As telehealth company Hims & Hers Health (NYSE: HIMS) navigates a turbulent short-term period following a disappointing Q2 2025 earnings report, some on Wall Street are projecting extended losses for the stock.

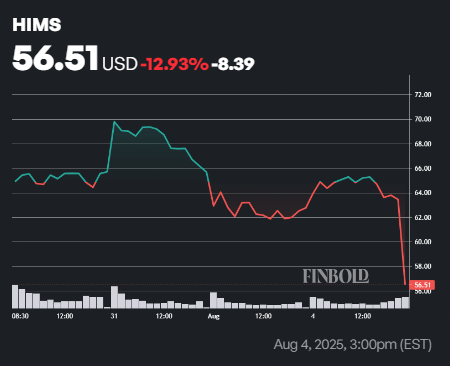

Notably, in pre-market trading on Tuesday, HIMS shares plunged 12% to $55. The stock had closed the previous session at $63.35, up 1.2%, and remains more than 150% higher year-to-date.

In the most recent quarter, Hims & Hers reported a 73% year-over-year revenue increase to $544.8 million, falling short of the expected $552 million. However, adjusted EPS beat estimates, coming in at $0.17 versus the forecasted $0.15.

Despite the strong profit figures, investors were rattled by the revenue miss and ongoing regulatory concerns surrounding the company’s compounded GLP-1 drug offerings. While the FDA has addressed supply issues, Hims continues to sell unapproved, personalized versions of popular weight-loss and diabetes medications.

Wall Street’s take on HIMS stock

Looking ahead, 10 Wall Street analysts tracked by TipRanks have issued a cautious outlook, projecting HIMS stock will average $42.33 over the next 12 months, a 33.18% decline from its current price of $63.35. The highest price target stands at $68, while the lowest is $28.

The stock holds a consensus rating of ‘Hold,’ with one analyst recommending ‘Buy,’ seven rating it as ‘Hold,’ and two issuing ‘Sell’ ratings.

Among them, Bank of America analyst Allen Lutz on August 5 maintained a ‘Sell’ rating on HIMS with a $28 price target, implying a potential 55% downside. Lutz cited weak core business growth despite strong GLP-1 revenue and the recent ZAVA acquisition. He warned of integration risks and over-reliance on compounded drug sales, along with concerns about customer acquisition and expansion into hormone therapy and the Canadian market.

Meanwhile, TD Cowen’s Jonna Kim reiterated a ‘Hold’ rating on HIMS, raising the price target to $48. Kim pointed to a combination of short-term challenges and long-term investments, citing infrastructure spending, subscriber transitions in sexual health, declining GLP-1 revenues, and regulatory risks as key headwinds.

Featured image via Shutterstock