While deficit hawking has somewhat fallen out of fashion, various forms of debt remain a major concern for economists, politicians, and the public.

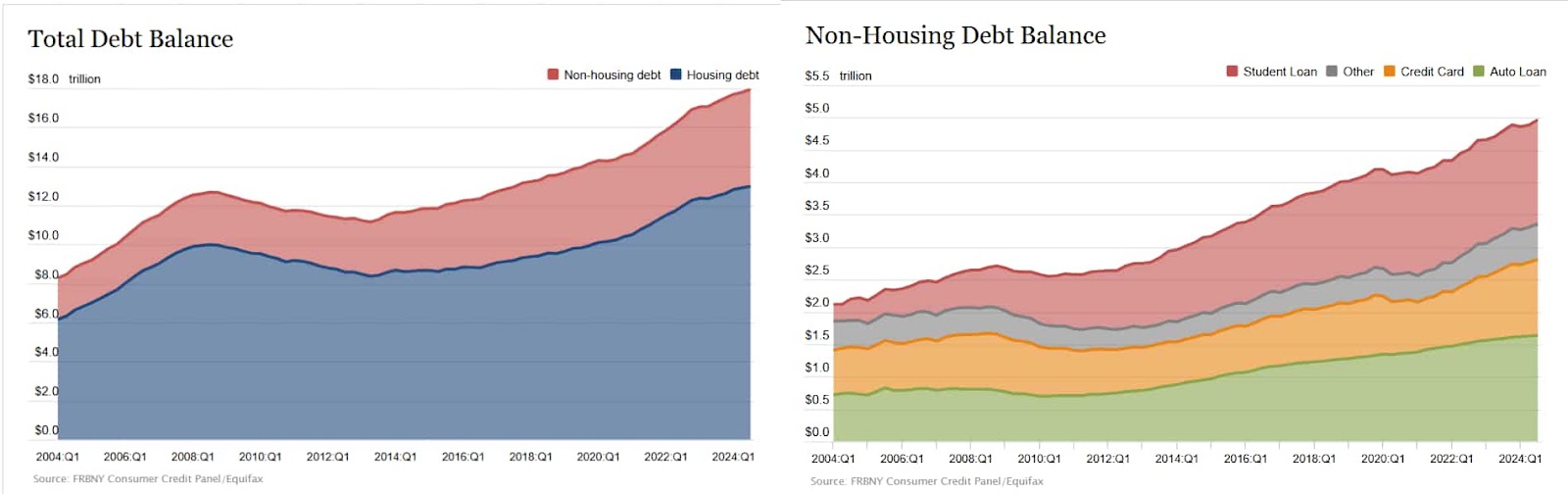

Much has been said about America’s ballooning public debt, but equally – if not more – concerning is the growth of household debt within the nation.

Specifically, the figure rocketed to a record of $17.9 trillion during the previous quarter. The New York Fed found that student loans, credit card balances, and car loans – the three biggest individual elements not part of housing debt – surged to $1.61 trillion, $1.17 trillion, and $1.64 trillion.

Picks for you

Why the rise in total household debt might not be alarming

Still, the bank’s economics research adviser, Donghoon Lee, opined that the rise is not as concerning as it appears at face value since income growth has outpaced the rise in the household burden.

The adviser, however, pointed toward another statistic – the rise in delinquencies – as a sign that many Americans are under significant stress.

Indeed, as far back as May, 8.9% of all credit card balances fell into some form of delinquency, per an NPR report. In September, it became known that U.S. auto loan defaults surged to 15-year highs.

All forms of debt appear to be galloping vs. U.S. GDP

In total, the new record figure of $17.9 trillion means that the U.S. household debt is now at least 64% as large as the nation’s Gross Domestic Product (GDP) is expected to be at the end of 2024.

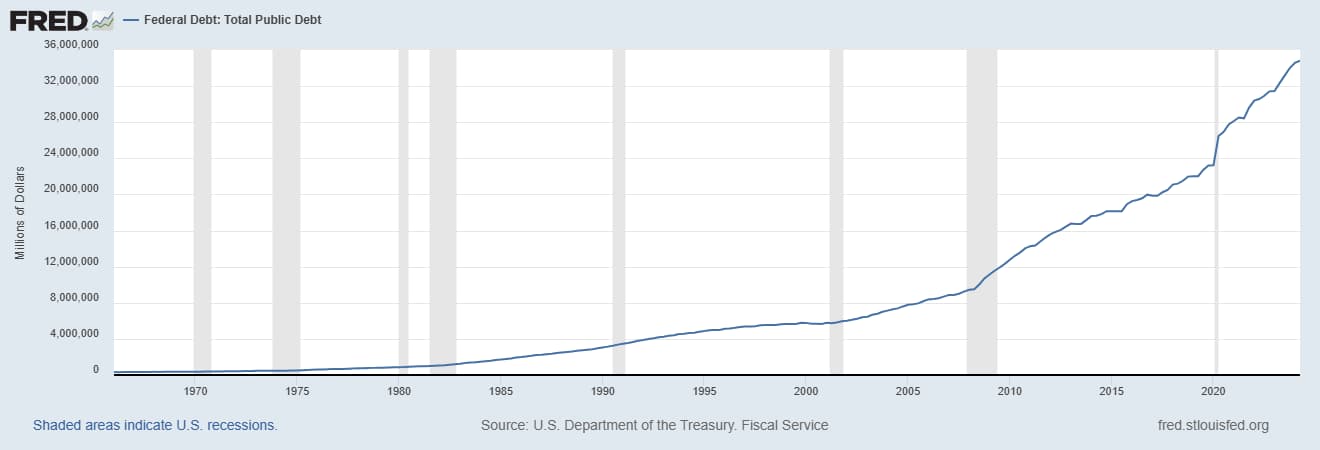

Perhaps more concerning is that both the number and the ratio are dwarfed by the national debt, which is approximately $7 trillion bigger than the GDP forecast.

Both numbers are, however, overshadowed by another statistic: CEIC data lists the ratio of all debt in the U.S. compared to GDP as 720.2%. Unlike the National and household debt, however, this metric is showing a steady decrease in recent years and constitutes a 7% drop from the previous quarter.

Total debt to total income ratio shows improvement from pre-pandemic levels

Finally, though most forms of debt will likely come under increased scrutiny under the inbound administration – and it is likely there will be an increase in deficit hawking due to the creation of the apparently toothless Department of Government Efficiency (DOGE), helmed by Elon Musk and Vivek Ramaswamy – it is noteworthy that there is silver lining even in the most recent data.

Specifically, as Donghoon Lee explained, income has risen more than household debt, so the ratio of the burden compared to total income has fallen from 86% in 2019 to 82% in 2024.

Featured image via Shutterstock