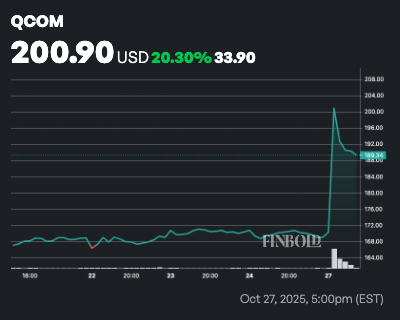

Qualcomm’s (NASDAQ: QCOM) stock is skyrocketing in double figures, marking one of its strongest single-day performances this year.

The stock has surged over 15% to $195 by press time, and year-to-date, it has rallied nearly 25%.

Why QCOM stock is spiking

The rally follows the chipmaker’s announcement of a major push into the data center space, unveiling two new AI chips designed for enterprise customers.

In this line, the AI200 and AI250 chips are specifically built to address memory-intensive AI applications. These products are part of Qualcomm’s broader strategy to diversify beyond smartphone chips and tap into the expanding AI infrastructure market.

The AI200 is slated for release in 2026, with the AI250 following in 2027. While the chips won’t be available immediately, investors have reacted positively to the company’s strategic positioning as it seeks to take on dominant players such as Nvidia (NASDAQ: NVDA).

Overall, Qualcomm is shifting its focus from mobile devices to capitalize on the growing demand for AI hardware. As global investments in AI infrastructure rise, the firm aims to strengthen its position with moves like its $2.4 billion acquisition of Alphawave in June and the launch of custom processors based on Nvidia technology.

In conjunction with the chip announcement, Qualcomm also released accelerator cards and server racks, completing its data center hardware portfolio. The new AI chips leverage the same Hexagon neural processing units (NPUs) used in Qualcomm’s smartphone chips, enabling seamless integration with AI accelerators in data centers.

Wall Street cautious on QCOM stock

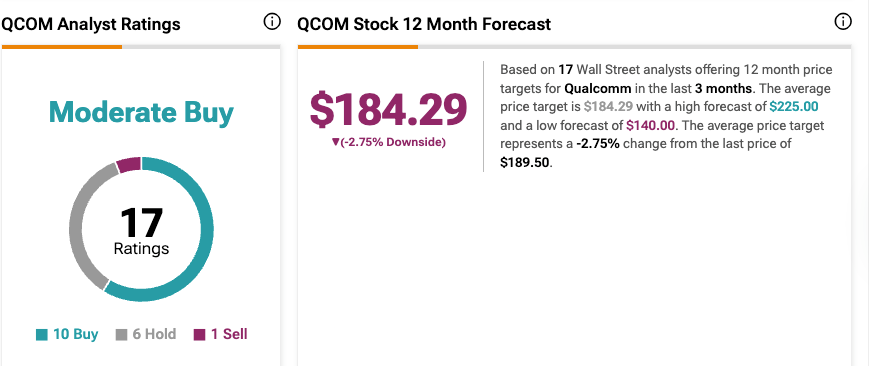

Meanwhile, analysts over at Wall Street are projecting the stock may face a short-term correction in the next 12 months. Consensus from 17 analysts tracked by TipRanks shows a ‘Moderate Buy’ rating for QCOM.

The experts have an average price target of $184.29, with a high forecast of $225 and a low of $140, indicating a slight downside of about 2% from the current price level.

Indeed, the new chip announcement is facing skepticism, with Bank of America (BofA) raising concerns over limited customer disclosure and revenue projections.

BofA views the chips as lower-end models without HBM and shipping in a year, with only a Middle East customer disclosed. The firm estimates $1 to $2 billion in potential revenue.

Featured image via Shutterstock