Intel (NASDAQ: INTC) stock remains one of the emerging winners on Wall Street, though analysts are projecting a more cautious outlook for the semiconductor giant over the next 12 months.

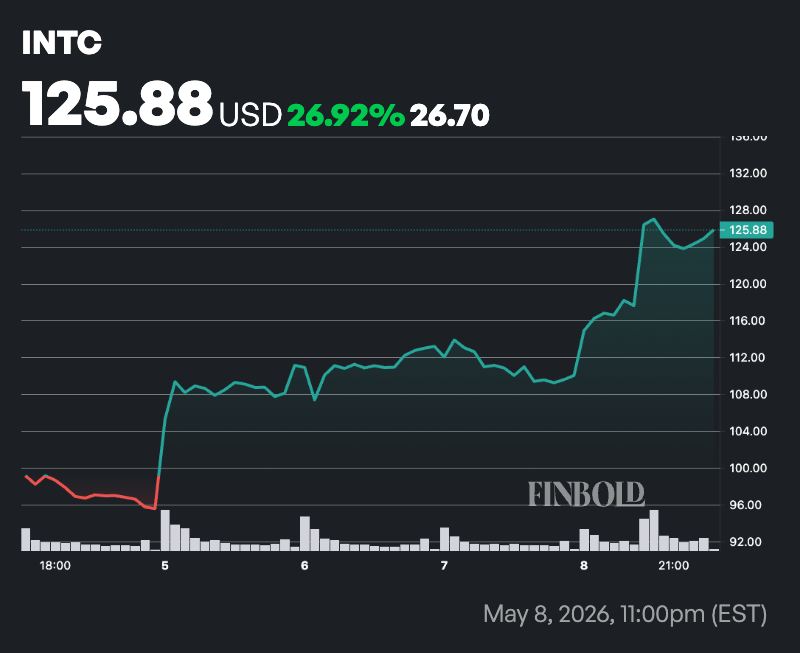

Notably, Intel’s recent momentum saw the stock hit a new record high of $130 on May 8, driven largely by impressive first-quarter earnings. Intel reported revenue of $13.6 billion, surpassing expectations, along with adjusted earnings per share of $0.29.

Another driver behind Intel’s recent momentum has been reports of preliminary agreements to manufacture chips for major clients, including potential U.S.-made Apple (NASDAQ: AAPL) devices.

The developments support broader supply chain diversification efforts backed by the CHIPS Act. CEO Lip-Bu Tan has focused on customer engagement, financial discipline, and rebuilding Intel’s manufacturing ecosystem to strengthen its chip design and foundry businesses.

Tan’s 2026 strategy centers on product execution, foundry expansion, and partnerships to expand Intel’s market opportunities.

However, analysts warn that the rally will depend on the company improving margins, production yields, and market share in an increasingly competitive industry. Investors are now watching upcoming earnings reports and potential confirmation of major manufacturing deals.

At the close of the last session, Intel shares were valued at $124.92, representing a year-to-date gain of nearly 240%.

Wall Street outlook on INTC stock

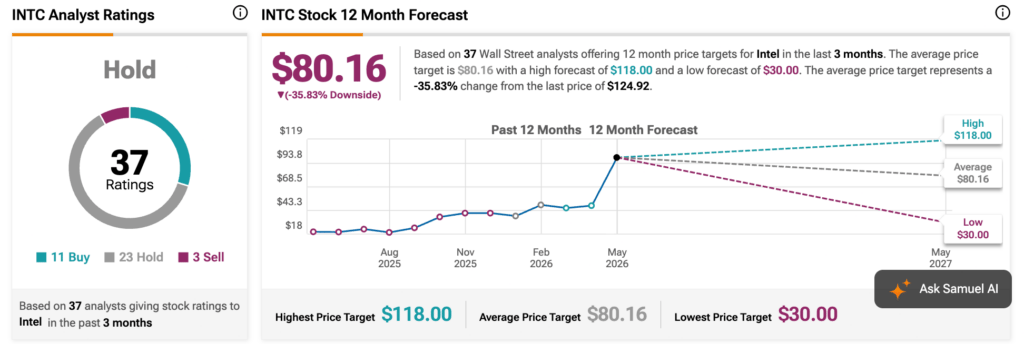

Analysts tracked by TipRanks maintain an overall consensus ‘Hold’ rating on the stock. Based on forecasts from roughly 37 to 41 Wall Street analysts, the average 12-month price target stands near $80, implying a downside of about 35% from the current valuation. Targets range from a low of $30 to a high of $118.

Among the analysts, RBC Capital Markets reiterated its ‘Sector Perform’ rating and maintained an $80 price target. The firm acknowledged strong momentum in Intel’s server CPU business, driven by rising demand tied to agentic AI and distributed inferencing, which are increasing CPU density and supporting higher average selling prices.

RBC also highlighted opportunities across Intel’s x86 portfolio, ASIC offerings, advanced packaging, and foundry services, with advanced packaging alone viewed as a multi-billion-dollar opportunity expected to ramp up in the second half of 2027. While Intel expressed confidence in its client business outlook for the second half of 2026 despite weakness in the broader PC market, RBC noted concerns about rising component costs weighing on gross margins.

Several other firms, including Roth Capital, Barclays, Morgan Stanley, and Robert W. Baird, also raised their targets following Intel’s stronger-than-expected first-quarter 2026 results.