Nvidia’s (NASDAQ: NVDA) stock price is showing signs of entering what analysts describe as a new “supercycle,” amid growing confidence in the technology company’s dominance in artificial intelligence.

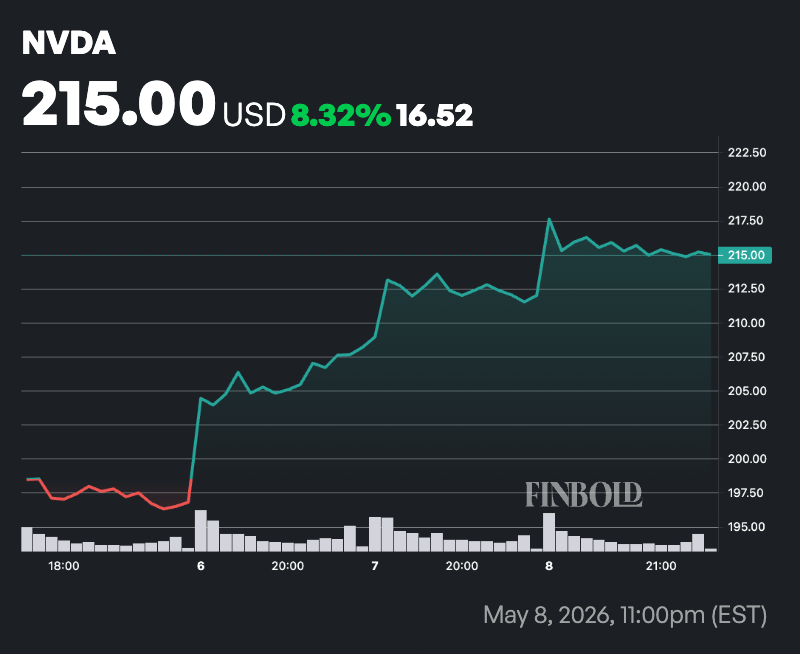

Notably, Nvidia has been on an upward tear, culminating in a May 8 intraday record high of $217 before closing the day at $215, up almost 2% on the session.

Nvidia stock price outlook

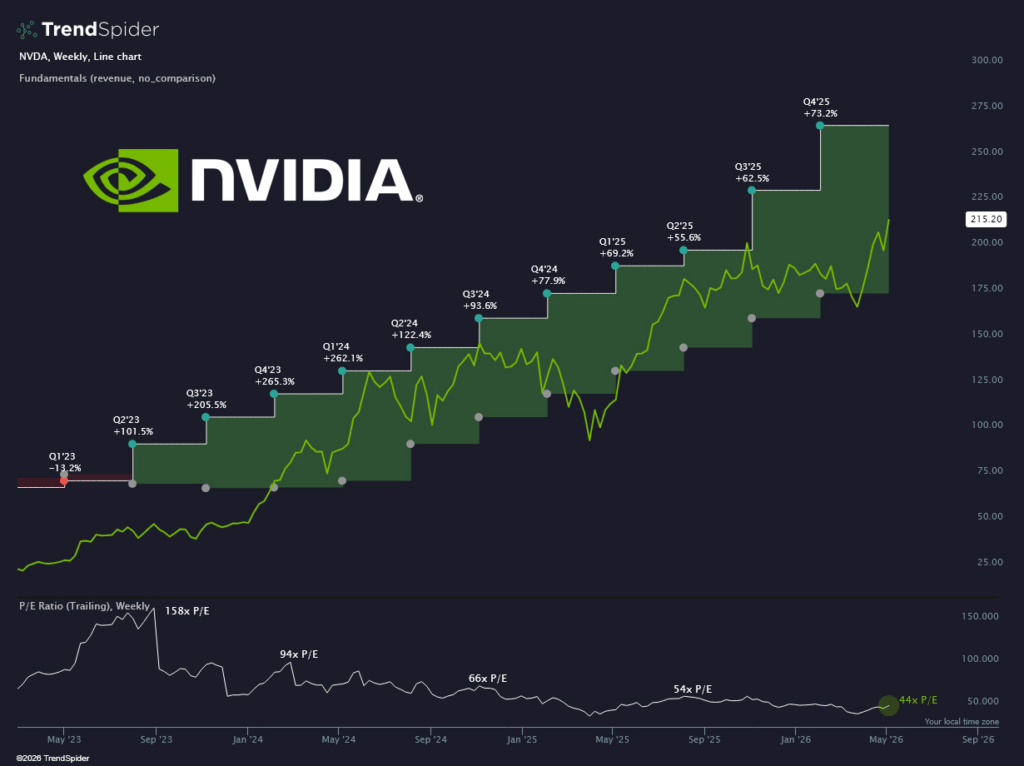

Meanwhile, the bullish outlook stems from Nvidia’s long-term rally, tracking a series of accelerating quarterly revenue increases, reinforcing its position at the center of the global AI infrastructure boom, according to insights shared by charting platform TrendSpider in an X post on May 10.

The analysis showed Nvidia’s growth cycle accelerated in fiscal Q2 2023, when revenue growth reached 101.5% year-over-year, before climbing to 205.5% in Q3 2023, 265.3% in Q4 2023, and peaking at 262.1% in Q1 2024.

Although the pace of expansion has gradually moderated from those extraordinary triple-digit levels, Nvidia has continued to report exceptionally strong growth rates throughout 2024 and into 2025. Revenue growth remained at 122.4% in Q2 2024, 93.6% in Q3 2024, 77.9% in Q4 2024, and 69.2% in Q1 2025.

The trend has remained resilient in subsequent quarters, with a revenue growth of 55.6% in Q2 2025, 62.5% in Q3 2025, and 73.2% in Q4 2025. The figures suggest demand for Nvidia’s AI accelerators and data center chips remains exceptionally strong despite the company’s massive scale.

At the same time, Nvidia’s valuation metrics suggest investors are growing more comfortable with its long-term growth outlook.

Although the company’s trailing price-to-earnings ratio once surged to 158x during the early AI rally, it has since compressed to around 44x even as the stock trades near record highs above $215. The combination of rapidly expanding earnings and a lower valuation multiple is widely viewed as a bullish sign.

NVDA stock price fundamentals

This outlook comes as Nvidia prepares to report its fiscal first-quarter 2027 results after the market closes on May 20.

Notably, the semiconductor giant enters earnings on a strong footing after guiding for roughly $78 billion in quarterly revenue, driven by continued surging demand for AI infrastructure and its Data Center business.

Analysts expect earnings per share of about $1.76 to $1.77, with many anticipating another beat-and-raise quarter given Nvidia’s recent track record.

Investor optimism remains supported by the continued ramp-up of Nvidia’s Blackwell platform and heavy hyperscaler spending on AI infrastructure.

CEO Jensen Huang has also pointed to accelerating AI adoption trends, while future platforms such as Rubin are reinforcing long-term growth expectations.

At the same time, risks remain, including U.S. export restrictions on advanced AI chips to China, valuation concerns, rising competition, and broader macroeconomic uncertainty that could affect near-term stock performance.