Recent years were marked by the unusually frequent phenomenon of a company underperforming expectations only to see its stock soar – with Tesla (NASDAQ: TSLA) being the most notable example – or beating forecasts and achieving strong results only for its shares to plummet.

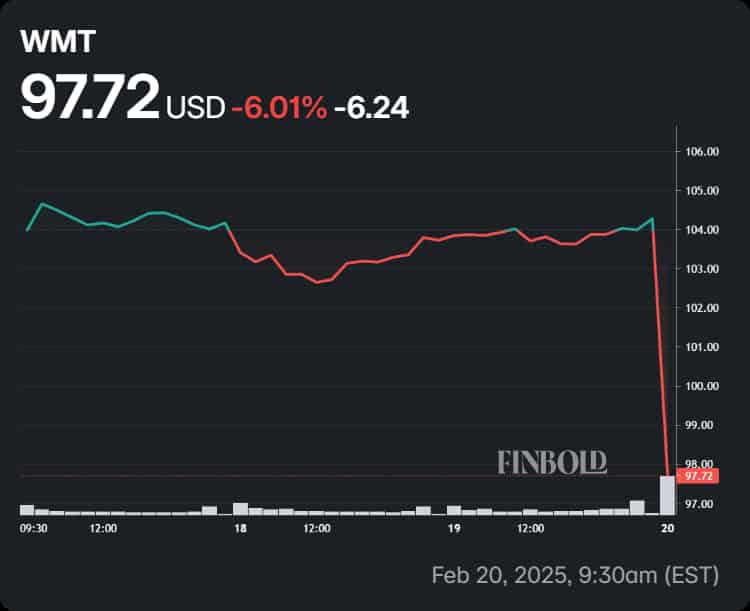

The latest firm to suffer from such a stock market beating was the retail blue-chip Walmart (NYSE: WMT). Specifically, the chain announced it achieved a revenue of $180.55 billion – above the expected $180.01 billion – and earnings per share (EPS) of $0.66 – above the forecasted $0.64- during its fiscal fourth quarter (Q4).

Despite this, WMT collapsed more than 8% during the extended session and is, at press time on February 20, 6.16% below its latest close for a total weekly drop to $97.72.

Picks for you

Why is WMT stock plunging

The plunge can be attributed to Walmart’s expectations for the future in many ways, spoiling the firm’s past success.

Specifically, the firm explained it expects growth to slow in 2025, while its CFO, John David Rainey, warned that the giant wouldn’t be ‘immune’ to the expected Canada and Mexico tariffs.

While concerns over the potential trade wars and geopolitics-induced disruptions aren’t without merit, the reaction may have already been oversized.

Are investors overreacting to Walmart’s report?

Approximately two-thirds of everything found on Walmart’s shelves is made in the U.S. in one way or another, meaning the retailer is likely to face only limited consequences from the escalating trade war.

Furthermore, the firm is in something of a sweet spot due to its position as a ‘great value’ seller, as weakness in the economy would likely drive more consumers to its store, while strength would enable it to absorb most shocks efficiently.

Walmart has also made strides in modernizing its business, as seen from the 20% annual growth of its e-commerce segment, further bolstering resilience.

Judging by the latest reassessments, major analyst firms also appear unphased by the somewhat weaker forecasts. RBC, for example, reiterated its previous ‘buy’ rating with a $109 price target, and JPMorgan (NYSE: JPM) offered the same assessment while maintaining the $112 target.

Still, vigilance remains important as there may be many underlying risks that remain unaccounted for given the current global situation featuring numerous complex oddities.

These, for example, include car parts that cross the border eight times before final assembly, the U.S. seeing one of its most important trade partners and the biggest foreign adversary in the same nation, and the E.U. propping up an authoritarian regime on its border to secure lithium supplies while ignoring environmental concerns that prevent the mining of the metal in Germany or Czechia.

Featured image via Shutterstock