While the stock price of American artificial intelligence (AI) cloud computing firm CoreWeave (NASDAQ: CRWV) continues to fly high, Wall Street is cautious about its long-term outlook.

Since its initial public offering (IPO) in late March, the stock has jumped nearly 360%, fueled by investor excitement and strong backing from Nvidia (NASDAQ: NVDA), which provides the GPUs powering CoreWeave’s AI infrastructure.

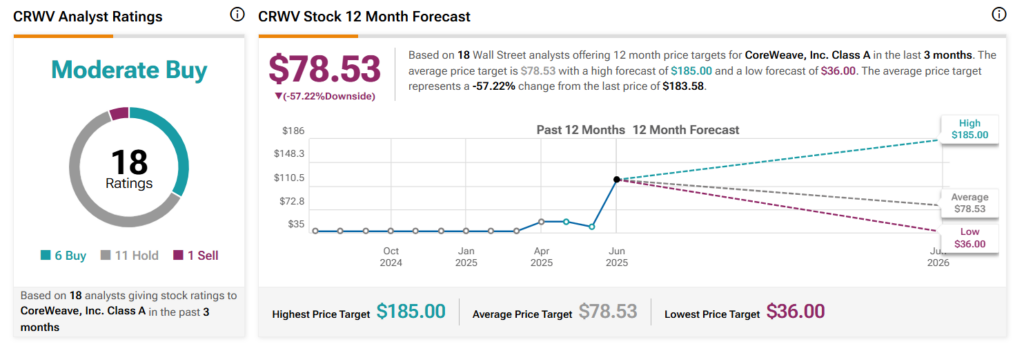

As of the last market close, shares of CRWV were trading at $183.58, an increase of almost 8% for the day.

Despite this positive momentum, analysts are urging caution. Data from TipRanks, which includes input from 18 analysts, shows that the average 12-month price target for CRWV is $78.53; this suggests a potential decline of about 57% from current prices.

Price targets differ widely, ranging from a low of $36 to a high of $185. Overall, there is a ‘Moderate Buy’ consensus on the stock, with six analysts rating it a ‘Buy,’ 11 a ‘Hold,’ and one a ‘Sell.’

Analysts’ take on CRWV stock

In recent analyst activity, Bank of America’s Bradley Sills downgraded the stock from ‘Buy’ to ‘Hold’ on June 16 while increasing the price target from $76 to $185. Sills expressed concerns about the stock’s valuation, noting its sharp rise after earnings and a high 25x 2027 EV/EBIT multiple. Yet, he remains optimistic about CoreWeave’s future, citing the growing demand for AI infrastructure, a $4 billion expansion related to OpenAI, new partnerships with hyperscalers, and a projected AI market size of $206 billion by 2027.

On the other hand, DA Davidson holds a more negative view. On June 9, analyst Gil Luria reiterated an ‘Underperform’ rating with a $36 target, raising concerns about CoreWeave’s financial structure. He pointed out that the company does not have upfront equity contributions or provide returns to shareholders during contract periods. Luria also noted issues with CoreWeave’s balance sheet, which shows $590 million in new debt, an existing $11.9 billion burden, and a low current ratio of 0.44.

Wells Fargo has adopted a more neutral stance, maintaining its ‘Equal Weight’ rating while increasing its price target from $50 to $60. Analyst Michael Turrin recognized impressive revenue growth and a $4 billion customer expansion but warned that these gains might impact FY25 margins. While the growth driven by AI is impressive, Turrin is hesitant about long-term challenges within the fast-changing AI landscape.

Lastly, Mizuho began coverage on May 16 with an ‘Outperform’ rating and a $46 price target. Analyst Gregg Moskowitz highlighted CoreWeave’s remarkable 736% revenue growth, healthy 74.24% gross margins, and strong position in compute-heavy AI tasks. However, he also pointed out that profitability remains a concern despite the company’s rapid rise.

Featured image via Shutterstock