With the stock market facing persistent macroeconomic challenges and the looming possibility of a US recession, investors find themselves in a precarious position, grappling with volatility and uncertainty.

In light of these concerns, Finbold has conducted an in-depth analysis of the market, pinpointing five stocks that are currently encountering headwinds and that traders should steer clear of in the near term.

Carnival Corp. (NYSE: CCL)

British-American cruise operator Carnival Corp. (NYSE: CCL) delivered a remarkable performance in the stock market this year, rising more than 140% year-to-date.

However, while some may assume that CCL has completely overcome its previous hurdles at first, this may not be the case.

Notably, Carnival has a long road to entirely recover from the challenges it encountered during the coronavirus pandemic, which continue to weigh on its balance sheet.

The company still has over $30 billion of dollars in long-term debt, while its liquidity ratios remain deeply suppressed.

The company is expected to report a loss per share of 14 cents this year, followed by a rebound in fiscal 2024. That said, Finbold advises investors to keep away from CCL in the short run.

CCL price analysis

At the time of writing, shares of Carnival Corp. were standing at $19.21, up 1.3% in the past 24 hours.

The company gained more than 20% over the past week, and over 50% on the month.

Walgreens Boots Alliance (NASDAQ: WBA)

Last week, Walgreens Boots Alliance (NASDAQ: WBA) warned investors that tepid consumer spending and its bigger-than-expected drop in coronavirus product sales would likely persist in 2024.

The executives said the company has been “impacted by the rapid softening of the macro environment and a more cautious and value-driven consumer,” sending its shares to an 11-year low of $28.64.

Due to these headwinds, Walgreens trimmed its 2023 earnings forecast to $4.00 – $4.05, from the earlier range of $4.45 – $4.65.

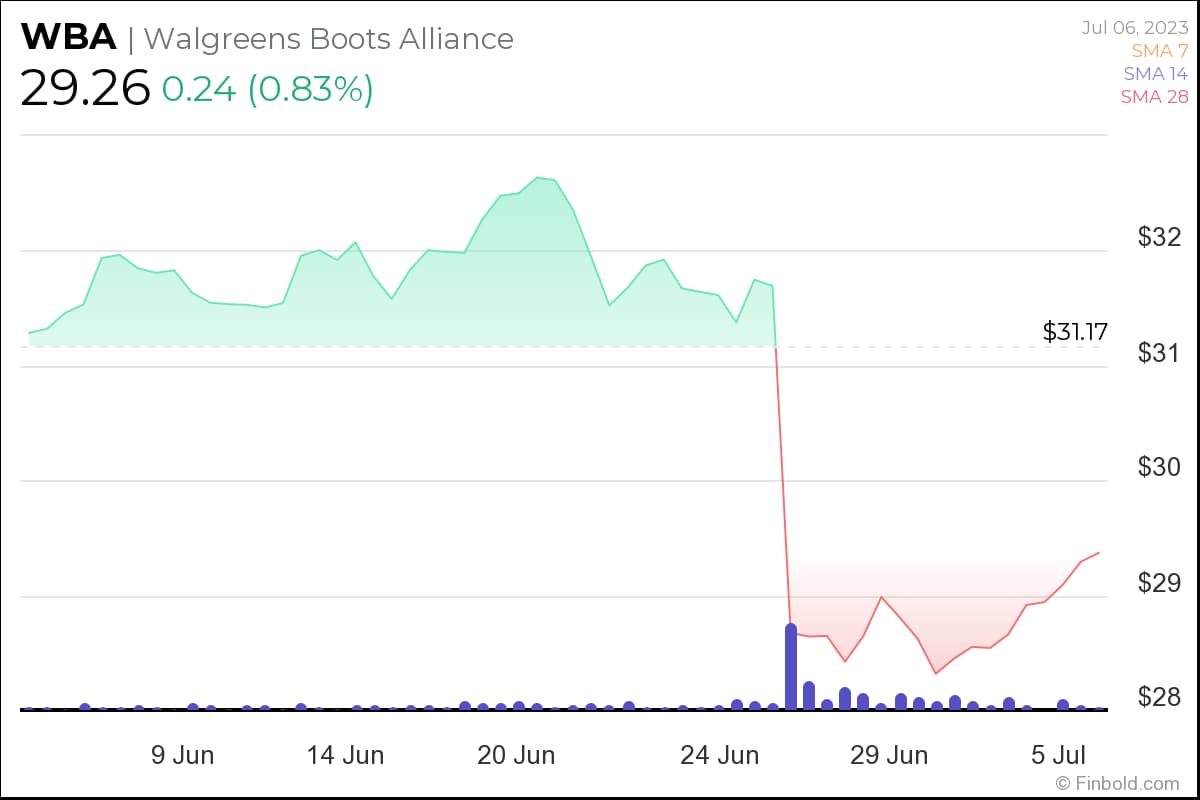

WBA stock price analysis

At the time of publication, Walgreens’ stock stood at $29.26, up around 0.8% in the past 24 hours.

In the last 30 days, WBA’s share price lost over 7% of its value, with the most evident drop seen on June 27, when the company issued the warning.

Year-to-date, the company’s share price is in the red by more than 21%.

Squarespace (NYSE: SQSP)

Squarespace (NYSE: SQSP), a website hosting and building platform, has been recently deemed as one of the most overvalued stocks by Morningstar analysts.

Notably, the financial services firm rated SQSP as a 2-star stock, primarily because it was trading at a significant premium to Morningstar’s fair value estimate.

While the company has some “very good growth dynamics,” Morningstar experts believe that its figure growth will be limited, mainly due to intensifying competition.

SQSP stock price analysis

At press time, shares of Squarespace stood at $31.46, down 1.7% on the day.

The stock rose more than 9% over the past week and is up over 41% year-to-date, adding more than $1.4 billion in market cap during that period.

Levi Strauss (NYSE: LEVI)

Levi Strauss (NYSE: LEVI), the renowned denim jeans pioneer, is set to release its fiscal second-quarter numbers on Thursday, with many expecting a challenging report.

In particular, analysts anticipate a 9% decline in revenue and a staggering 90% drop in net income per share.

While Levi Strauss has previously surpassed bottom-line expectations, Citi strategists recently lowered its price target on the company’s shares, expressing caution about potential risks in the second half of the year.

With the first week of July being relatively quiet for earnings announcements and a trading holiday on Tuesday, investors may have reasons to exercise caution when considering Levi Strauss as an investment option.

LEVI stock price analysis

Shares of Levi Strauss fell nearly 2% on Wednesday and were trading at $14.12 at press time.

The stock secured slight gains over the past month of around 4.1%, although it remains down 10% since the beginning of 2023.

Joby Aviation (NYSE: JOBY)

Joby Aviation (NYSE: JOBY), a growing air taxi service provider, experienced a remarkable share price surge in recent weeks after a series of positive developments within the company.

One of those developments was clearing a regulatory hurdle for airworthiness and also attracted a noteworthy international investor.

Although Joby Aviation’s long-term prospects appear promising, it is still a pre-revenue company with a market capitalization of nearly $7 billion.

Joby is expected to generate revenue next year but may take several years before the company becomes profitable. Taking this into consideration, as well as the limited market size and competition, it is advisable to keep an eye on market dips rather than join the recent rally in JOBY shares.

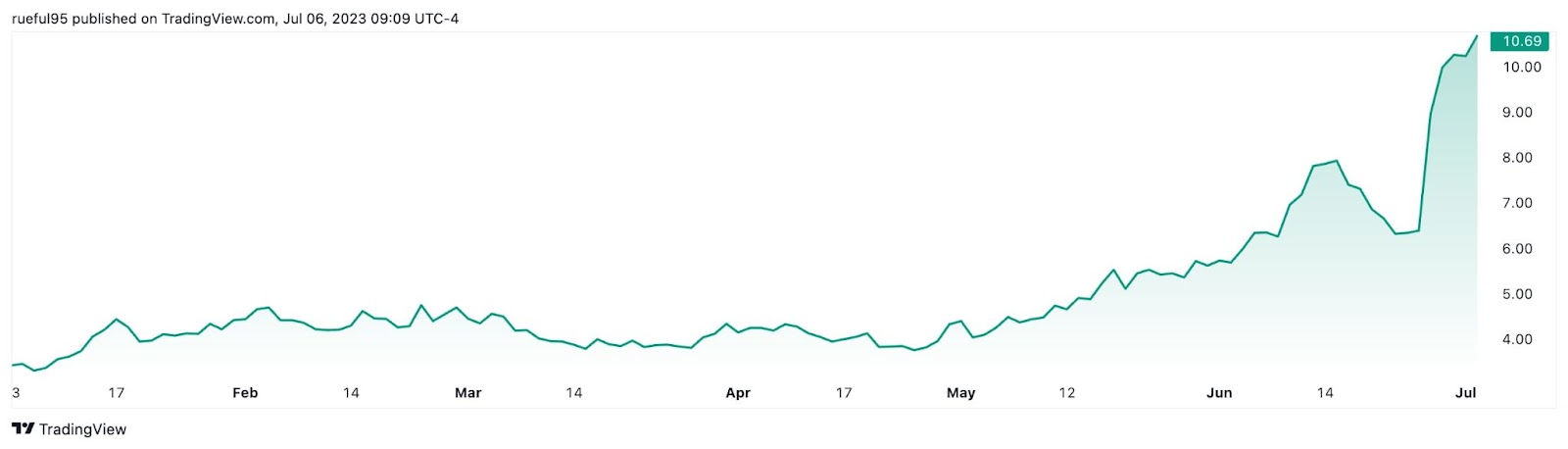

JOBY stock price analysis

At publication time, Joby’s stock was trading at $10.69, up 4.5% on the day.

The stock rose more than 52% and 86% in the past week and month, respectively.

Year-to-date, JOBY gained a mouthwatering 212.5%, propelling its market value by around $4.5 billion.

Final Words

In an ever-changing market landscape, Finbold’s analysis highlights five stocks that investors should avoid trading next week. Even though some of the aforementioned stocks have been on a sharp rally this year, it is advisable to steer clear for the time being.

Buy stocks now with Interactive Brokers – the most advanced investment platform

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.