This guide will look at the causes and predictors of recessions. It will also briefly list the most significant recessions in recent U.S. history, as well as the best investing strategies during times of economic downfall.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

Summary

– Recession definition: prolonged economic decline (typically 2+ quarters);

– Marked by falling GDP, income, jobs, production, and spending;

– Part of the business cycle (peak → contraction → trough);

– Causes: financial crises, inflation, external shocks, low confidence;

– Signals: rising unemployment, falling demand, inverted yield curve;

– Govt. response: lower interest rates, stimulus, increased spending;

– Examples: Great Depression, 2008 crisis, 2020 Covid crash;

– Strategies: invest in defensive sectors, dividend stocks, diversify.

Recession definition

They are the period between the peak of economic activity and its subsequent trough (lowest point). As a result, recessions generally produce declines in economic output, consumer demand, and employment.

In a 1974 New York Times article, economist Julius Shiskin presented a few benchmark definitions of what constitutes a recession, the most popular of which became the decline in real GDP (a measure of a country’s gross domestic product adjusted for inflation) for two consecutive quarters.

In the United States, The National Bureau of Economic Research (NBER) is commonly recognized as the authority for dating U.S. recessions. The NBER defines an economic recession as:

“A significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

Recessions and the business cycle

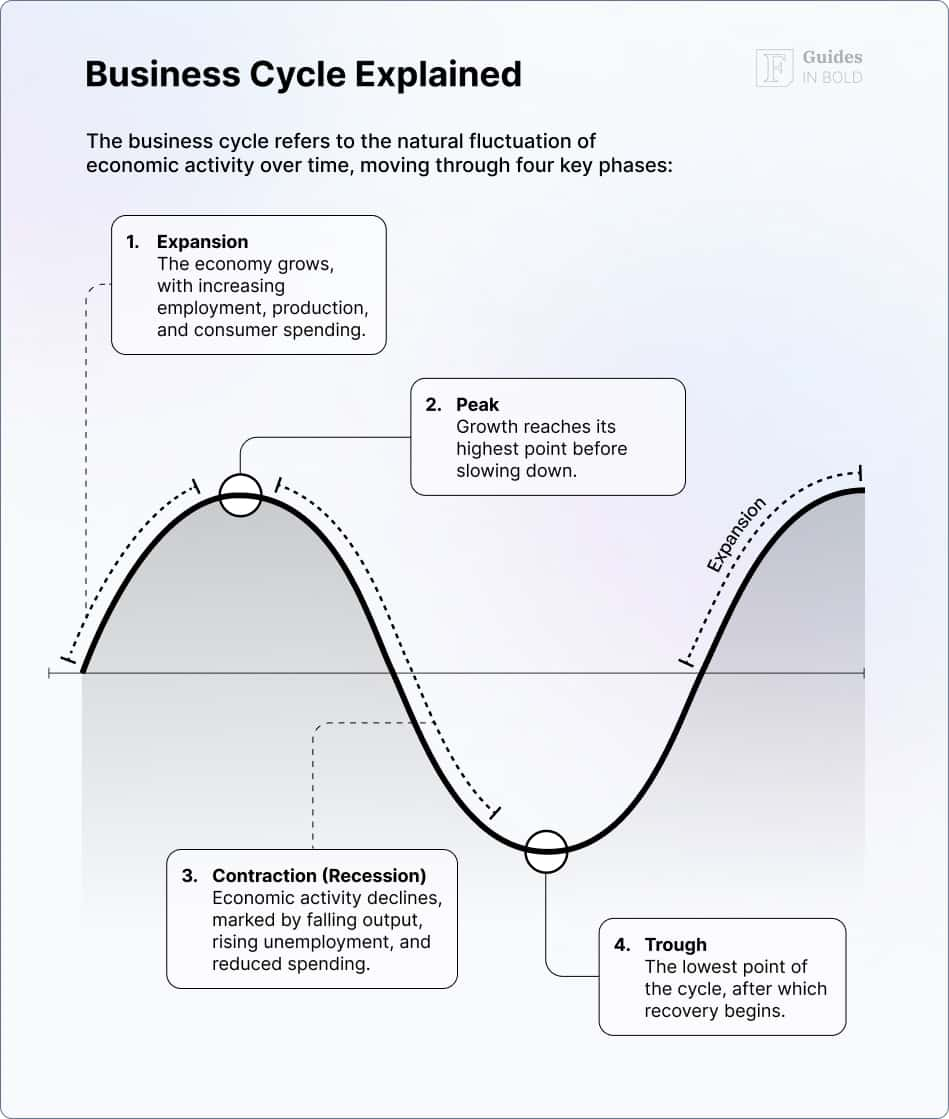

To fully understand the economic factors that constitute a recession, it’s crucial to recognize the relationship between recessions and the business cycle. A business cycle is comprised of the natural upward and downward fluctuations in the key indicators of economic activity: production, employment, income, and sales.

A business cycle contains one expansion and contraction in sequence. One complete business cycle has four distinct phases: expansion, peak, contraction (recession), and trough. Recessions typically begin at the business cycle’s peak (the end of an expansion) and end at the cycle’s trough (the beginning of the next boom).

Since the Industrial Revolution, growth has been the norm in capitalistic economies, with contractions being an inevitable element of this system. Ultimately, recessions are the relatively short corrective phase of the business cycle, adjusting the economic imbalances induced by the initial expansion and clearing the way for growth to resume.

Business cycles occur at unpredictable intervals, are irregular in length, and their severity is contingent on the economic variables of the time.

According to U.S. government research, the economy, particularly since World War II, has undergone longer periods of expansion than contraction. For instance, between 1945 and 2019, the average expansion lasted about 65 months, and the average recession lasted about 11 months. However, the 2009-2020 expansion was the longest at 128 months.

What happens in a recession?

Recessions are caused by a loss of consumer and business confidence. As consumers and companies become anxious about the economy, they hold onto their money and cut spending. The decreased demand forces businesses to reallocate resources and scale production, resulting in layoffs and fewer jobs.

Recommended video: What causes an economic recession? – Richard Coffin

The interconnected combination of economic factors includes:

Economic shocks

Economic shocks are unpredictable events that cause sweeping economic disruption. This is because markets and industries are interconnected in the economy, so blows to either supply or demand in any sector can have a substantial macroeconomic impact. In particular, shocks to vital industries such as energy or transportation typically bring about a slowdown of economic activity with ripple effects on consumers, workers, as well as the stock market.

For instance, a sudden, sustained escalation in oil prices due to a geopolitical crisis like Russia’s invasion of Ukraine might raise costs across the economy. Additionally, the outbreak of COVID-19 in 2020 and the public health restrictions imposed to contain its spread is another example of an economic shock that can trigger a recession.

Loss of consumer confidence

Loss of confidence in the economy prompts consumers to slow spending and save whatever they can. And because almost 70% of U.S. GDP depends on consumer spending, the entire economy can drastically slow. As a result, businesses are forced to reallocate resources, laying off workers as the downturn magnifies. Then, as retail sales slow, the manufacturing sector suffers, intensifying unemployment even further.

Inflation

Inflation is the rate at which the general price level of goods and services in an economy increases over time. In other words, inflation means that the purchasing power of money is decreasing as prices for goods and services rise.

Inflation can be measured by calculating the percentage change in the price level of a basket of goods and services over some time, such as a year or a quarter. This basket of goods and services typically represents the average spending patterns of households in an economy. Inflation can have both positive and negative effects on an economy.

As central banks raise interest rates (slowing demand and effectively the economy) to curb inflation, it becomes more expensive for consumers to borrow money. As a result, consumers are less likely to spend, particularly on major purchases like houses or cars. Furthermore, high borrowing costs will also force companies to reduce their spending and growth plans.

For example, the Federal Reserve under Paul Volcker raised interest rates above 19% to battle inflation of the late 1970s, which contributed to the 1980 recession (the last double-dip recession).

Deflation

The opposite of inflation is deflation which occurs when the value of goods and services across the economy falls. The shift in supply and demand brings down prices as sellers try to attract buyers, encouraging consumers to wait even longer for those prices to drop, further reducing demand. Lower consumer spending culminates in a downward spiral, the reduced activity inhibiting economic growth and contributing to growing unemployment.

Financial bubbles

Asset bubbles occur when the prices of investments such as tech stocks during the dot-com boom or housing before the financial crisis of 2008 skyrocket, far beyond their underlying fundamentals (intrinsic valuation).

These high prices are backed by artificially inflated demand and consumer creed and funded by increased credit supply (e.g., low borrowing costs). Their unsustainable nature culminates in the inevitable burst of the bubble, wiping out investor wealth and causing businesses to fail, setting the stage for a recession.

Recession predictors

While there is no guaranteed method of forecasting a recession, an inverted yield curve has demonstrated in the past to be a reliable metric of economic downturns, preceding each of the ten U.S. recessions since 1955.

An inverted yield curve indicates that long-term interest rates for bonds are less than short-term interest rates. In an inverted yield curve, the return decreases the further away the maturity date is.

Recommended video: The chart that predicts recessions

Recessions often get reduced to a simple definition of two consecutive quarters of GDP decline. While a good rule of thumb, it hardly captures the actual scope of a recession. In reality, the NBER, which declares when the U.S. has entered a recession, tracks the change in business cycles by evaluating various indicators.

Apart from an inverted yield curve, these economic indicators can also forecast trouble on the horizon:

- A decline in real GDP;

- A decrease in real income;

- Increase in unemployment;

- Stagnation of industrial production and retail sales;

- Sudden stock market decline;

- A reduction in consumer spending.

Fluctuations in just one of these factors are insufficient for the NBER to sound the alarm, which is why the two-quarter system is inadequate at predicting a recession accurately. However, these factors are indeed intertwined. For example, if a rising percentage of the workforce finds themselves without jobs, consumer spending will decrease even further.

How can government solve a recession?

Since the Great Depression, governments worldwide have used fiscal and monetary policies to regulate the expansion and contraction of the economy. During a recession, the government (fiscal) lowers tax rates or increases spending to boost aggregate demand and fuel economic growth. At the same time, The Federal Reserve (monetary) works to increase lending and spending. In an economic boom, they apply opposite strategies.

U.S. fiscal policy is predominantly built on the ideas of economist John Maynard Keynes (1883-1946), who believed that aggregate demand (total spending in the economy) drove the performance and growth of the economy and that inadequate aggregate demand could lead to prolonged periods of low economic activity. Keynes argued that governments could stabilize the business cycle by adjusting spending and tax policies rather than expecting markets to self-correct.

His theories were developed in response to the Great Depression and defied prevailing economic sentiments based on the free market (laissez-faire capitalism). Ultimately, Keynes’ ideas were highly influential and led to the New Deal, involving massive spending on a series of public works projects and welfare programs.

The Fed’s role during a recession is to enforce expansionary monetary policy to fuel economic activity. They do this through three key steps: lowering the interest rate, purchasing government securities, and reducing reserve requirements. Lowering interest rates, for example, will boost consumer borrowing and, thus, spending.

Recommended video: Monetary and Fiscal Policy: Crash Course Government and Politics

Recessions in the U.S.

The U.S. has withstood 14 official recessions since the Great Depression, confirming such downturns are an unavoidable part of the economic cycle or part of the regular cadence of expansion and contraction in an economy. Still, a recession and the chaos it brings are cause for concern and a painful departure from the economy’s usual growth mode.

Interestingly, recessions in the U.S. have become increasingly rare over the past 40 years, possibly because policymakers have gotten a better grasp on their causes. For example, according to the International Monetary Fund, there were 122 completed recessions in 21 advanced economies between 1960–2007, which makes the proportion of time spent in recession only about 10%.

Now let’s briefly list some of the most consequential recessions (and their causes) in recent U.S. history:

The Covid-19 recession (February 2020–April 2020)

The Covid-19 recession, also known as the Great Lockdown, is the most recent global economic recession caused by the COVID-19 pandemic.

The first significant sign of recession was the stock market crash in February 2020, which saw indices drop 20 to 30%. Then, in March 2020, the pandemic spread to the U.S, and the resulting travel and work restrictions caused unemployment to surge (from 3.5% pre-pandemic to 14.7% in April 2020), triggering an unusually short (the recession lasted only two months in the U.S.) but sharp recession.

Following the introduction of effective COVID-19 vaccines and aggressive stimulus packages, the U.S. economy and markets saw vigorous recovery from 2021 into early 2022, with the GDP for most major economies returning to or exceeding pre-pandemic levels and market indices setting new records by late 2020. However, by mid-2022, resurgent inflation led the Federal Reserve to raise interest rates, increasing recession risks.

The Great Recession (December 2007-June 2009)

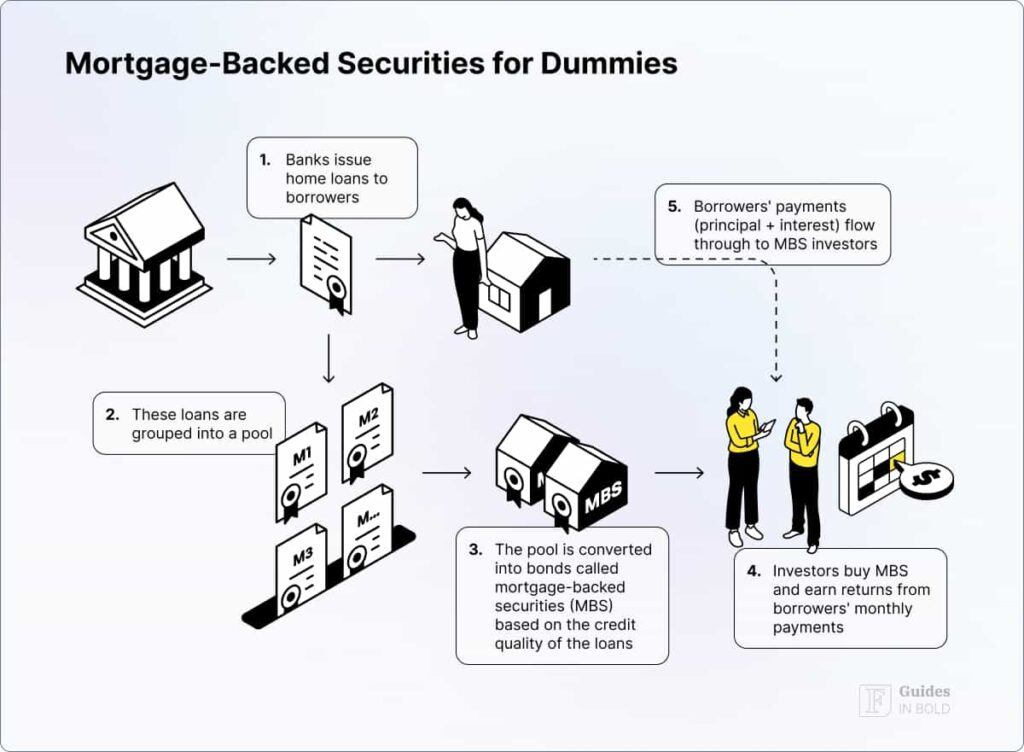

The Great Recession was the most devastating economic downturn since the Great Depression, caused by a combination of issues (e.g., lax lending standards, government housing policies, poor industry regulation), commencing with the collapse of the real estate bubble.

As housing prices fell and lenders began to default on their loans, the value of derivative products such as mortgage-backed securities (MBS) held by investment banks plunged, causing several to collapse or be bailed out. The period between 2007–2008 was called the subprime mortgage crisis.

Ultimately, the combination of banks being unable to lend to businesses and homeowners paying off debt rather than borrowing and spending resulted in a recession that began in the U.S. in December 2007, extending over 18 months, causing the GDP to fall 4.3%.

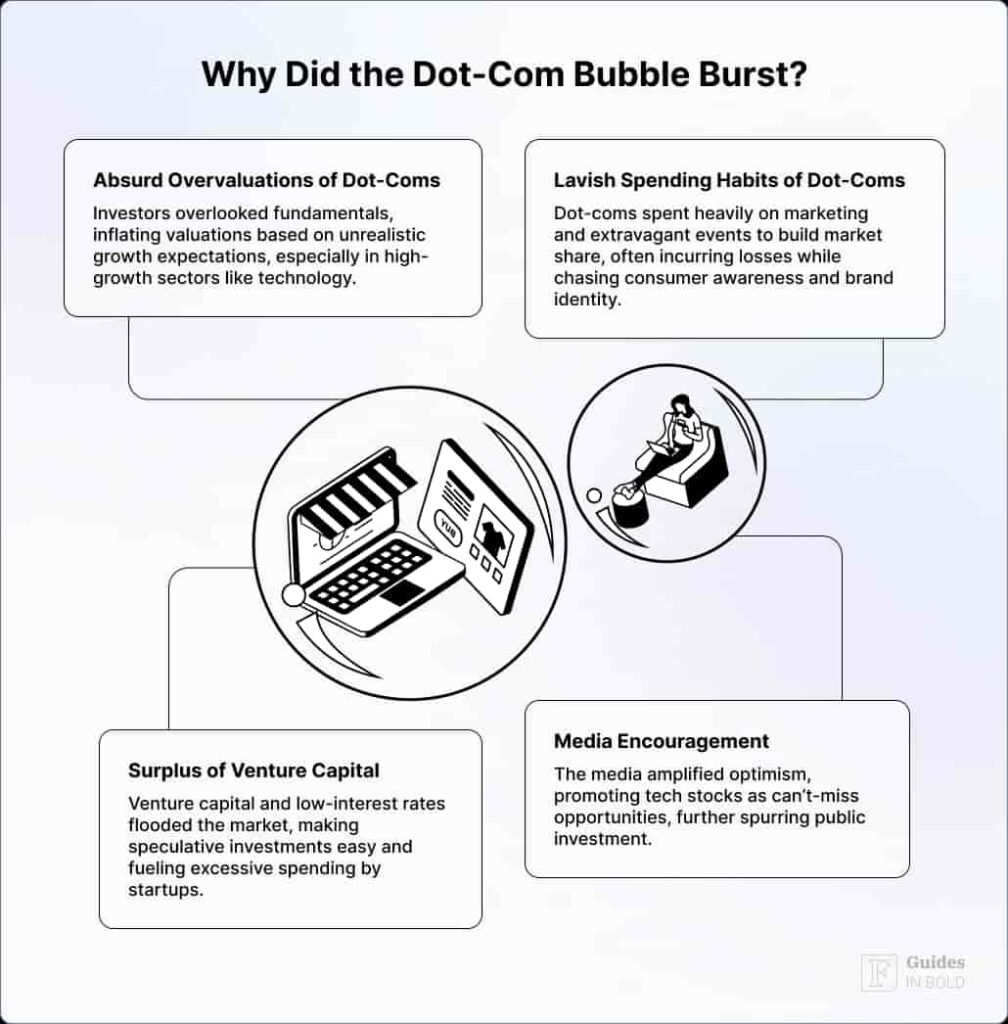

Dot-com recession (March 2001-November 2001)

The dot-com recession resulted from a bubble in technology stocks as commercial internet use rapidly expanded. The dot-com bubble was fueled by highly speculative investments in internet stocks during the bull market of 1995 to 2000, with the technology-dominated Nasdaq index increasing five-fold during that time.

Unfortunately, things started to shift in the late 2000s once investors recognized many of these companies had unsustainable business models, commencing a bear market that would last around two years and affect the entire stock market.

The crash saw the Nasdaq index plunge 76.81%, culminating in the majority of dot-com companies going bankrupt and evaporating trillions of investment dollars in its wake. It would take 15 years for the index to regain its peak, which it did on April 24, 2015.

Because of the economic stimulus provided by the Bush administration’s tax cuts and the federal funds rate reductions (benchmark rate reached a low of 1% by mid-2003), the recession that followed was relatively mild for the broader economy, though devastating for the tech industry. This recession was followed by the longest economic expansion in U.S. history.

The Gulf War recession (July 1990-March 1991)

At the beginning of the 1990s, the U.S. underwent a brief, eight-month recession spurred primarily by the restrictive monetary policy enacted by the Fed, primarily in response to inflation concerns which saw federal funds rates skyrocket to 9.75% in May 1989 – in effect – limiting economic growth.

The immediate cause of the recession, however, was the 1990 oil price shock (following the Iraqi invasion of Kuwait in August 1990), which saw oil prices double, resulting in a loss of consumer and business confidence.

The end of the Gulf War helped stabilize oil prices, which allowed the economy to hit its trough, but recovery was challenging. Unemployment continued to rise even after the recession, hitting its peak at 7.8% in 1992, a year after the recession was officially over. It was in 1995 that unemployment finally fell below pre-recession rates.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

How to invest during a recession?

While it’s important to remain cautious, a total lack of exposure to the stock market might mean missing out on picking up high-quality assets at discounted prices. So, though challenging, economic downturns also coincide with the best opportunities. Ultimately, a recession-proof investment strategy involves investing in high-quality companies with low debt, positive cash flow, and solid balance sheets.

Some of the recession-proof investment practices include:

- Invest in healthy companies: Look for companies (e.g., utilities, basic consumer goods conglomerates, and defense stocks) that are maintaining low debt, profitability, strong balance sheets, and a positive cash flow despite the economic headwinds;

- Invest in recession-resistant industries: Some industries perform relatively well during recessions. For example, counter-cyclical stocks, which typically move opposite to the prevailing economic trend, increase in value during times of financial downfall. During an expansion, however, they decrease. Counter-cyclical stocks can be found in these industries: consumer staples, grocery stores, discount stores, firearm and ammunition makers, alcohol manufacturers, cosmetics, and funeral services;

- Don’t panic: When markets fall, try to avoid impulsive reactions such as selling all your holdings;

- Diversify your portfolio: Move into well-positioned investments to endure a recession. Hold a mix of shares and bonds. Consider spreading across global markets not to be overexposed to downturns in any one area;

- Use dollar-cost averaging (DCA): Allocate a fixed amount regularly to your investments, regardless of the current price. In fact, recessions can be particularly lucrative opportunities to use a DCA approach because you’ll buy shares as the price falls;

- Consider dividend stocks: The best dividend stocks provide a cushion for your portfolio during an economic downfall. Even if a company’s stock price falls, it may keep paying dividends;

- Take advantage of cheap stocks: Amid a bleak economic climate, the stock price of investments may remain depressed, meaning there could be an excellent opportunity to buy stocks for a discounted price.

Recommended video: Warren Buffet investing advice during a recession

In conclusion

To sum up, periods of economic contraction are the inevitable corrective phases of the business cycle. And though they are a common factor in the economic landscape, they’ve grown less frequent and shorter in the modern era.

Despite the fact that recessions are temporary and have always been followed by periods of growth, they can still be frightening experiences. That is why it’s crucial to recognize the signs of a recession to be prepared when one eventually occurs. Above all else, investors should try to stay calm during times of market volatility and uncertainty, as well as maintain long-term perspectives so they can participate in the recovery.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about recessions

What is a recession?

A recession is a significant slowdown, i.e., a contraction in economic activity (popularly defined as two quarters of consecutive decline in GDP), illustrated by declines in real GDP, income, employment, manufacturing, and retail sales. Though painful, recessions are considered an inevitable part of the business cycle, characterized by the normal cadence of expansion and contraction in an economy.

What causes a recession?

A widespread drop in spending typically leads to a recession. This may be caused by numerous events, such as a financial crisis, supply chain disruptions, an asset bubble bursting, or a large-scale natural disaster (e.g., the COVID-19 pandemic).

How can high inflation cause a recession?

Rising inflation commonly leads to increased production costs, resulting in layoffs and fewer jobs in general. And if the Fed takes action by raising interest rates to combat rising inflation, there’s a risk that the move could help trigger a recession. This is because increased interest rates discourage borrowing and thus lead to decreased consumer and business spending, depressing demand even further.

How to overcome a recession in the economy?

In response to recessions, central banks typically adopt more lenient monetary policies to inject additional money into the economy. They achieve this by lowering interest rates, decreasing reserve requirements, and intensifying open market operations. Such measures are aimed at stimulating consumer spending and promoting increased investment by businesses. Additionally, governments often implement expansionary policies, including ramping up public spending and reducing taxes, to further bolster demand and rejuvenate economic activity.

How to predict a recession?

An inverted yield curve seems to be the most reliable metric for forecasting economic downturns, preceding each of the ten U.S. recessions since 1955. It signals that long-term interest rates for bonds are less than short-term interest rates, meaning the return decreases the further away the maturity date is.

How long do recessions last?

Economists measure a recession’s length from the business cycle’s prior expansion’s peak to the downturn’s trough. In the U.S., the start and end dates of recessions are officially declared by the National Bureau of Economic Research. For example, recessions between 1945 and 2001 lasted ten months on average, compared to 18 months for recessions from 1919 to 1945 and 22 months for recessions between 1854 and 1919.

How many recessions has the U.S. had?

According to NBER, since 1854, the U.S. has suffered 34 recessions.

What is the difference between a recession and a depression?

While both a recession and a depression describe periods of shrinking economic activity, they differ in severity, duration, and scale. A depression is a much more extreme economic downturn that can last for several years. There’s only one recorded instance of a depression in U.S. history: the Great Depression, beginning with the Wall Street crash of 1929 and ending during World War II in 1941.

Are we in a recession?

According to the conventional benchmark (two consecutive quarters of negative GDP), the United States entered a recession in the summer of 2022 (after Q1 and Q2 reported negative GDP). The NBER (the nonprofit organization responsible for declaring recessions in the U.S.), however, didn’t then and still (as of December 2024) hasn’t announced a recession.

What is a double-dip recession?

A double-dip recession, also referred to as a W-shaped recovery, is when a recession is followed by a brief rally, then another recession. Double-dip recessions can be caused by various reasons, such as economic shocks or contractionary government policies, and involve prolonged unemployment and low GDP. The last double-dip recession in the U.S. occurred in the early 1980s.

How can a bursting of an asset-price bubble in the stock market trigger a financial crisis?

The bursting of a stock market bubble can trigger a financial crisis by rapidly deflating asset values. This sudden drop in stock prices erodes investor wealth, dampening consumer confidence and spending. The ripple effect leads to reduced business revenues, potential layoffs, and significant losses for financial institutions invested in these assets. These combined factors can strain the financial system and potentially lead to a wider economic downturn.

What happens to mortgages during a recession?

During a recession, mortgage rates often decrease due to central banks lowering interest rates to stimulate the economy. This makes borrowing cheaper, potentially leading to more affordable mortgage payments for new borrowers. However, existing fixed-rate mortgage holders may not see a change in their payments. Conversely, those with adjustable-rate mortgages could benefit from reduced rates. Additionally, the housing market may slow down, with lower demand leading to decreased home prices. In short, the situation can be challenging for homeowners looking to sell, but advantageous for buyers.

Where to put retirement money in a recession?'

In a recession, it’s generally advisable to place retirement funds in conservative, low-risk investments such as bonds, money market accounts, or high-grade corporate or government debt securities. Diversifying your portfolio across different asset classes, including some exposure to stocks for long-term growth potential, can also be wise. The key is to focus on preserving capital and minimizing risk, rather than seeking high returns, given the typically volatile market conditions during a recession.

Who benefits in a recession?

During a recession, entities that typically benefit include discount and essential goods retailers, debt collection agencies, bankruptcy attorneys, and businesses involved in cost-reduction services. Investors with cash reserves can also benefit by acquiring assets at lower prices. Additionally, companies that offer affordable or essential services tend to remain stable or even thrive in such economic downturns.

How does recession affect 401k?

A recession can negatively impact 401(k) accounts, primarily through declining stock market values, leading to reduced account balances. However, the extent of the impact depends on the account’s investment mix and the market’s overall performance. Long-term investors might see their 401(k)s recover post-recession, especially if they continue contributing regularly and maintain a diversified portfolio. For those nearing retirement, the effect can be more significant, highlighting the importance of a well-balanced investment strategy that accounts for market volatility.

What is the Keynesian solution to a recession or depression?

The Keynesian solution to a recession or depression focuses on increased government spending and lower taxes to boost demand and stimulate economic activity. This approach, based on the theories of economist John Maynard Keynes, advocates for government intervention to offset decreased private spending during economic downturns, thereby fueling job creation and consumer spending. The goal is to kick-start the economy through fiscal stimulus until private sector demand picks up again.

What is the difference between recession and inflation?

Inflation refers to the general increase in prices and decline in purchasing power over time, whereas a recession is a period of economic decline, typically identified by a decrease in GDP for two consecutive quarters. Inflation is characterized by rising costs of goods and services, while a recession is marked by reduced consumer spending, business investment, and often increased unemployment. In short, inflation indicates an economy where prices are growing, whereas a recession indicates an economy that is contracting.

What happens to gold and silver in a recession?

In a recession, gold and silver often act as safe-haven assets, with their prices generally increasing as investors seek stability away from volatile stock markets. Gold, in particular, is seen as a hedge against economic uncertainty and inflation, leading to higher demand and prices during economic downturns.

Does anything get cheaper during a recession?

Yes, during a recession, certain things can get cheaper, such as housing, stocks, and some consumer goods, as demand falls and businesses lower prices to attract customers. However, not everything necessarily becomes cheaper, as the impact varies across sectors.

What should not do in a recession?

During a recession, it’s important to avoid panic selling investments, taking on high-interest debt, making large unnecessary purchases, neglecting your emergency savings, and overextending on risky investments. Staying financially cautious and focusing on stability can help you weather the economic downturn more effectively.

Can banks seize your money if the economy fails?

No, banks cannot directly seize your money if the economy fails. However, during severe economic crises, governments might implement measures like freezing accounts, limiting withdrawals, or enforcing bank bail-ins, where depositor funds could be used to stabilize failing banks. However, this is rare and typically happens only in extreme situations.

Should I take my money out of the bank in 2025?

It’s usually not a good idea to pull out large sums from the bank unless you have specific concerns. Most banks are insured by institutions like the FDIC, which protects your deposits up to certain limits. Instead, think about spreading out your investments, keeping some cash handy for emergencies, and staying up-to-date on what’s happening in the economy.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.