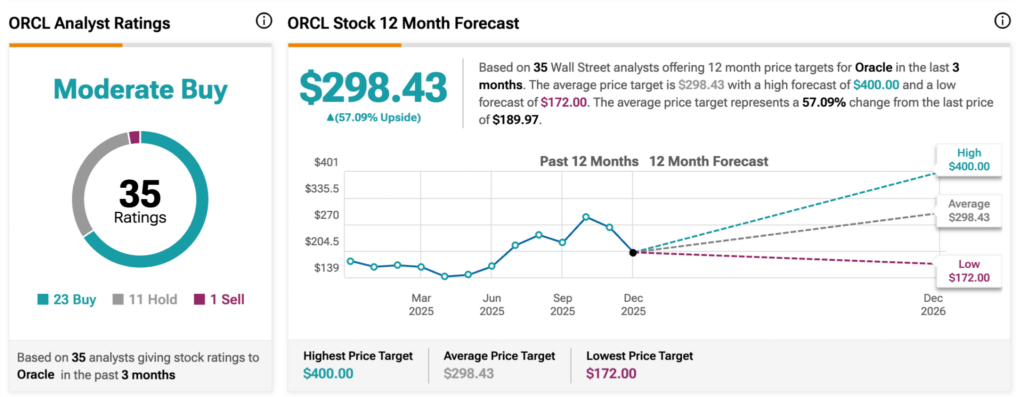

Wall Street bullish on ORCL stock

On Wall Street, 35 analysts tracked by TipRanks have assigned a ‘Moderate Buy’ rating to the technology stock. Of these, 23 recommend ‘Buy’, 11 suggest ‘Hold’, and one advises ‘Sell’.

The average 12-month price target stands at $298.43, representing a potential upside of 57.09% from ORCL’s last closing price. The highest forecast reaches $400, while the lowest sits at $172.

Among them, Mizuho’s Siti Panigrahi on December 11 reiterated an ‘Outperform’ rating and a $400 price target on Oracle following the company’s mixed fiscal second-quarter results. The firm argued that near-term concerns around a modest revenue miss and rising AI-related spending do not undermine Oracle’s long-term growth outlook. Mizuho acknowledged weakness in the license business but noted cloud results were broadly in line, with revenue up 9.67% over the past year to $59.02 billion. The firm also highlighted management’s efforts to address financing concerns through “bring your own chip” and GPU rental models that limit upfront capital needs.

On the same date, Scotiabank’s Patrick Colville cut his price target on Oracle to $260 from $360 while maintaining a ‘Sector Outperform’ rating. The bank flagged Oracle’s decision to reaffirm, rather than raise, its fiscal 2026 OCI outlook. It noted that near-term earnings growth appears limited, with next-quarter profit guidance only in line with Street expectations. Scotiabank said the pullback does not alter its long-term view, pointing to Oracle’s scale, double-digit revenue growth, and strategic advantages in GPU-as-a-service, access to leading-edge silicon, and capital-raising capacity.

Featured image via Shutterstock