While Meta Platforms’ (NASDAQ: META) stock has had a volatile start to 2026, Wall Street analysts believe the social media giant’s equity is likely to see notable growth over the next 12 months, with expectations for double-digit gains.

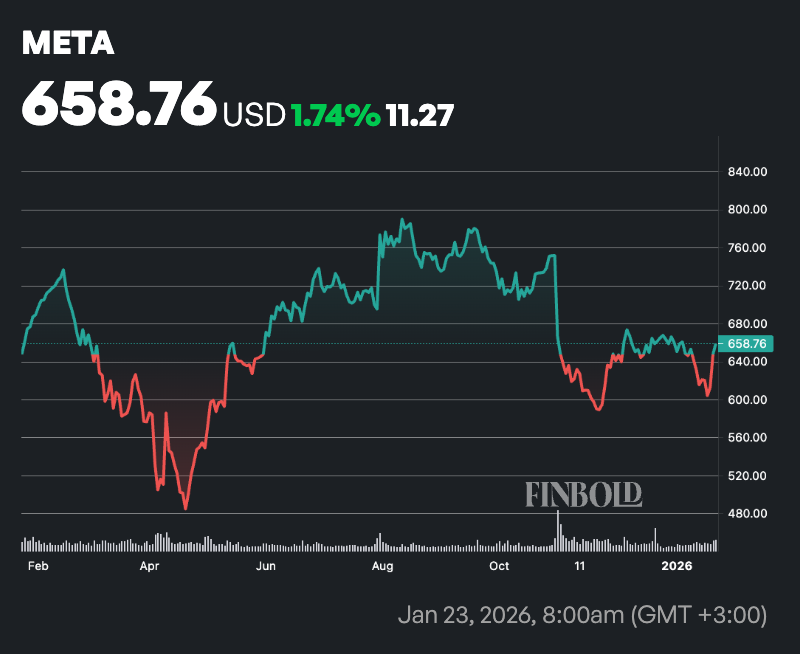

At the close of markets on January 23, META was trading at $658, having gained about 1.2% so far in 2026. Over the past year, the stock has risen a modest 3.5%.

Notably, Meta currently trades at a lower valuation than its mega-cap peers, with shares priced at roughly 20 times forward earnings. That discount could narrow in the year ahead as the company sustains growth and deepens its push into artificial intelligence (AI).

In this context, improvements in automation across Meta’s advertising business may play a key role in driving stronger financial results and boosting investor confidence.

Wall Street bullish on META share price

Overall, Meta Platforms continues to draw strong support from Wall Street analysts, with consensus forecasts pointing to meaningful upside over the next year. According to data compiled from 44 analysts on TipRanks, Meta carries a ‘Strong Buy’ rating, reflecting 37 ‘Buy’ recommendations, six ‘Holds’, and just one ‘Sell’.

The average 12-month price target for Meta stands at $820.21, implying potential upside of about 24.5%. Analysts’ targets span a wide range, with the most bullish forecast at $1,117 and the lowest at $655.15.

Analysts take on META stock price

Among the analysts, on January 23, Wells Fargo trimmed its price target on META shares to $754 from $795 while maintaining an ‘Overweight’ rating, citing higher expected operating and capital expenditures tied to updated capacity contract evaluations. Analyst Ken Gawrelski pointed to a near-term timing mismatch between Meta’s rapidly ramping AI compute investments and the pace at which new AI-driven products and use cases can be monetized, leading to upward revisions to OpEx and CapEx forecasts for 2026 through 2028.

On the same date, Stifel lowered its price target to $785 from $875 while maintaining a ‘Buy’ rating, citing increased near-term scrutiny around returns on AI investments rather than any deterioration in core fundamentals. Analyst Mark Kelley noted that advertising checks remain solid, with Instagram Reels showing particular strength, but said investor focus is shifting toward Meta’s 2026 total spending and capital expenditure outlook following the company’s Meta Compute announcement. Stifel sees room for both expense and capex estimates to rise above consensus, adjusted its Reality Labs assumptions to reflect recent headcount cuts, and reduced its valuation multiple as investors reassess AI investment efficiency, even as the stock trades near fair value and retains strong upside from current levels.

Finally, Jefferies analyst Brent Thill reiterated a ‘Buy’ rating on Meta Platforms with a $910 price target, arguing the stock has lagged peers despite intact fundamentals. Thill highlighted Meta’s underperformance versus Alphabet over the past year, leaving it the cheapest of the Magnificent Seven at about 28.5 times trailing earnings, and said investor concerns around heavy AI spending and ongoing Reality Labs losses may be overlooking strengthening benefits from Meta’s AI-driven advertising engine. He also pointed to emerging monetization opportunities across WhatsApp and Threads as potential catalysts that could help close the valuation gap.

Featured image via Shutterstock