Lucid Motors (NASDAQ: LCID) has had a bumpy ride ever since its initial public offering (IPO) back in mid-2021.

The electric vehicle (EV) business set ambitious production and delivery standards for itself — which it subsequently failed to meet. As a result, Lucid stock has been on a steady downward trajectory over the past three years.

The situation is also exacerbated by the presence of what can only be described as a double-edged sword. While Lucid has secured the seemingly endless backing of Saudi Arabia’s Public Investment Trust, which is the company’s largest stakeholder, this has also led to repeated concerns surrounding share dilution.

With all that being said, there are several significant silver linings in otherwise dark skies. On January 6, the carmaker reported its Q4 production and delivery results. This marked the first instance in which the company outpaced its own guidance since 2022. Earlier still, on November 7, 2024, the company’s Q3 2024 earnings call saw both revenues and earnings per share (EPS) come in above analyst estimates.

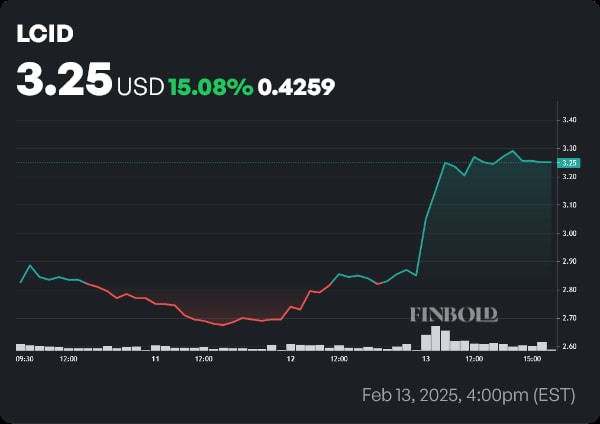

By press time on February 14, Lucid stock was trading at a price of $3.25. The price of LCID shares saw a 14.03% move to the upside on February 13, after an eminent Wall Street firm gave the luxury EV company a vote of confidence.

Benchmark bullish on Lucid stock ahead of earnings

On February 12, Benchmark analyst Mickey Legg initiated coverage of Lucid stock with a ‘Buy’ rating. The researcher set a $5 price target — if met, it would equate to a 53.84% surge from current prices.

In a note shared with investors, Legg cited an optimistic outlook regarding domestic electric vehicle production, which he expects will improve in 2025 and further accelerate in 2026 and 2027, on account of lower prices and improved infrastructure. The Benchmark researcher believes that Lucid stock can benefit from the opportunity based on its technology, strong balance sheet, access to capital, and highly integrated manufacturing capabilities.

As bullish as that sounds and as optimistically as the markets have reacted to the coverage, context is important. Since the start of the year, Lucid stock has only received two updated outlooks — the other, from Cantor Fitzgerald, is a ‘Neutral’ rating with a $3 price target. Wall Street is far from a consensus when it comes to LCID shares.

Investors should always be mindful of countertheses. Amidst slowing demand, consumer preferences in the EV market are increasingly trending toward affordability. The company’s current lineup of vehicles is on the expensive side. While Lucid is planning to expand its offerings with several new, more affordable models, they’re scheduled to arrive in 2026 — by which time, we might be looking at a ‘too little, too late’ situation.

Featured image via Shutterstock