The stock of Advanced Micro Devices (NASDAQ: AMD) has been on something of a roller coaster ride in recent months, having recorded both stellar rallies and staggering drops.

Still, AMD shares have overall underperformed as they are, at their press time price of $119.95, 25.03% in the red in the last 12 months.

Such a situation is somewhat surprising given that the company is the second-most prominent player in the otherwise exceptionally strong semiconductor industry and has actively participated in the ongoing artificial intelligence (AI) boom.

AMD’s struggles can largely be linked to its inability to really chip away at Nvidia’s (NASDAQ: NVDA) dominance, a competitiveness issue that has only been growing in relevance in the initial weeks of 2025.

Wall Street remains bullish about AMD

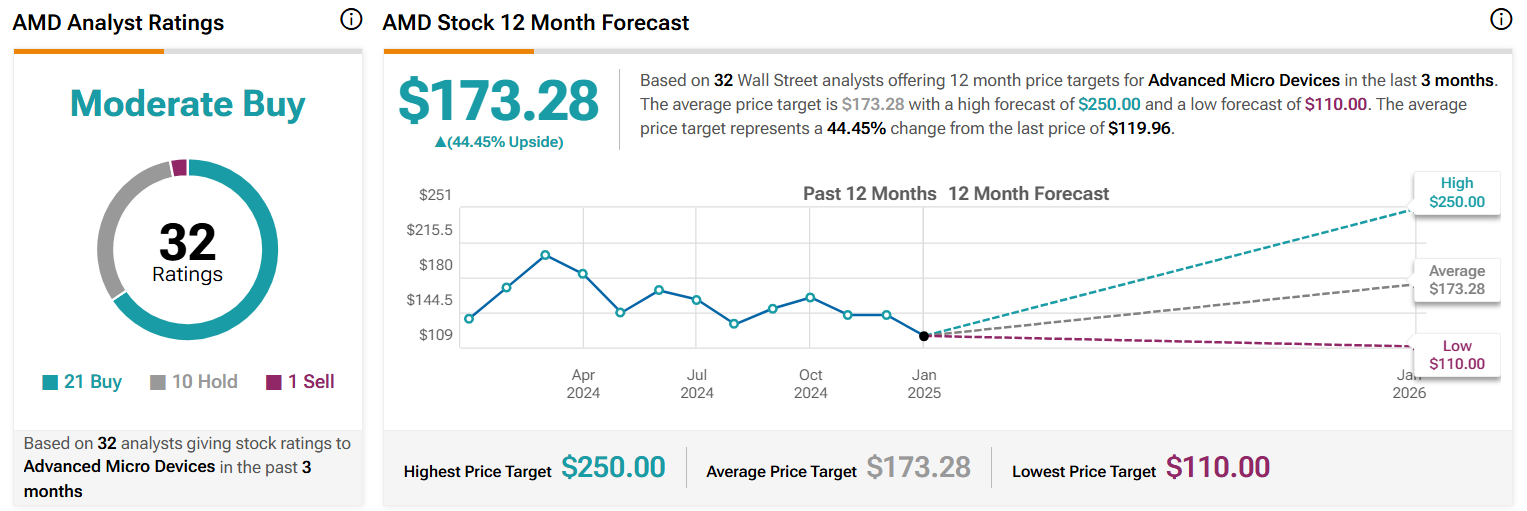

Despite the stock market situation, Wall Street experts remain generally optimistic about Advanced Micro Devices stock, as evidenced by the AMD shares’ average ‘moderate buy’ rating on the stock analysis platform TipRanks.

As data retrieved on January 16 shows, 21 analysts believe AMD is a ‘buy,’ 10 are ‘neutral,’ and only 1 estimates the stock is a ‘sell.’ Similarly, the chipmaker’s equity is generally forecasted to rise 44.45% in the coming 12 months to $173.28.

Furthermore, the Street high forecast – assigned by Rosenblatt Securities in late October – sees AMD stock more than doubling in value within 52 weeks to $250, and even the Street low of $110 – given by HSBC on January 8, predicts only a minor drop from the press time value.

January brings a series of stock price target downgrades for AMD

Still, the limited downside in HSBC’s price target should not mask the relatively dire assessment that came with it.

Indeed, Frank Lee justified the January 8 downgrade by pointing out that the lukewarm demand for Advanced Micro Devices’ MI325 GPU severely limits the hopes the firm could gain market share against the much larger Nvidia in 2025.

Such an opinion has been widely echoed in other January revisions as every readjustment of AMD stock that was provided in the first half of the month has been downward.

For example, Goldman Sachs’s (NYSE: GS) Toshiya Hari pointed toward a loss of confidence in the semiconductor company’s ability to continue growing when he revised his price target from $175 to $129 on January 10.

The latest reassessment, given by Wolfe Research’s Chris Caso on January 16, also added the lowered expectations for AMD’s data center GPU revenue growth in 2025.

“We now expect $7bn in DC GPU revenue for CY25 vs. our prior expectation of $10bn+,” Wolfe Research stated.

Not all January AMD stock revisions bearish

Despite all Advanced Micro Devices stock price targets getting lowered in January, not all analysts recommend selling or merely holding the stock. For example, despite reducing the forecast from $180 to $160 on January 10, Mizuho stuck to a ‘buy’ rating.

Similarly, despite making a massive revision from $220 to $150, KeyBanc also continued rating AMD as ‘overweight’ – ‘buy’ – and Loop Capital even initiated its coverage of the chipmaker with a positive assessment and a $175 target, demonstrating continued confidence that the firm can continue gaining market share as it improves its technology and infrastructure.