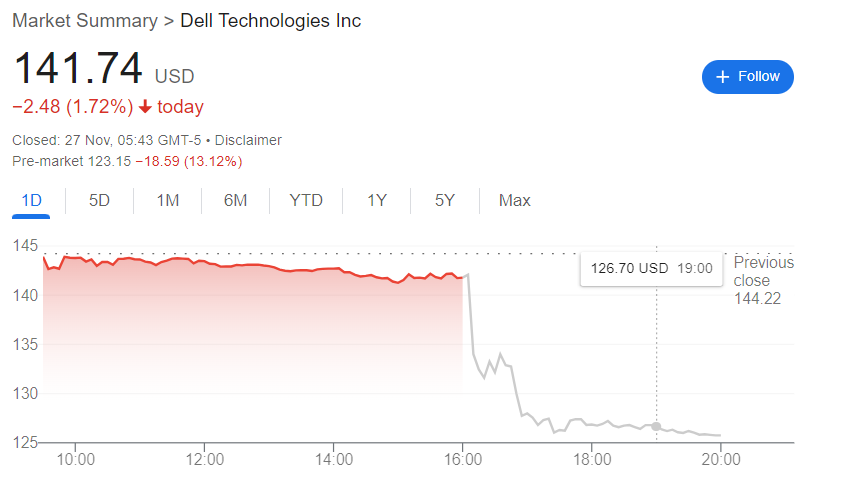

Dell’s (NYSE: DELL) share price is spiraling downward as investors digest the company’s third-quarter earnings and future forecasts.

At the close of the latest trading session, Dell was trading at $141.74, ending the day down 1.7%. The weakness extended into pre-market trading on November 27, where the stock has plunged over 13% to $123. Despite this dip, Dell remains green for 2024, gaining almost 90% year-to-date.

Why DELL share price is plunging

This decline comes even as the company reported better-than-expected Q3 results and a bullish outlook regarding Dell’s venture into artificial intelligence (AI). The technology giant posted earnings per share of $2.15, surpassing the expected $2.06. However, revenue came in at $24.4 billion, slightly below the forecast of $24.67 billion.

Picks for you

Dell also recorded a double-digit surge in demand for traditional servers, driven by increased orders for AI servers. These CPU-based servers, are less power-intensive and help optimize data center resources for AI investments.

However, the outlook for the fourth quarter has spooked investors. Specifically, during the earnings call, Dell projected revenue between $24 billion and $25 billion for the final three months of 2024. This forecast fell short of the estimated $25.57 billion.

The stock is also being weighed down by weaker demand for Dell’s traditional PCs at a time it anticipates lower server sales from enterprise customers who are delaying purchases of new devices powered by Nvidia’s (NASDAQ: NVDA) next-generation Blackwell chips.

Wall Street’s DELL stock outlook

In the wake of these results, Bernstein analyst Toni Sacconaghi maintained an ‘Outperform’ rating on Dell with a $140 price target but highlighted mixed signals in the outlook.

According to Sacconaghi, while the AI business shows promise, delays in PC upgrades and AI server shipments have impacted guidance. Concerns persist about the company’s reliance on Tier 2 cloud providers and potential challenges in scaling AI infrastructure.

Sacconaghi noted that Dell’s expanding AI pipeline supports its long-term growth potential despite these issues.

“Dell’s Q3 results were somewhat disappointing. Revenues were slightly below consensus, and the company guided for Q4 revenues that were nearly $1B below Street expectations. <…> . Dell’s AI pipeline appears to have improved to $15-20 billion,” Sacconaghi said.

Goldman Sachs also maintained a ‘Buy’ rating on Dell stock and increased its price target to $165 from $155. Despite the gloomy fourth-quarter forecast, the firm cited the company’s strong third-quarter results as a positive factor.

Amid this outlook, investors are monitoring how Dell establishes itself in AI, anticipating it will catch up to dominant players such as Nvidia. To this end, Dell has been reallocating resources to AI, including initiatives like shedding parts of its global workforce, with results expected to be visible in the coming quarters.

Featured image via Shutterstock