A quarter of a century of increasing dividends is a hell of a way to generate some passive income. Enter Dividend Aristocrats.

These companies have kept increasing their dividends for at least 25 consecutive years, even during economic downturns, the recession, and the recent pandemic, and they show signs of strength today amidst all the trade-war uncertainties.

We analyzed five prominent names in an underrated sector to see which one stands out the most. The winner: Medtronic (NYSE: MDT).

Why the healthcare sector will dominate in 2025

Projected to reach $1.87 trillion by 2030, the U.S. healthcare sector is immensely profitable. After all, unlike some other services, healthcare usually isn’t optional, and with regulatory oversight being no great shakes, to say the least, the sector has grown quite comfortable.

As a result, pharmaceutical giants, health insurers, and medical device manufacturers seem promising.

Sure, there are some potential red flags to consider. For instance, some companies in the sector depend on foreign suppliers for raw materials and manufacturing. But, the trade war is unlikely to affect raw profit margins of companies like Eli Lilly (NYSE: LLY) and Abbott Laboratories (NYSE: ABT), given their enormous scale.

As mentioned, many people don’t really have alternatives. If they need medical care, they will look for it. We can compare this to the grocery and consumer staples sector, where demand holds steady regardless of economic cycles.

For example, Coca-Cola (NYSE: KO), another Dividend Aristocrat, appears to be doing fine. Its stock is up over 16% year-to-date (YTD) and has a 52-week high of around $74. Looking ahead, the company predicts $9.5 billion in free cash flow (FCF) for 2025, despite the talk about Donald Trump’s proposed trade policies.

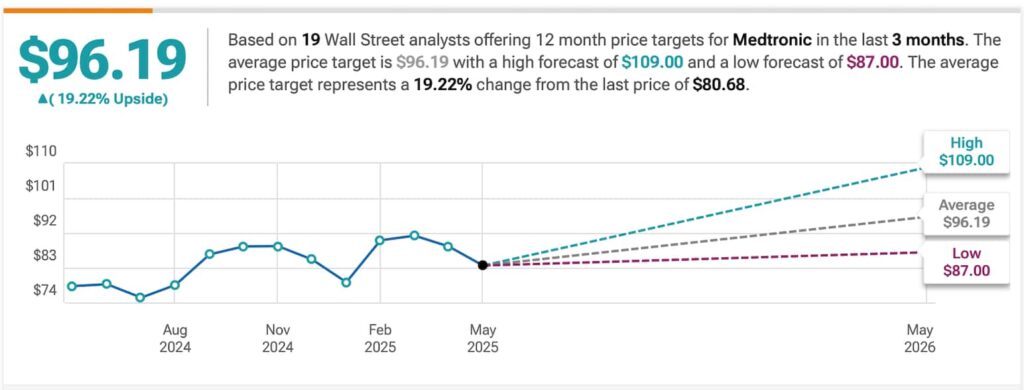

Medtronic price prediction

Medtronic’s (NYSE: MDT) portfolio spans treatments for health conditions, including cardiovascular disease, diabetes, and neurological disorders. The company operates in more than 150 countries and has a market cap of $103.48 billion.

MDT stock has fluctuated within a 52-week range of $75.96–$96.25, but analysts see a potential upside of 18.79% and project a target price of >$109 in the next 12 months. Its forward price-earnings ratio (PE) of 14.67 also suggests a reasonable valuation in the sector and might therefore be a solid entry point if you’re on a budget.

As for the dividends, Medtronic boasts a dividend yield of 3.52% and a payout ratio of 76.98%, which suggests solid long-term reinvestment potential.

Abbott Laboratories (NYSE: ABT) is a comparable Dividend Aristocrat. The company stands out as a leading healthcare provider in more than 160 countries and has raised its dividend for no less than 53 consecutive years.

As of now, it offers an annual dividend of $2.36 per share, translating to a dividend yield of approximately 1.80%. Projections also appear bullish, as Abbott shares are up 15.74% YTD (more than decent compared to the S&P 500, which is down -1.12%).

Promising but potentially riskier buys

UnitedHealth Group (NYSE: UNH), the largest health insurance provider in the U.S. and a Dividend Aristocrat, has had it rough recently, being under pressure for math slips that resulted in higher-than-expected medical costs. As a consequence, the management pulled down the earnings per share forecast entirely.

However, the company’s dividend remains unaffected, having climbed 14.60% per year over the past five years with a current yield of 2.8%. Likewise, some will consider the stock undervalued, trading at just 12.4x trailing earnings.

AbbVie (NYSE: ABBV), a $323 billion biopharma giant, is in a similar spot. While the company remains on solid footing, boasting a gross profit margin just north of 70%, it still faces some hurdles. For example, its aesthetics division remains under pressure due to broader economic challenges and heightened competition. Moreover, changes to prescription drug pricing rules could affect profitability.

Becton Dickinson (NYSE: BDX) has also seen its stock outlook downgraded by analysts amid growing concerns over its near-term performance and strategic direction. The stock is down -24.33% YTD and is now seen as undervalued. Still, earnings per share slightly beat expectations at $3.35 (versus $3.28), and the company is planning a spin-off of its biosciences unit that may reshape its financial future.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

Featured image via Shutterstock